UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

But the question is how much of the bull run have you missed by being out of the market?

None so far, I lightened up at the March highs just before the Trump tarifs spooked the markets, and knowing I'd need a lot of it within seven months. The stuff I sold is at almost exactly the same level this morning.

Sorry if it seems like I'm trying to pick on you, that's not my intention. It's essentially a debate about active Vs passive investing strategies where you prefer active and I prefer passive (albeit constantly having to resist the temptation to have an active dabble).

In this particular example, if you'd have adopted a passive approach and invested in a global index fund in March then you'd be about 15% up by now. So it seems your active decisions in respect of both stock selection and timing have lowered your returns on this occasion. Although if the market drops back below the March level again, which it may well do, you might still feel vindicated.

I read Edukator’s post as implying he realised some investments because he knew he had some cash needs in the immediate future and his commentary was on what remained. Less an active vs passive strategy, more a bird in the hand vs two in the bush approach, and totally understandable.

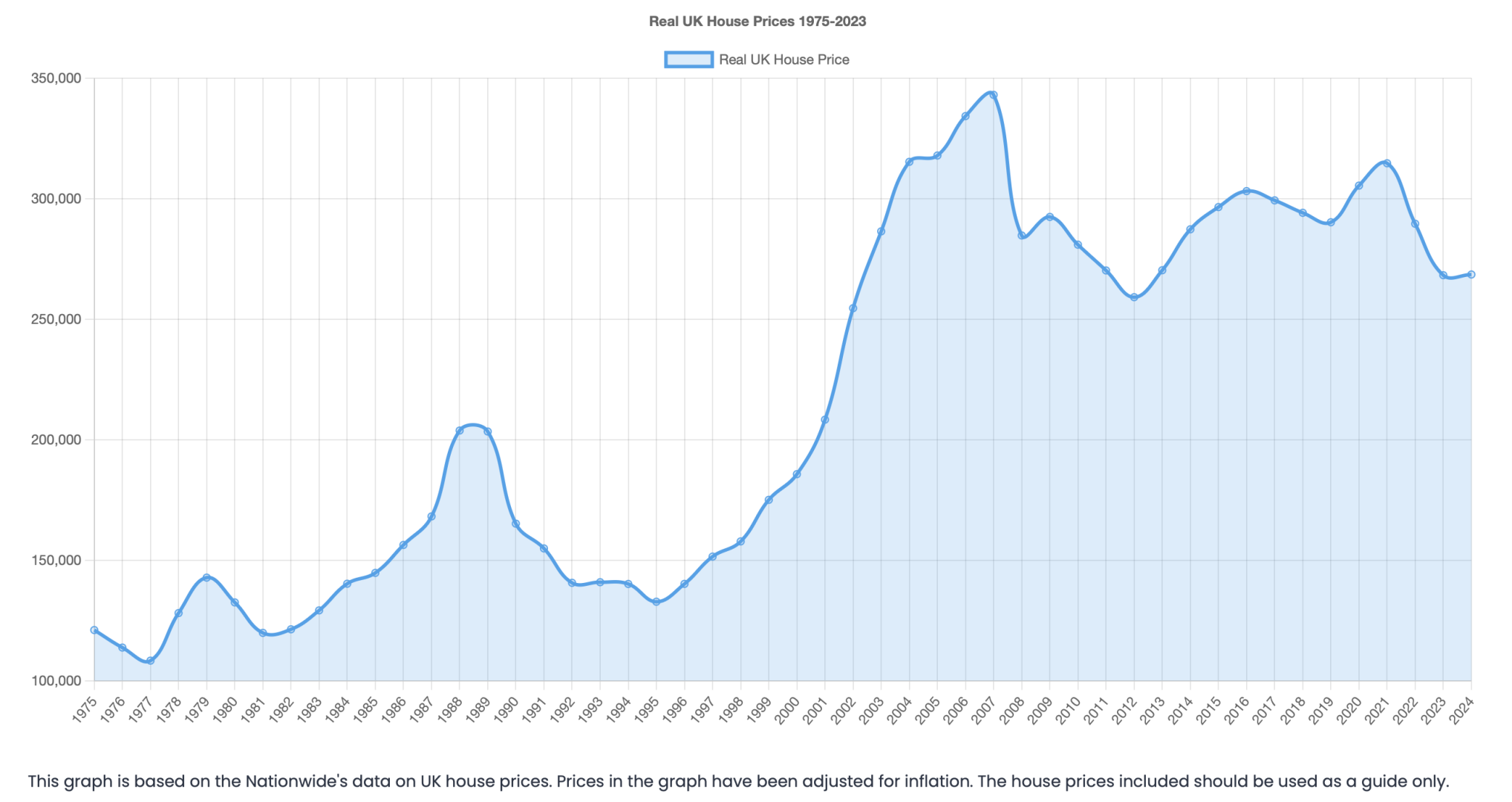

At the end of the day leveraged property has smashed everything else in terms of returns in this country over the last 30 years, so anyone who was fortunate enough to benefit from that has done well. Pure luck rather than judgement though.

I posted this the other day. If you bought property in the 90's you've done really well. Post 2000? not so much - we're only now where we were in 2003 in real terms.

Thing is I don't want to be in a Global Index fund, Roli Case. The stocks in those indexes are some of the most overvalued in my view. The boom in index linking is part of what I see as a bubble and I don't want to be a part of that at this point in time. Even if I'd invested in index funds I don't see how I'd have got 15% since March. No gain since March is pretty good for someone investing in Euros.

The rise of Euro against the dollar would have eliminated any gains compared to US indexes. The Euro is up 12% since March

Euro pound is up about 8% and the FTSE about the same

Eurostox 50 is where I sold

The CAC has gone nowhere

I could have made money in Asia even though the Euro is strong. I sold out of Asia about ten years back when I finally saw a reasonable profit after years of ups and downs. Asian ETFs are a lottery IME.

So from my Euro investor point of view any gains since March have been from lucky/wise choices rather than following indexes. And in pound terms the portfolio I've kept is nicely up, even the one I said had "underperformed" is positive in pounds..

Dow futures looked promising earlier but as we get closer to the open not so.

There are all sorts of thematic ETFs..

Global minus USA... 'VXUS' for example, or global developing marks, etc etc.

There's an ETF for all occasions!

Global ETFs and s&p500 ETFs are the most popular at the moment as that's where most returns are made currently..

And you can split your money between a couple to accomplish what sort of weighting you want.

For example I'm about 60% in 'all world' and about 40% in developed Europe (large and medium cap companies).

I was about 7% up overall since April which is pretty good going, but I'm only about 5% up after Friday's shenanigans. It'll recover over the next week I'm sure.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

"A couple", I've lost count, somewhere around 12. 🙂

"A couple", I've lost count, somewhere around 12. 🙂

Lol. You might want to look at consolidation if you've got 12?!

Seems a bit excessive! But if it works for you it works.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

So, I'm 5 years off my teachers DB pension and want to retire. For £54K of my SIPP, I can get £12000/year for 5 years from a fixed term annuity. That's the same as a guaranteed annual growth of around 4.5% if I left that £54K at the mercy of markets and used flexi draw down. I'd still have the rest of my SIPP and ISA invested, but this could ride out 5 years of instability quite nicely.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

<off to the classifieds in search of a crystal ball or ravens entrails....>

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

So, I'm 5 years off my teachers DB pension and want to retire. For £54K of my SIPP, I can get £12000/year for 5 years from a fixed term annuity. That's the same as a guaranteed annual growth of around 4.5% if I left that £54K at the mercy of markets and used flexi draw down. I'd still have the rest of my SIPP and ISA invested, but this could ride out 5 years of instability quite nicely.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

<off to the classifieds in search of a crystal ball or ravens entrails....>

Depends entirely where you are at in life and what you want, there's no 'one size fits all' strategy. Generally people (and pensions) 'de-risk' as they get older to avoid impact from market crashes, so they might transition more to bonds than equities, etc.

But I'm only mid 40's so I'm going hard on equities at the moment, and I can afford to ride the waves of a stock market crash without panic selling...

..If I were 2 years from pension age though, I'd have a much more conservative attitude.

I didn't have time to edit my post, when I say 'going hard on equities' I mean big ETFs, not individual stock picking/stock trading, I'm quite conservative in my strategy, 'buy the whole market' if you have time to ride any dips out, rather than spinning the wheel and buying individual stocks/shares.

The returns are less exciting, but the risk is a lot lower, too.

boxelder. The 4.5% guaranteed on the annunity is what treasuries around 5 years are yielding so the insurance company offering that annuity is taking very little risk. No risk to you, reasonable return - that's sounds pretty good for money you know you are going to spend over the next five years. 5 years is too short to ride out ups and downs on money you know you're going to need. Imagine you'd taken the risky option in Summer 2000 and see where that would have left you. If you think about it it's better than 4.5% because they have less and less of your money to invest as they give it you back. More like 7%

High risk strategies are for money you don't need in the short term and may never need at all.

For those thinking the market in AI is overpriced and is going to crash/slump/dip/adjust..... Well, you're not the only ones.

https://youtube.com/shorts/efPNRNtbOdY?si=wXAjthiLCdibQomx

Channel4 News podcast is out there on this topic. Worth a listen.

I'm counting the days till November when I can cash out my employee share options. If I can do that before the crash then I think I'll be reasonably covered.

If I don't then......

Hmmmmmm. I have instructed a matured cash ISA to be transferred to Vanguard with a view to opening a S&S ISA all allocated to the VWRP ETF.

The request hasn't been executed yet so think I might just dump the cash into another cash ISA..

I'm counting the days till November when I can cash out my employee share options. If I can do that before the crash then I think I'll be reasonably covered.

My employer is the largest gas consumer and B2B supplier in Germany. 90% of our supplies came from Gazprom before the Ukraine war, and for a year or so we had to make up all the lost volumes at market spot prices when the supplies stopped overnight.

Shares lost 98% and really haven't recovered because basically we got taken over by the German government and there's none to trade on the market.

It's a good job I'm not relying on those as part of my retirement planning. 😭

I think that the AI engineers and CEOs don't understand probability and exponential functions very well. To my mind, AI is almost certainly going to burn out and not show most of the improvements that it is purported to.

However it doesn't matter what I think, it's what the rest of the market thinks that matters. In order to time the market, I both need to be correct, and at the right time. Being correct at the wrong time is just another form of being wrong in business and finance IMO.

Hmmmmmm. I have instructed a matured cash ISA to be transferred to Vanguard with a view to opening a S&S ISA all allocated to the VWRP ETF.

The request hasn't been executed yet so think I might just dump the cash into another cash ISA..

Vanguard platform charges platform fees, on top of the fund management fee. If you want to buy a vanguard ETF, you're best buying it within a stocks and shares ISA on a fee-free platform such as T212 or invest engine.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

Not that it will make much difference to the decision on this amount but wouldn't it be more like £4k left assuming you draw down monthly rather than yearly?

Your average investment for calculating returns in Yr 1 is £48k, not £42k, and so on.

Not read all of this but are you a couple with no mortgage? How much do you give yourself each week?

^^ not sure which post that is asking about. There was a lot of chat quite a few pages ago on the magic number for a couple on their own without a mortgage. I recall the average was around 3-4.5k per month, after tax, to cover all life costs.

If you think about it it's better than 4.5% because they have less and less of your money to invest as they give it you back. More like 7%

The quick calculation I did was subtracting the drawdown each year, so fairly sure it matches 4.5%. I'd always seen annuities as too conservative/playing too safe, but a short term one could safely see me to DB pension starting, so I now know I can afford to become an idle ne'erdowell retire. It's still a chunky decision though, with my wife not wanting to retire and employers needing to fill the (small) gap I'd leave

.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

Not that it will make much difference to the decision on this amount but wouldn't it be more like £4k left assuming you draw down monthly rather than yearly?

Your average investment for calculating returns in Yr 1 is £48k, not £42k, and so on.

Correct (probably). I was doing some crude sums to get the approximate annuity AER and then applied the same to the 7% growth i.e. subtract £12k, multiply by 0.07 etc.

I always thought all this shizz was dull, but once you realise it can stop you having to turn out for work.........

Why worry about your employers filling the gap you leave? It’s not your problem, and if it is a problem for them you might find they offer you a sweeter end to working life such as flexi/part time work or more money until they do find a replacement.

They're friends and it's already PT/Flexi. It's not really an issue if I give notice.

I always thought all this shizz was dull, but once you realise it can stop you having to turn out for work.........

I do also think it’s easy to overthink it all, I’ve certainly found that to an extent.

Why worry about your employers filling the gap you leave?

"The Indispensable Man" by Saxon White Kessinger

Sometime when you’re feeling important;

Sometime when your ego ‘s in bloom;

Sometime when you take it for granted,

You’re the best qualified in the room:

Sometime when you feel that your going,

Would leave an unfillable hole,

Just follow these simple instructions,

And see how they humble your soul.

Take a bucket and fill it with water,

Put your hand in it up to the wrist,

Pull it out and the hole that’s remaining,

Is a measure of how much you’ll be missed.

You can splash all you wish when you enter,

You may stir up the water galore,

But stop, and you’ll find that in no time,

It looks quite the same as before.

The moral of this quaint example,

Is to do just the best that you can,

Be proud of yourself but remember,

There’s no indispensable man.

^^ that’s great, not seen it before.

Thought I’d bump this along a bit to see if anyone else has joined the club ! Loving it so far, and it’s certainly making the 100 days of exercise thing a lot more doable this year 🤞

I finished work one week ago ! 38 years in work with 5 different companies in the private sector. The biggest change has been handing back my company mobile phone and the phone number, and having my own phone. No more emails , no more calls at ridiculous hours of the morning from security or the night shift. With a work phone as the only phone - I never felt truly away from work. Its odd not to have a "schedule" that we've all had since aged 5 - school, academic year, work etc. Now its all my time. And yes the 100 days of exercise is much more doable - trying to mix it up with Swimming running and biking. Joined the gym. Went to Tescos at 11.00am on a Tuesday - who are all these old people - oh I am one of them....... Its not a great time of year to finish after the summer we've had - hence the gym/swim thinking. Looking forward to some bike touring next year and travelling with Mrs OD.

Enjoy it. 😎

Haven't had a minute since finishing at the end of March. We had just got back from our 3rd tour of riding in Europe and was offered a trip to Soul on the Reef in Tenerife from someone who couldn't go.

Checked the Schengen calculator, had enough days come on for November so on impulse we are here.

Couldn't have done any of it pre retirement.

I finish December 31st via redundancy! The stock market is making me very twitchy at the moment to be honest. My payoff of 2 years pay will be carefully saved as I feel already exposed with my DC pension along with current employer share scheme.

What pocket money jobs do people have?

Is a days pay for collecting supermarket trollies worth getting out of bed for?

The stock market is making me very twitchy at the moment to be honest. My payoff of 2 years pay will be carefully saved as I feel already exposed with my DC pension along with current employer share scheme.

A fairly similar position here, and hoping to not need to start drawing on my DC pension till early 2027, possibly longer if I pick up some consulting type work.

I think my pension funds have lost about 15k in the past week…..I try not to think about it too much.

I’ll be 60 in February and while I don’t think I’ll get bored there are a few part time work things on my radar, possibly a few days a month type stuff.

We finished end of March and it's been great since then. Main thing is the absence of pressure on our time from work and not having to jam things we enjoy in at the weekend. As per Tracy above, we've been pretty busy but it's stuff we want to do .

We went to Ireland at the start of June and were anticipating a return to London in September, now it's we might pop back in January.

Neither of us miss work and we have both been offered bits and pieces. I'm doing a week or so on an unfinished project and wish I hadn't volunteered but Mrs K turned down the opportunity for some consultant work this week.

Financially out goings have dropped substantially living off savings and investments so far.

What pocket money jobs do people have?

Is a days pay for collecting supermarket trollies worth getting out of bed for?

I think this will depend entirely on individual situations, and how much you may need/want to fill any gaps to savings and pensions.

I have a few pals who do supermarket delivery driving a couple of days a week. Adds up to a decent enough tax free income (about £1k a month I think), assuming you’re not using up tax free allowances on pension drawdown.

I’d also be really interested in hearing what pension-top-up, part-time jobs people are doing. And how that’s working out.

i took VR at 60 - I have a mix of final salary and DC a pension. Because of the VR i don't intend to draw on my pension for at least 12 months - I've made sure we have no debt - House, car etc all paid for. I am not intending to work - if I did it would only be part time. Like others you still feel pretty exposed with a DC pension to the vagaries' of the stock markets. Unless of course "our Rach" changes all this on budget day in a couple of weeks.....

I’d also be really interested in hearing what pension-top-up, part-time jobs people are doing. And how that’s working out.

no pension top up here......... and no intention of doing any work.... far too buy.

5 grandkids and a couple of bikes to keep me occupied.

I don't have a pension as such.... Have all my monies invested in various funds (via Hargreaves Lansdown) and I plan on releasing some of that as and when I need it.

Have always been self employed so no employer contribution scheme for me.

I could have paid into the German pension system for self employed but my accountant told me years ago not to bother as you pay way more in that you get out. He told me bung any spare cash into my investments.

I know I'm at the whim of the markets. I'll move some money into less risky funds as the years go by, but I'm 43 so still capable of working if I chose to. Using a compound interest calculator I should be on for a little over a million in ten years time.

Am I at a disadvantage not having a pension?

no pension top up here......... and no intention of doing any work.... far too buy.

Ah interesting. You posted something a while back that I took to mean that you were doing some Amazon delivery driving. Impressed to hear it ain't so!

Ah interesting. You posted something a while back that I took to mean that you were doing some Amazon delivery driving. Impressed to hear it ain't so!

no,i think i posted saying you could earn a couple of quid per day doing this.

far too busy for work me. #lessmoneymoretime

I think Amazon drivers get around £200 a day…..but you need to have car, insurance etc which will eat into the headline figure

Depend on where you live, but in most rural areas there’s very little part time work here that pays above minimum wage. There’s plenty of cleaning/housekeeping work at weekends for holiday rental changeovers for cash in hand if you don’t mind scraping shit off a carpet occasionally for half the year.

I work part time in a local shop and get paid at the living wage rate, plus I’ve also got a design and print business where we sell product through local shops - it’s taken 7 years to grow sales/reasonably profitable and this year we will be able to pay Mrs DB up to the tax-free allowance. I’m hoping that I can sell that business on in a few years when I start drawing my pension - should pay for a new car or a decent holiday. Also means that we’re not drawing down on savings as much, leaving pensions and investments intact - a lot can still happen in 4 years though.

The last few years has also shown that we can live within relatively modest means - certainly lower than what some of those lifestyle predictors estimate - the important thing being that everything’s paid off, no mortgage, loans, car etc.

Am I at a disadvantage not having a pension?

Not since annuity pensions got replaced by pension pots. However:

If you haven't already done so sign up to make voluntary contributions to the UK state pension.

Depending on whether you can pay class 2 (working and paying social Security abroad) or class 3 (inactive abroad) it costs sweet **** all or under a grand a year. You need 35 years contributions for the full state pension. I'll end up with 29/35 having been misinformed back in the day and fobbed off for a few years. Requirement is already having three years contributions before leaving the UK so check your pension record on line and if you have apply. There are some rules around dates and moving out to work which in my case I proved with my last P45 and and having applied for an E111 (and a French employment record that they didn't ask to see).

hhhhhhhhhhhhhhhhhhhhhhhhhhhh