UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

newrobdob - MemberI was wondering when did the split occur? <snip> First house was £53k, paid £28k of that off and sold for £110k. I might have been one of the last people to get a 100% mortgage

That's when the split occurred.

It won't last forever though, all markets self-correct in the end

As has been stated repeatedly over the years though, it isn't a functioning market. And hasn't been for deacades. Governments constantly meddle in it for short term political expediency. From flogging cut price council homes in the 80's (to buy votes) through to the frankly insane Help to Buy scheme introduced by Osbourne (to buy votes)

IMO, I think you'll find the 'us & them' has just been re-established, except now the percentage of ownership has increased markedly from pre 80's.

Which makes the lenders very happy as they now technically own much more capital/assets, earning interest ( read rent) on long term loans and taking very little liability and responsibility for the maintenance and upkeep, leaving that to the 'owners' ( read tenants - until,of course the debt is fully paid).

To summarise @stoats and @pjay 😉

Just looked at where we used to live in N. Wales. We lived in a terrace of slate miners' cottages right next to a main road. Even for the area they were nothing special.

1999: £32k

2001: £41k

2002: £43k

2017: £90k

Apparently the average for a terraced house in that village is £122k.

Looking round us and up into The Dales - average price is £300k - £360k. These prices have a social impact. There's no way a young couple can afford to buy a property given that most jobs in the area are agriculture/quarrying/tourism based. Is it any wonder that local schools are getting shut down due to lack of pupils. Yet attempts to provide "local" housing are met with resistance, primarily from those who can afford the current prices.

I remember when I was younger, a typical mortgage was 3.5x a single salary (conventional wisdom was that you shouldn't borrow more than this). So your £30k salary nets you a £105k mortgage. I hope you like living in the less salubrious end of Burnley.

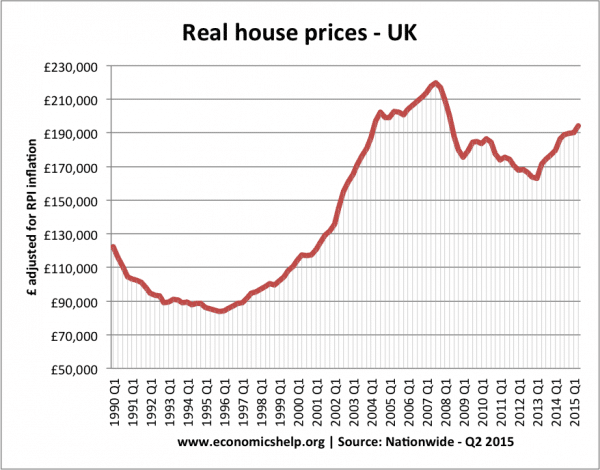

and with interest rates at 11%, that's possibly a sensible figure. When they're <1%, what is the point in making a high earner move houses several times (in order to get to the house they want) rather than allowing them to borrow what is (to them) an affordable sum of money? static earning multiples are a pretty hopeless tool as they don't take into consideration number of dependents, costs, or overall level of earning (bringing up a kid on £10k takes a lot more of your take-home income than bringing one up if you earn £100k). The graphs on the first page show that payments as a % of income are at their lowest rate since 1988..

208k will get you a rather nice (if I do say so myself) 3 bed detached corner plot with a garage in the grim midlands. It's got riding from the door as well...

Granted I couldn't have afforded it by myself or without help from parents so we've actually been very lucky. Saying that, friends that are more sensible with money have managed to save for a deposit (although I'm mainly friends with engineers so wages tend to be higher)

It won't last forever though, all markets self-correct in the end

Yes and no. This isn't a simple supply/demand system, because there are different aspects to demand.

We might end up with houses being affordable to private landlords but not first time buyers; which would result in houses being a commodity subject to its own market driven by investors not homeowners. So again, rich people get even richer as this capital gets handed down to offspring, and rents can go up to the point where the poorer or younger people can just about afford to pay leaving them no spare money to save. And worse still, if say young professionals can only afford to rent and not buy, they will become trapped so when they finally die they have no capital to pass on to their grandkids who won't be able to get out of the trap.

Keeping people renting transfers money from the poor to the rich.

£90k will get me a small plot of land with planning permission, or a two bed caravan in a trailer park.

You'd get a 4 bed terraced house for that near me and enough change left over for a decent 2nd hand car. It wouldn't be anything fancy but in a safe area with good neighbours.

I think too many people get caught up in what other people would think of them when buying somewhere to live and overstretch to the point they have almost nothing left over.

I'd much rather live very comfortably in a modest house in a less desirable area than be upto my eyeballs in debt with not much spare for anything else.

I suppose the same goes for cars.

I've just resigned myself to living in footflaps' shed until I manage to kill off the family.

binners - MemberIt won't last forever though, all markets self-correct in the end

As has been stated repeatedly over the years though, it isn't a functioning market. And hasn't been for deacades. Governments constantly meddle in it for short term political expediency. From flogging cut price council homes in the 80's (to buy votes) through to the frankly insane Help to Buy scheme introduced by Osbourne (to buy votes)

I have it on good authority that 1) the Banks are ready to absorb a reduction or hold in property prices on their balance sheets, 2) the number of Millennials and X&Ys in 'generation rent' along with concerned mortgage payers is passing the number of Boomers to make it politically viable to do it.

The recent easing of planning rules and large scale building projects represents the first cracks in post-credit crunch plan to protect prices.

It won't hopfully be a massive crash, it's unlikey (Brexit disaster aside) but the gap between income and prices will narrow and it will be by a lot.

I'd much rather live very comfortably in a modest house in a less desirable area than be upto my eyeballs in debt with not much spare for anything else.

What else do you do with your money though?

It's not just a case of trying to impress people, in the early 2000's it was one of the best investments you could have made. And the best thing is, it's mostly the banks money your investing, like a 10x mutiplier of your deposit.

I remember when I was younger, a typical mortgage was 3.5x a single salary (conventional wisdom was that you shouldn't borrow more than this)

That ratio was the max I could borrow in 97 IIRC.

I've just resigned myself to living in footflaps' shed until I manage to kill off the family.

I have 16 Lithuanians in there at the moment.......

My daughter is 25 and about 2 years into a career as an IT consultant. Late last year she changed job so that instead of being based in London she could base herself out of Edinburgh, with one of the main reasons being was that she can afford to buy a decent flat now (£110-130K or so) in Edinburgh but is years away from being able to do so in London (and even if she could it'd either be a shite area or really far out).

I think too many people get caught up in what other people would think of them when buying somewhere to live

If you live in an area with cheap housing, I suspect you haven't experienced what drives people to stretch themselves with house prices.

I don’t get the issue from my experience; I bought my first house with then girlfriend at 23 years old in 2010 for £135k. Salaries where £20k each. We then sold that for same price and bought second home for £186k on a joint salary 50k. We sold that 3 years later for £60k profit and bought our house now for £205k and spent £20k renovating – it’s now worth £300k with a mortgage of £200k on a joint salary of £70k. We haven’t been ‘lucky’ on house purchases – simply bought the right house in the right area and renovated it sensibly.

In my area – N.Wales and Chester house prices are certainly reachable and there’s still money to be made.

Nothing on rightmove for under £90k here, oh apart from a block of 3 garages for £65k and an old BT repeater station for £20k and Aylesbury is hardly leafy suburbia

I have 16 Lithuanians in there at the moment.......

Must try harder, I reckon you could house 30 Syrians at a push.

I have it on good authority that 1) the Banks are ready to absorb a reduction or hold in property prices on their balance sheets, 2) the number of Millennials and X&Ys in 'generation rent' along with concerned mortgage payers is passing the number of Boomers to make it politically viable to do it.

I'll believe it when I see it. Every single government has made similar noises. None have got even close to actually doing anything realistic about it. As with most things where politicians and bankers are concerned, don't listen to what they say, look at what they do.

It won't hopfully be a massive crash, it's unlikey (Brexit disaster aside) but the gap between income and prices will narrow and it will be by a lot.

Given there's no indication wages will rise meaningfully in the short-medium term, I don't think we can have one without the other.

I think the only thing that is likely to make houses affordable for first time buyers again is a rise in interest rates big enough to shaft people who are leveraged really hard on their existing mortgages, a la the 80s. However I don't think BoE will be willing/allowed by its political overlords to raise rates, even to counter the horrendous inflation we'll see as a result of Brexit.

EDIT: beaten to it by Binners, more or less.

Sometimes it is luck, "well timed" might be a better term: when I moved to our current area I was renting a flat at £300pcm as well as paying a small mortgage on our then current house. It wasn't a nice area so looked for something else, found a small terraced house for £34k, I'd got savings so put down a decent deposit and had a second mortgage of £115pcm.

We then moved to the area and bought our current house, sold the terraced house for £60k after just two years of owning it and basically paid off the mortgage on our current house. The sub-prime financial crisis started about six months later.

Edit: and when I went to the bank to use the proceeds to pay off the mortgage I got: "Ooh! You've a lot of spare equity. Do you want to take out a loan?"

It's not just a case of trying to impress people, in the early 2000's it was one of the best investments you could have made. And the best thing is, it's mostly the banks money your investing, like a 10x mutiplier of your deposit.

This, in the SE.

Housing in London is/was the 90's/00's replacement for the final salary pension. We've been very, very fortunate- especially since we left and bought elsewhere..

Had this thread before and as I pointed out Darlington in Durham is a great town with plenty of Jobs and good affordable housing on the East Coast Main line - however the person that was moaning didn't want to live in a "Darlington" they wanted trendy Leeds city centre for £2.50... there is loads of affordable houses in the UK just not in the South East

Irrespective of all of this^, it's a [i]total[/i] shitter on one salary 🙂

there is loads of affordable houses in the UK just not in the South East

Aye, it's grim daan saff!

I bought my first house with then girlfriend at 23 years old in 2010 for £135k. Salaries where £20k each

What if you don't both earn 20k? What if you're single?

You really can't see a problem?

To answer the OP, 1999 dot com bubble, investors got out and put money in housing, cheap credit and low interest is making many things boom in price as keeping money in the bank earning 1% is pretty pointless, witness silly prices for classic cars, bikes, art etc etc

What if you don't both earn 20k? What if you're single?

What if you're married with a partner who can't work, 2.4 kids and a spaniel?

That's the point I was alluding to (badly). Time was, one salary could raise a family. Now we've got a situation where both adults [b]have[/b] to work in order to keep a roof over their heads whilst maintaining a half decent standard of living.

I don't have kids, I don't know how you lot do it.

I don't know how you lot do it.

I sometimes wonder how (and have posted around this subject in the past). I earn decent money, my wife gets a small salary from my business and also works part time so between us our income (before tax) is around £80k.

We have a mortgage (£1k a month but 'own' around 65% of our current house) but no other debts (ie, no HP on cars etc) other than the usual household things yet every single month we are broke. Yes we get some nice things but are very careful with money (my wife shops at Primark/Sainsbury's etc for clothes, I use TK Maxx) and we do get to go away on holiday once a year. but that is never anything overly fancy.

However, many of the other parents at our girls' school rock up in expensive cars/4x4s, go to exotic locations for 5 star holidays (two, three and even four times a year) and all seem to be draped in expensive clothes and jewellery – and they all have nice houses and are spending loads on extensions/conversions etc. One parent recently posted on Facebook (about a week after returning from a 5 Star holiday in Mauritius) asking about recommendations for luxury breaks to Lapland for next Christmas.

I simply do not know how people* do it – are they all just banging it all on credit?

*However I do know that one family have an interest only mortgage which (to my mind) is utterly bonkers.

Sandwich - MemberMust try harder, I reckon you could house 30 Syrians at a push.

Under 16s or children? 🙂

Im 30.

3 bed semi in the greenbelt.

Set our goal and saved like **** for it

I did 18months adhoc taking all the work abroad I could get in equatorial guinea- Nigeria and holland working on the rig's.7-8 weeks at a time. I did another 3 years doing ad-hoc without the same urgency mind to get the money to renovate it and to pay it down to a comfortable monthly level. And have finally taken a position where I only work 6 months of the year to shift the balance back the other way.

I have several peers who are all similarly educated living near by who have all bought houses in a variety of methods. Some have grafted for a deposit like we did - others the bank of mum and dad and some are mortgaged to the eyeballs.

How ever being in a very expensive part of Scotland( compared to living in Dundee or Glasgow) I must say I don't know too many people who have not managed to get them selves a house IF they wanted one.

Equally Brother in law bought a nice 2 bed flat for less than half what our house cost - in Glasgow.

I'm not sure what I did is too different to the olden days. One of my older colleagues dad's bought his house after 2 years in south Georgia whaling !

Johndoe - interest only mortgage makes sense if it is far cheaper than renting and you are investing the extra elsewhere for greater return

Edit 80k PA and you are broke!

london and south east, properties are expensive, but not definitely 'too' expensive

[url= http://www.rightmove.co.uk/property-for-sale/property-39972246.html ]Personally i think oieo 380k for a 2 bed ex council flat in an area with a high crime rate is pricey, its not even in hipsterville.[/url]

interest only mortgage makes sense if it is far cheaper than renting and you are investing the extra elsewhere for greater return

Well yes, *IF* you are. I have no idea if they are or not, but the amount they spend on cars (they currently have four although only two people can drive), holidays, clothes etc makes it seem unlikely (neither are exactly high earners although of course I don't know particular details and perhaps they have been recipients of windfalls).

Edit 80k PA and you are broke!

Yup! I really don't know how, but we do spend quite a lot on clubs etc for our children which really adds up – singing clubs, gymnastics, horse riding, music lessons etc – I guess we are investing in their wellbeing.

london and south east, properties are expensive, but not definitely 'too' expensive

Two of my younger colleagues have just bought a 1 bed flat together for £450k.

Aye well johndoh you do never know. No one ever tells the whole story .

Learnt that lesson along time ago when my mate always had the best of toys.....When I was old enough I understood why. His parents had split and dad was trying to buy his love. He said he always looked in at my mum and dad and wished he had the family rather than the toys.

Look after you and yours and don't worry about the others. They wouldn't worry about you. There's usually always another side to every story.

Look after you and yours and don't worry about the others.

To be honest I try not to, but my wife comes home from school drop off quite regularly saying 'x is doing y' and it makes me feel like I am not able to provide for my family in the same way others seem to be able to do.

Everyones situation is different, i thought i had missed the boat through variable earnings (self employed) and being single or in relationships that didn’t last long enough to settle. i’m mid 40’s and only bought 2 years ago having been shafted by my bank (having 80k in savings with them but them not lending me a penny for a mortgage)

switched banks and i had to wait another year to buy thus paying more. bought a small flat in SE19 (good area, good street, cheapest property) and had to put down 65k as there was no way i could get a low LTV mortgage being self employed.

now 2 years later its gone up 120k and i’m in a stable relationship and between us we are sitting on 850k of property that we probably owe 360k on. its nuts when i think about it.

but i still think younger people can do it if you put your mind to it and don’t expect to be going out every night and having the latest gadgets etc. i did it with zero help from M&D.

i am surprised how little property has increased in some of the shires mentioned in this thread, i guess this is low wages that a keeping laid on things.

Cougar - Moderator

[i]What if you don't both earn 20k? What if you're single?

What if you're married with a partner who can't work, 2.4 kids and a spaniel?[/i]That's the point I was alluding to (badly). Time was, one salary could raise a family. Now we've got a situation where both adults have to work in order to keep a roof over their heads whilst maintaining a half decent standard of living.

That's precisely the aspect which Stoner's link is missing. The socioeconomic landscape has changed dramatically in the past 30 years. Not all families are geographically close anymore, childcare is common (and very expensive) both parents are likely to work full time.

Also, household income doesn't tell the whole truth. Earning £60k, you may have been to Uni and thus have loans which reduce your income by over £300pcm, childcare can cost over £1000, utilities are more expensive. the amount you have available for a mortgage (as decided by the bank) will be substantially lower than your 3* combined income.

Just how much income is required to buy a 3 bed house in an okay area in Bristol? You'd need to be earning over £80k, have no dependants, no debt and no life. Rent in Bristol can easily top £1000 for 2, add in utilities, consumables, transport and insurance and you're over £2500 per month. at £80 you'd be paying over £430 in student loans. You're left with £1000 per month before you've bought anything or done anything. lets assume you can save 85%. it'd be 3 years before you have a deposit...what happens if you're 30 and are thinking of starting a family? Do you wait? My £380k house has gone up by over £60k in 2 years, so the house you were aiming for, saving for, is now out of reach...If you have kids, your £1000 per month that you were saving isn't going to be there for long...

interest only mortgage makes sense if it is far cheaper than renting and you are investing the extra elsewhere for greater return

That's what I did and borrowed as much as I could starting from 1996 which seemed to me to be a good time to buy as were starting to recover from the nightmare of the late 80s/early 90s. Worked out rather well for me, I took risks but mitigated to a degree by having lodgers.

[img]  [/img]

[/img]

Yup! I really don't know how, but we do spend quite a lot on clubs etc for our children which really adds up – singing clubs, gymnastics, horse riding, music lessons etc – I guess we are investing in their wellbeing.

Not easy the pursuit of "upper middle class" ....

we are sitting on 850k of property that we probably owe 360k on. its nuts when i think about it.

It's nuts at a casual glance, TBH. (-:

The wife and I are currently saving like mad to get on the ladder, I'm 27 she's 2 years my junior, combined income of 55k ish, been renting for 4 years and recently got married so that blew our deposit, so started from zero again this new year. Looking around the 200k price for 3 bed place, around north Norfolk, we are putting away a large amount of cash in savings and we estimate it will take 2 years for the deposit alone.

We are told there are not enough new houses being built, but also that there are lots of empty houses, but perhaps not in the right places, and there seems little central will to alter things to push industry and tech start-ups to base themselves in lower cost areas. But the Market really is not going to sort this out.

I've often seen it quoted that there's over a million houses empty across the whole country, and certainly there seem to me lots of empty space above shops in many towns, space that's otherwise used as a junk store. Trouble is most of the property owners quote security as the biggest impediment to letting out those spaces; surely though having people living above the shop and others in the area keep it alive and add to security, being able to react quickly to unusual noises or activity at night or weekends.

European cities apparently have a much higher density of occupation within the main shopping areas, this has to be the answer for our cities and towns.

Why the **** did you blow it on a wedding? Serious question