UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

Just banning BTL or changing tax doesn't increase supply - you'd actually reduce supply and make the housing problem worse. Not everyone wants to buy a house or is at the stage in their life when it makes sense etc. A good supply of rental properties is good for the economy as it facilitates movement of labour to where demand is greatest.

It's a simple equation of demand outstripping supply. There isn't room to build the a city the size of Portsmouth every year and it's not just about building houses. It's building schools, hospitals and everything else that is required.

The country is too densely populated and the situation will get worse and worse. It's not unique to the UK - there are housing crises in many places.

There are just too many damn people in the world and too many of them who would like to make the UK their home.

Building houses is expensive, because land is expensive as is building decent homes, as they require skilled tradesmen, who get paid well...and they are build from expensive materials. This isn't the 1890's when there was abundant land to be built on, by a skilled workforce who were paid nearly nothing by modern standards.

Obviously building more affordable housing is important. I do find the social housing thing a bit perplexing - I know a few people who have historically been eligible for it, but then keep the house and the subsidised rent long term even though they are now on decent incomes. I’m not sure how this affects the market, or even if it does at all but it seems strange.

TH asserting that renting could be cheaper than buying is absurd. The house still needs to bought and a return made on it in a reasonable timescale otherwise the investor wouldn’t invest

Here is the rub of the problem... property is viewed as a safe investment, and always (almost) goesone way in value. This has to be protected even tho' it's a bad outcome for a lot of people and that number will grow, because that's how it works. It'll take a brave man to flatten that growth out tho' it will do so itself at some point..

I'd answer to Joe above that most of that isn't true. Lots of places are densely populated , and that the problem with the UK is both price of property being disproportionately high, and concentration of wealth in the SE distorting the UK market. Luckily the UK isn't a country with high immigration or it would be even worse

There isn’t room to build the a city the size of Portsmouth every year and it’s not just about building houses. It’s building schools, hospitals and everything else that is required.

The country is too densely populated and the situation will get worse and worse.

There is loads of room if there was the will to build more. If we had the population density of Singapore, a functional country, then the entire population of China, USA and Russia could live here. That's an extreme example but we can certainly comfortably accommodate quite a few more people and have the space for a lot more houses.

TH asserting that renting could be cheaper than buying is absurd. The house still needs to bought and a return made on it in a reasonable timescale otherwise the investor wouldn’t invest

Unless it's an old house.

I lived on a private Estate for years and rents are below market. Even now.

I like the idea, I've owned my own home for 4 years and in my early 30s and have no intention of ever moving. So I can remortgage to 100 years, reduce my payment down to zip, now freeing up loads of cash to pay into a pension/early retirement fund. And the house is there already set up for my kids when I pass. What's not to like.

I'm essentially a long term, very cheap rent paying tenant in my own home, with a guarantee my spawn will also be ok.

Andylc makes a good point.

I remember seeing Bob Crow on Question Time a few years ago, going on about how he still lives in a council house as it "keeps him in touch with the people".

He was earning £80k+. Bollocks to keeping in touch, it's denying a house to someone who actually needs it, at the expense of the taxpayer who is subsidising the accommodation of an already very wealthy man.

A massive part of problem is people seeing houses as ‘investments’ or sources of income.

But the majority view their own home as a home.

My experiance of social housing was a house that just about did what we needed it to do. Albe it in an area that was inconvienance to live in. Fairly troublesome and ergo there was an incentive to get out of there asap...

Which is why right to buy in principle is a good idea as long as the money from the rent and sale of properties is channelled back into building more houses. As long as the rent paid and the purchase price cover the cost to build new the system refreshes the housing stock without blocking social housing for those who need it and doesn't turf people out of their homes for many years.

Previous implementation of right to buy was diabolical, Thatcher actively banned the sale money from being reinvested. Social housing should not be seen as life long (for most people), it should be seen as a stepping stone to home ownership accepting their will always be a need for good social housing and some people will need lifelong support.

Obviously building more affordable housing is important. I do find the social housing thing a bit perplexing – I know a few people who have historically been eligible for it, but then keep the house and the subsidised rent long term even though they are now on decent incomes. I’m not sure how this affects the market, or even if it does at all but it seems strange.

Ok, there's a bit of misinformation here. Rents are only 'subsidised' if you're eligible for some kind of assistance (housing benefit for example) otherwise the rent is unsubsidised, ie you pay it all yourself. Not everyone who lives in social housing is on benefits.

Social housing should not be seen as life long

Why on Earth not? Done properly it provides secure housing for people and jobs for loads of different trades.

Removal of the profit element is subsidised over the free market.

No matter how you cut it social housing is appealing from a cost pov.....

Being put 10 floors up in a tower block less so.

Which is why right to buy in principle is a good idea as long as the money from the rent and sale of properties is channelled back into building more houses.

Except its not as easy as just building more houses, there's planning, obtaining land and getting nimbys to agree to more social housing near them, before you even start on the actual job of building houses.

It’s just a dead cat from the Dead Cat Party.

I’ve heard talk of 50, and now 100 year mortgages. Unless the interest rate is halved for 50 years, and quartered for 100 years, then the repayments are only going to reduced a small amount. It would only be the repayment part that would be reduced.

Like I said, dead cat.

Social housing is cheaper to build using direct labour and no profits and state owned brownfield sites

It does not have to be shit housing. We had some very good stock before it was all sold. Rest of Europe has good social housing. What makes us so special that we cannot? A shit scheme in Edinburgh was flattened and nice social housing built instead

We had some very good stock before it was all sold.

I do wish folk would stop harping on about the great sell.

Of the stuff they sold a huge %age would have been massively outdated by now and required significant refit and still be fairly shit. - I live in such a case.

1950s corporation housing . Minimal insulation and design doesn't allow for much retrofit.

It's such that my neighbours house is going to auction rather than being retained in social housing stock.......

And it can be a nice house but if it's in an inconvienance area it's still a shit house....you get minimal say in social housing as to where your going to live like it or lump it if your lucky enough to be offered

Social housing is cheaper to build using direct labour and no profits and state owned brownfield sites

Lastly are those facts or assumptions.....

The rest of Europe, bar maybe the Netherlands have inadequate social housing and no real forward plan on how to achieve this, they also have the same house price and private rental concerns, so it’s not just a UK issue, or easily solved

I’ve heard talk of 50, and now 100 year mortgages. Unless the interest rate is halved for 50 years, and quartered for 100 years, then the repayments are only going to reduced a small amount. It would only be the repayment part that would be reduced.

But owning, even with a mortgage, Harold sof advantages over renting. I have a mortgage but I can build an extension if I want, change the windows, new bathroom, even something like get a cat without asking anyone. Well, ok,I still need permission for the extension but not from a landlord.

Monthly costs being equal a mortgage is still better than rent.

The other advantage of extra long mortgages is that inflation erodes the debt. If your rent or interest only mortgage is £500 a month today, in 40 years time the mortgage is still only £500 but the rent would be £1500. The difference would easily cover both covering bills, and paying off the principal. Most people can expect to live 50 years after they turn 30, so it's cheaper to have a house, even without considering the value of the asset you have for free at the end

But as others have said, if we do see 50 year mortgages, it can't be the start of another house price increase, too many times we've seen schemes and changes that should improve the market for buyers at the lower end, but all too often this is eroded away after a couple of years, as it just feeds the market yet again.

We do need a reduction in house prices, not a crash, as all that does is put millions of homeowners into potentially serious financial issues with their asset to debt ratio and ability to remortgage, and with a crash credit would become harder, so those trying to get a mortgage would probably lose out on favourable rates, or need more deposit, but there has to be a happy medium.

There are many ways to skin this particular cat. However, even if the government (the tories specifically, but applies to the Labour Party too I guess) does commit to doing something worthwhile to address the issue there will be a huge number of self-interests going on, some party donors company will be making a mint whilst churning-out thousands of terrible affordable/social properties (probably on flood plains, on on a postage stamp between two dual carriageways), there will be no infrastructure to support dropping thousands of families into a particular postcode, the local authority crippled with costs trying to maintain thousands of poorly built houses, which will subsequently deteriorate to ghetto status within 10 years.

The sad reality is that until we address the decline in standards of UK politics - we cannot trust the same people (or type of people) who deliberately broke the system, to fix it.

I said before that the Conservative party is effectively now the "UK GOP" - Nobody anywhere near power has absolutely any interest in "fixing" anything that would genuinely improve life for the majority of the UK population. Even on those issues that would both deliver genuine improvements for people AND be vote winners (new hospitals anyone?) - we have accepted a reality where there is no accountability to deliver after the votes have been cast.

Personally, I am hopeful that covid shifting office-workers to a wfh model by default will result in a huge number of benefits - being able to work for a business based in the southeast, whist living in rural Wales (for example) being a huge one.

However, you have that absolute tit Jacob-Rees Mogg setting the government's policy that this must be prevented, and we must squander this enormous opportunity - why? So that the status quo can not only continue, but funnel even more money into the pockets of their chums.

Sorry - bit of a rant - but thinking that the current crop of bastards in Westminster (of all colours) are going to deliver anything different than a continued erosion of quality of life for the average person in the street, is just a fantasy.

And me, no will from the top to sort the problem other than coming up with slogans.

The rental market is getting worse.

Surely we're in danger of reaching the point where people who are renting are unable to make the jump to home ownership as it'll be impossible to even consider saving up a deposit, that's if we're not already there!

Well the requirement for borrowers to prove they can cope with a 3% increase in base rate has been dropped from today. It might not have an immediate effect due to other factors but when the market next starts growing in the double digit range it'll certainly have an effect. Suddenly people will have less of a barrier on how much they can borrow so sellers will up their prices accordingly.

50 year mortgages with fewer restrictions to protect people from overextending? It can only go one way.

House prices up by 11% this year, no end of this rise in site, we don't really learn much even when you have a financial meltdown like in 2007/08, we're way past madness now, and the sad truth is folk love it, being able to have this fake wealth, ah well, just another thing for our kids to fix when we're all gone.

https://www.bbc.co.uk/news/business-62390578

I cannot fathom how prices continue to rise – are people trying to get their moves completed and mortgage rates fixed before the steady increase in rates that will inevitably happen soon so are willing to pay more and more?

I have a colleague, possibly around mid 50's-60, very well paid, who said he'll never pay off his mortgage, ever. Now he must have a lovely house, but this sounds a bit mad to me, as someone who paid off the mortgage before I was 50 ?

Other issues are houses being 'held' empty to pay for care fees. Just about to sell MIL's 4 bed detached, that's been empty 3 years as it was much cheaper to have a council charge on the house, rather than sell and pay for a care home. House is now being sold to pay fees, but it's been an empty family house for 3 years.

Is he on an interest only mortgage??

I've no idea but it just seems odd - I suppose if he's relying on house prices to increase and doesn't need it to fund care homes ? It's a way of having a super posh home above your earning potential ?

I'm amazed that he was able to get a mortgage that would not be considered repayable by the bank. Surely they'd have set out a payment schedule that covered it?

It’s a way of having a super posh home above your earning potential ?

Or has a modest home that meets his needs but circumstances in his life mean that he doesn't think it will be fully paid for in his lifetime?

I’m amazed that he was able to get a mortgage that would not be considered repayable by the bank. Surely they’d have set out a payment schedule that covered it?

There are some niche 'lifetime' mortgages available that can see you into very old age but the lender maintains a security on the property.

I’m amazed that he was able to get a mortgage that would not be considered repayable by the bank. Surely they’d have set out a payment schedule that covered it?

Because of his age?

Someone with a decent pension, especially DB has a guaranteed income for life.

I’ve no idea but it just seems odd – I suppose if he’s relying on house prices to increase and doesn’t need it to fund care homes ? It’s a way of having a super posh home above your earning potential ?

Both of the above? Also inheritance tax blag?

If he's on a cheap interest only mortgage, then perhaps he's putting the rest of the money he would otherwise spend on the mortgage into his care home/retirement fund?

I don't know him well enough to ask. He'll have a good pension ! Just seems a really strange comment he made. Based in the North, but 'home' is Brighton, commutes and stays over.

Just seems a really strange comment he made.

Perhaps he was just having a shit day?

I cannot fathom how prices continue to rise – are people trying to get their moves completed and mortgage rates fixed before the steady increase in rates that will inevitably happen soon so are willing to pay more and more?

Constrain supply below demand and prices normally rise. Lower number of transactions means you need less people able to afford 'a bit more' to push the stats up.

A strong labour market and limited housing stock helped to boost UK house price annual growth by double digits in July, despite rising interest rates, high inflation and lower affordability.

Housing stock remains low, with the average number of properties on sale per surveyor at a 40-year low, and both the effect of inflation running at a 40-year high of 9.4 per cent and record low consumer confidence were highlighted by a cooling of mortgage transactions managed by Nationwide.

https://www.ft.com/content/782987d0-732e-4620-ad85-ab87c6494123

How anyone young is supposed to find money to save for a deposit independently right now is frightening.

The assault on the young continues, a few generations ago you could reasonably expect to own a home in your 20s, that you could afford to heat, get a university degree without 50k of debt at double the market interest rate and support a family with only one of you working.

Riots are coming, make no mistake.

Perhaps interest rates and their relation to equity should be inverted. That way, those with the most, benefit the least at the point when they can easily afford it.

Like tax, but for mortgage interest.

Riots are coming, make no mistake.

I also think we're in a bit of a 'how to boil a frog' situation.

Long term we will hit boiling point - and as well as protest, I suspect we will still see a huge challenge in the housing market.

It sure was a good time for Priti Patel (only in office because of Brexit) to push through laws outlawing protest. Not what you might call a coincidence.

The assault on the young continues, a few generations ago you could reasonably expect to own a home in your 20s, that you could afford to heat, get a university degree without 50k of debt at double the market interest rate and support a family with only one of you working.

In an odd way it must be affordable though, otherwise no one would buy them and it would have collapsed already.

I don't think anyone really want's to go back to the days when women didn't work. So the reality is that household incomes have doubled, and as almost all that extra wasn't needed for non-housing costs we've ended up in a situation where the new normal is to spend 75% of two incomes on a house, not 50% of one, which roughly corelates to house prices trebling relative to average earnings.

It's shit and there's no winners, but it's the fairly inevitable outcome as houses are the one thing everyone needs where there isn't an unlimited supply.

The assault on the young continues, a few generations ago you could reasonably expect to own a home in your 20s, that you could afford to heat, get a university degree without 50k of debt at double the market interest rate and support a family with only one of you working.

Yep - when my dad was 27 (in 1979), he was earning roughly a teacher's salary, and bought a 3-bed house with a garden in a decent part of town for about 3 years' wages. He had left school with a couple of O levels and done an apprenticeship at the post office.

When I was 27, a similar house was more like 8 years of a teacher's wage. And now it's probably over 10 years.

(My step FiL bought his first house in 50's in a 'new' estate in Buxton for 5 month's wages!)

And yes, now 50% of young people also pay an additional 9% on their earnings in Student Loan repayments.

I just don't see how we can continue to squeeze the young much longer.

In an odd way it must be affordable though, otherwise no one would buy them and it would have collapsed already.

True... but affordable for who?

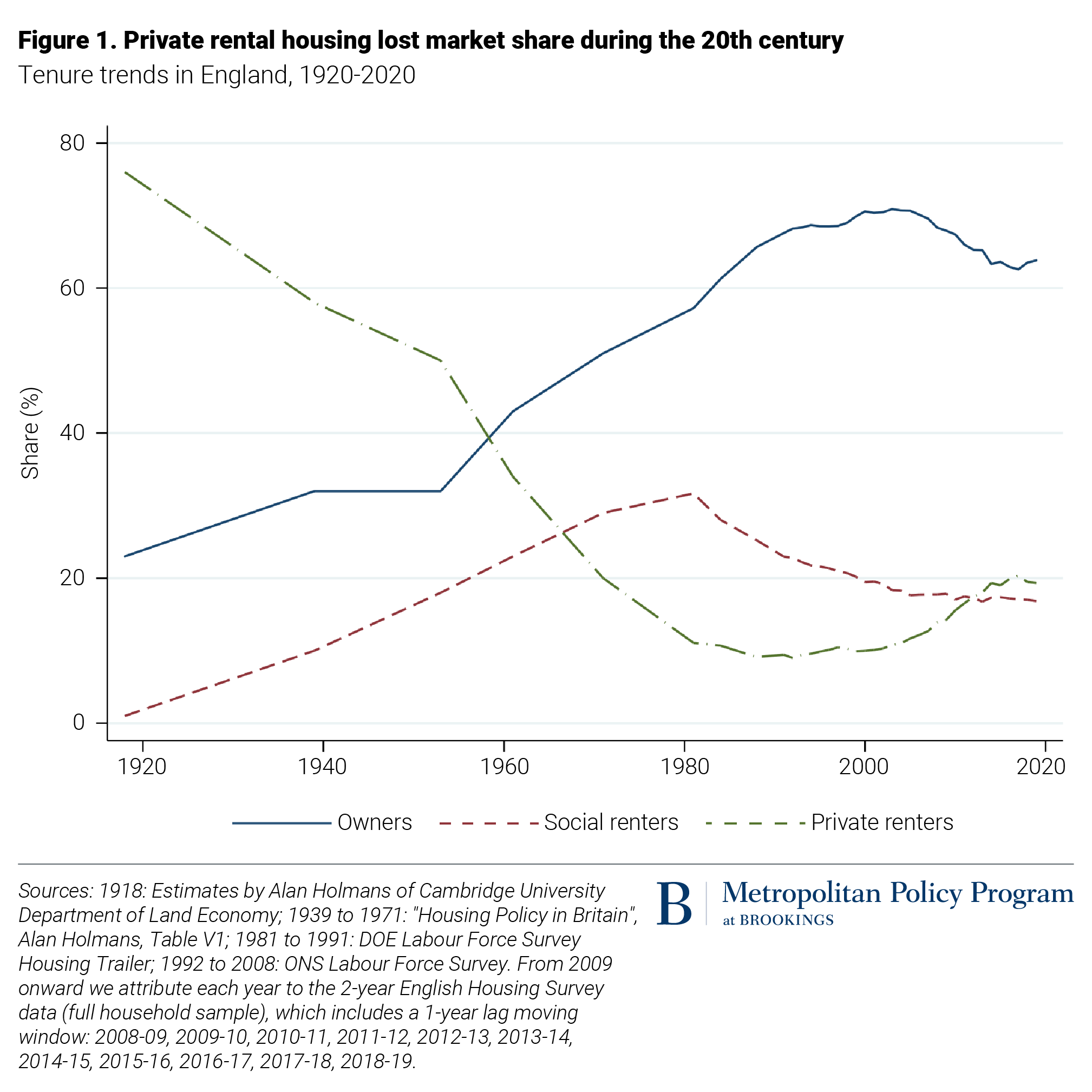

It seems that over the last 15 years, houses are increasingly being bought by landlords for private rentals. Levels of owner-occupiers are now barely above the levels of the early 80's and peaked in the mid 2000's. Makes sense: landlords are more likely to be older, asset-rich, good candidates for BTL mortgages and so on. So yeah they are 'affordable' because someone, somewhere, is affording them - but....