UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

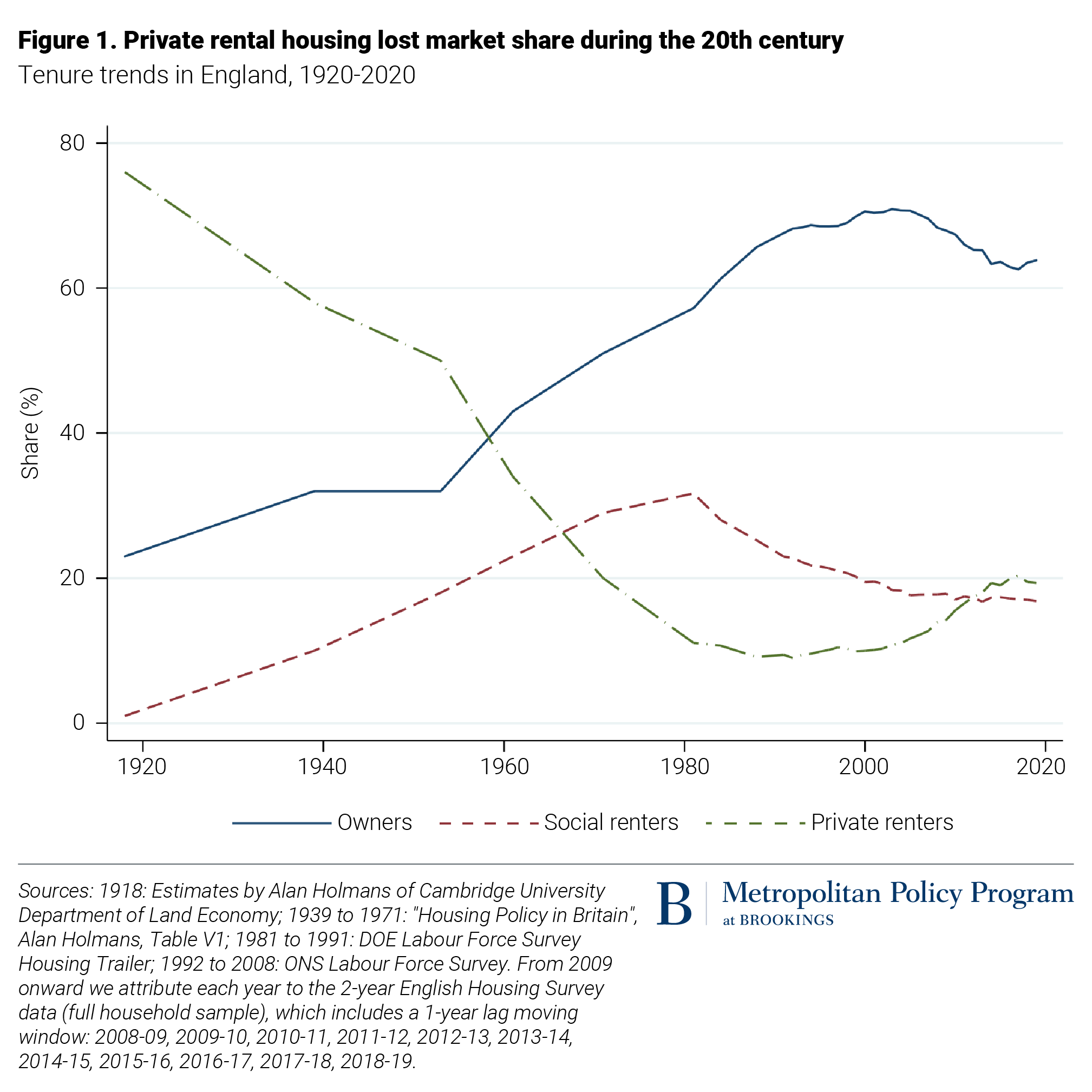

Just noticed you can clearly see in that graph where Right To Buy kicks in - that sudden boost in the owner-occupiers in the early 80's, mirrored by a corresponding drop in social renters. And then it all ran out of steam in the 90's

True… but affordable for who?..... landlords

Yea, that's another problem.

My original thoughts were along these lines, 2 incomes has become the norm and as a result the multiple of income to mortgage amount has gone form 3x to 9x.

Yep – when my dad was 27 (in 1979), he was earning roughly a teacher’s salary, and bought a 3-bed house with a garden in a decent part of town for about 3 years’ wages. He had left school with a couple of O levels and done an apprenticeship at the post office.

When I was 27, a similar house was more like 8 years of a teacher’s wage. And now it’s probably over 10 years.

Which in itself creates a chicken and egg scenario with landlords. Are landlords pricing people out of the market, or is the market just reflecting what people can afford, but as a result of that they can't afford it until they're settled down as a couple? So you end up with people renting longer, which drives demand for rentals?

I don't think it's right, or good for the economy that house prices are this high, but there's an argument that you're seeing a correlation and implying a causation.

Totally anecdotal, but we're looking as first time buyers right now and numerous nice, finished houses that we've bid on have gone to cash buyers way over asking. To me that says either large portfolio landlords, or inheritance buys.

Had a look at rightmove history yesterday and spotted a 2020 newbuild that sold this year for £110k over original price. £110,000 in 2 years! We knew things had got expensive but when you really look at the upticks in numbers it certainly feels like a bubble ready to burst. Every house we look at is the most expensive to have ever sold on a street, by at least £30k

That graph really brings it home that renters are staying in rented homes for far longer before buying with lots never making the jump.

So the reality is that household incomes have doubled, and as almost all that extra wasn’t needed for non-housing costs we’ve ended up in a situation where the new normal is to spend 75% of two incomes on a house, not 50% of one, which roughly corelates to house prices trebling relative to average earnings.

Which really screws over the likes of me who are single and only have one income.

Are landlords pricing people out of the market, or is the market just reflecting what people can afford, but as a result of that they can’t afford it until they’re settled down as a couple? So you end up with people renting longer, which drives demand for rentals?

Landlords are pricing on the assumption that a couple will move in, single people are being driven out of the market.

To me that says either large portfolio landlords, or inheritance buys.

Or downsizers moving up from the South East!

Are landlords pricing people out of the market, or is the market just reflecting what people can afford, but as a result of that they can’t afford it until they’re settled down as a couple? So you end up with people renting longer, which drives demand for rentals?

Both, I'd imagine. Because in addition, the higher rental prices are, the longer it takes people to save up a deposit, so the longer they'll need to rent, which drives demand for rentals, which pushes the rental prices up, which makes it more attractive to become a landlord....!

So you end up with people renting longer, which drives demand for rentals?

A major impact is the need for large deposits. Which can be tricky if you are paying out large amounts in rent. Whereas a landlord can ratchet up by remortgaging for the increased value and stick the deposit down on the next one. In theory risky but when you have the government desperate to prop up the values it becomes less so.

The problem with housing as a market is you dont really have a choice in the matter. You cant really chose to not bother.

We have some houses near us that sold in the last year - for over asking price, on average over 20%, a few 30% over asking, one for 38%(!) over..

Now showing negative / slowing house prices.

https://www.zoopla.co.uk/property/uprn/122006187/

https://www.zoopla.co.uk/property/uprn/122003512/

https://www.zoopla.co.uk/property/uprn/124024739/

https://www.zoopla.co.uk/property/uprn/122004758/

Or downsizers moving up from the South East!

Or, as we have, families moving north pre and post-pandemic.

An example: We have one neighbouring family who lived in London, looked at what are the best state schools in Scotland were. Dunblane High School was the answer. So they moved here having never even visited until the house search, offered 25% over asking in 2019 and now aim to get their toddler into said 'best' state school in Scotland.

2022 and some people here are still claiming housing is affordable. Just look at wage stagnation vs average deposit size, multiplies of income required and average mortgage length.

So the reality is that household incomes have doubled, and as almost all that extra wasn’t needed for non-housing costs we’ve ended up in a situation where the new normal is to spend 75% of two incomes on a house, not 50% of one, which roughly corelates to house prices trebling relative to average earnings.

You are completely missing the greed of BTL and the rigged credit rating system.

2022 and some people here are still claiming housing is affordable.

It can still be done - my niece is just buying her first house, she's early 30s, single and has a good but not mega job. House is in Exmouth too so not some grim ex industrial town.

2022 and some people here are still claiming housing is affordable. Just look at wage stagnation vs average deposit size, multiplies of income required and average mortgage length.

Except you missed the bit where I pointed out that household incomes doubled since the start of that graph it switched from the default of a man going to work and a housewife to two full time incomes. Which means that any comparison of prices/deposits Vs incomes is completely irrelevant as it's not how people live anymore.

It's inevitably going to lead to massive inflation in the one thing we all buy but where supply is restricted because we're* all trying to buy the same houses, but have* many times the budgets to do it that our parents had.

The only way that will reverse is if the cost of everything else goes up meaning those 2-income households have less money to compete with each other in the housing market ................

*collectively as a population. You or I might not completely fit that description, but as a population the average is now a two income household which means that the money left over after food, clothes and everything else is much higher, so it get's spent on rent/saving for a deposit/paying a mortgage.

It certainly feels like some kind of turbulence is kicking up a notch. I'm just hoping we can exchange very soon and be moved. For our example, we've sold in a very popular south Manchester area, and sold for asking price. We were actually a bit on the cheap side compared to similar properties. One EA wanted us to put it on £40k above what it sold. Some of the new build sites we went to view have called us recently. We didn't think those plots would be available to us (we have to have sold ours before reserving on many sites). Things definitely seemed to have stalled in some areas.

2022 and some people here are still claiming housing is affordable.

I’ve not noticed this, other than pointing out that some people are buying them and hence ipso facto they are ‘affordable’.

Pretty much everyone agrees, that housing is ridiculously expensive. I would argue though, that whilst it may be worse than ever, it was not in any way easily affordable in 60’s, 70’s or 80’s… as some appear to suggest.

My parents bought a 2 bedroomed house when they married in their mid twenties. On one wage. However, I rarely saw my father as he worked 70+ hours every week. When I did see him, he was so irritable I wished I didn’t. We had an outdoor toilet. My friends didn’t even have a bathroom, but used a tin bath in their living room - once a week.

My wife and I were both 28 when we bought our first, rundown 2 bed flat. Having scrimped and saved for years to get the deposit. Interest rates were 15% iirc.

Recently my eldest daughter bought her flat in her mid 20’s having scrimped for 4 years, living in a multi-shared house.

My youngest daughter, has been fortunate enough to inherit a modest amount of money, that has enabled her (in her mid 20’s) to buy a house. She has been lucky. Like what I presume is an increasing number of young people, reaping the benefits of grandparents who bought in the 60’s and 70’s.

The situation now is dire, but the people who bought before, or are moving from ‘down South’, are not to blame imho. It is successive governments and those who voted for them.

I could never bring myself to buy to let, as it must surely inflate prices. But, I find it hard to totally condemn those that do, rather than see their meagre savings vanish before them due to inflation.

Are you really trying to say house prices are high because more women are working and so people now have more money to spend? Apart from the ridiculousness of this logic - have you seen the price of childcare? People with high rent do not have savings.

I’ve not noticed this,

Erm.. you go on to make an argument that affordability has not gotten worse.

The truth is, the home has been turned into a financial product used to enrich people that are deemed "credit worthy"

I could never bring myself to buy to let, as it must surely inflate prices. But, I find it hard to totally condemn those that do, rather than see their meagre savings vanish before them due to inflation.

The issue with BTL is you can take a loan out to do it and be massively leveraged.

So you start with £10k, buy a £100k asset, then make your 7% form it and pay 2% interest on the loan.

So in terms of making a return on your "savings" they're making 50% ROI (in that example).

Then you wait a year or two for prices to go up 10%, cash out that 10% by remortgaging and repeat.

I'd rather see the sector limited to actual bigger businesses (very non-lefty of me) by limiting the balance sheets of landlords to for example 50% debt. That would realistically (in my mind anyway) mean pension funds owning tower blocks rather than individuals buying up individual houses.

Apart from the ridiculousness of this logic

You mean, simple statement of fact?

The truth is, the home has been turned into a financial product used to enrich people that are deemed “credit worthy”

You've said this twice now, but with the exception of people who really shouldn't be allowed anywhere near a credit card, who doesn't have a good enough credit rating to get a mortgage? I had to get a credit card, use it for nothing other than to get a phone contract, and that was enough to get me a mortgage. It's hardly 'rigged' if it's that easy to play the game that a £10/month sim card was enough.

You’ve said this twice now, but with the exception of people who really shouldn’t be allowed anywhere near a credit card, who doesn’t have a good enough credit rating to get a mortgage?

Absolutely oblivious to the situation. Plenty of people pay fair higher rent than they could borrow as a mortgage.

Are you really trying to say house prices are high because more women are working and so people now have more money to spend?

it's one of the factors. There is no single reason. The emergence/popularity of BTL mortgages in the 1990s and 2000s, selling off of social housing stock and plenty of other factors all also contributed.

Absolutely oblivious to the situation. Plenty of people pay fair higher rent than they could borrow as a mortgage.

Because interest rates have been <2% for a decade now. Watch that collapse if rates rise. Banks quite rightly want to make sure you can afford the repayments if they revert back to historical averages.

And if everyone can then afford a more expensive house, then prices would just go up again. Because that's exactly what happens every time 'affordability' increases, cut the stamp duty, prices rocket, interest rates drop, prices rocket, wages go up, prices rocket.

The only way you'd break that cycle is to massively oversupply housing to remove the link between what people can afford to pay and it's value, which is never likely to happen again.

My opinion is relax/reduce planning law to increase the volume of houses built, but impose stricter controls on the building process to improve the quality.

This should improve supply and reduce speculation.

As a homeowner, I have no problem with interest rates rising if it means house prices will fall. The commoditization of the home is the problem, all these other factors are just symptoms of this. I agree we need to build more housing, in particular, social, but let's not pretend greed has nothing to do with high house prices.

but let’s not pretend greed has nothing to do with high house prices.

But once you're a home owner, you've got no real influence on it's value. The value will always be determined by the almost inevitable bidding war between buyers.

Call it greed all you want, but people need houses and as a result will pay whatever they an afford unless there's an oversupply of housing stock.

As a homeowner, I have no problem with interest rates rising

I'm going to infer this puts you more "out of touch" with the younger end of the market than most, because most of us are mortgaged to the hilt to afford anything. I'm dreading my next mortgage renewal.

If you are mortgaged to the hilt (I am) then you aren’t really a homeowner.

If you are mortgaged to the hilt (I am) then you aren’t really a homeowner.

Fair point, don't make it even more depressing 😂

I’m going to infer this puts you more “out of touch” with the younger end of the market

Nonsense, I am thinking of my kids and society in general. What do you think is going to happen when generation rent gets to retirement age?

The greed is not from people living in their own homes, it's from BTL, second homeowners, holiday homeowners, unscrupulous student landlords, foreign investors who don't even bother renting out their properties and politicians who prop it up all up time and time again because they have their own property portfolios.

Nonsense, I am thinking of my kids and society in general. What do you think is going to happen when generation rent gets to retirement age?

Hysteria aside, "generation rent" as we've been called, do generally seem to eventually get on the housing ladder. It's not easy, but you're ideas of increasing loan to income ratios, and crippling us with interest rate rises aren't exactly going to solve it for your kids are they.

Look at the graph posted earlier, the proportion renting and owning leveled off 2012 ish, so 'something' is definitely happening, depending on how it oscillates over the next 50 years or so you could argue that stagnation goes back as far as 1990. Maybe it'll revert back to going upwards, maybe ~30% is the level of rented housing the market needs after all. Plenty of young people (from my experience anyway) move around a lot, spend time living/working in different cities, before settling down. Buying doesn't suit a lot of people at that age.

And without a reform of stamp duty* it never will. So there needs to be some level of renting going on.

*my proposal, abolish it as a transaction tax and make it a property tax. Effectively double council tax. The net result would be to encourage more moves as people retire and rather than thinking "I've paid off this nice 4 bed house so I'll keep it" they'll have to seriously consider whether they should downsize and let another growing family use it.

House prices coming down or wages going up are the only things that will solve it. To do this requires a complete change in mindset and policy. It's not fine because people get on the housing ladder later, they are a huge deficient by that point and probably have taken out a massive, 30, 35 hell soon to be a 50-year mortgage to do so.

I'm not sure that wages going up really would solve it. It would allow people to bid that bit more to get the house they really want. which would push prices back up again.

I think a large increase in housing supply would go a long way to sorting things out though.

House prices coming down or wages going up are the only things that will solve it.

Watch what happens with 2 years of 10% inflation and rising rates, looks like you're only one looking forward to it 🤷♂️

Realistically though people REALLY want a house, and will pay everything they can afford for it if they have to. We're taking out >25yr mortgages based on 2 incomes because that's what makes it affordable. If I didn't, the next person would have done.

The problem is absolutely on the supply side of the equation, and I think altering the rental market is twiddling in the margins. A dead cat to distract from how far behind we are building new housing. Either through nimbyism or lack of infrastructure. If the rental market was as oversized as you think, then there wouldn't be parts of the country where you have to rent without even seeing the property first they go so quickly.

Build enough and the free(ish) market would erode those BTL returns, both through competition between landlords who buy them, and because landlords would compete for a smaller rental market.

House prices coming down or wages going up are the only things that will solve it.

Well the only way house prices are coming down vs wages is in a deep recession. The long term problem is demand exceeds supply.

Well the only way house prices are coming down vs wages is in a deep recession. The long term problem is demand exceeds supply.

not really there's a whole bunch of ways to make it happen, eg

1) higher interest rates

2) cgt on primary residence

3) higher tax on buying btl (currently 3%, ramp it up)

4) higher other tax\conditions on btl (harder to kick people out etc, this is already happening)

5) further borrowing restrictions (multiples of income/ability to pay etc)

6) increase supply

7) spare bedroom tax

etc etc. I'm not saying all these are fair necessarily (fairness is a funny thing anyway) - but they would all make property prices drop.

incidentally, increasing supply doesn't always work either. Places like sydney, phoenix and vancouver have space to grow (less so in vancouvers case) - but still property is in a massive bubble. If you think prices are high here try buying something in aus..

not really there’s a whole bunch of ways to make it happen, eg

Tinkering around the edges. If demand >> supply the market will push the price of the asset as high as it can go, stretching people to the max. It's not as if housing is an optional asset, like Bitcoin, people generally need somewhere to live.

The only time house prices see significant falls, in the UK, is during recessions.

increasing supply doesn’t always work either.

You sure about that? Supply / demand is one of the most basic rules of economics.

have space to grow

Which is not the same as an increase in supply. One of the problems the UK currently faces is that the combined private sector house building capacity is less than the annual increase in demand.

There are millions of renters that want to be owners, but can't afford to (despite paying more in rent than a mortgage would cost). It's not all about increasing the number of houses, but reducing the number of BTL landlords.

There are millions of renters that want to be owners, but can’t afford to (despite paying more in rent than a mortgage would cost). It’s not all about increasing the number of houses, but reducing the number of BTL landlords.

Maybe, but then you're swapping those 1:1. And therefore doing nothing for prices as for every rental sold you're generating another buyer. It might work for some people, but not everyone.

And it achieves nothing for those renting bedsits, HMOs, living with friends, family, or flats that were never big enough to be viable long term anyway.

Tinkering around the edges. If demand >> supply the market will push the price of the asset as high as it can go, stretching people to the max. It’s not as if housing is an optional asset, like Bitcoin, people generally need somewhere to live.

The only time house prices see significant falls, in the UK, is during recessions.

the only time they have seen drops in the past is because of that, sure. but prices aren't supply/demand in the way you think, as the demand side is effectively "the amount of spare cash people have", rather than just the number of people who want them. Make it tougher to own btl, and you reduce demand, but supply stays constant.

if you put a 50% capital gains tax on primary properties, price rises would grind to a halt really really fast.

Easiest way to reduce prices is limit borrowing, job jobbed. Then need to address the supply issues but to an extent excess credit drives the devolpers towards lower density premium housing. Reduce what people can borrow and expect to see a lot more affordable higher density housing.