UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

Do the French and German foreign ministers have a long history of taking paid work on Iranian state television too?

Which is another of Corbyn's problems, what he said on Iran recently was perfectly reasonable, but because of his History of being openly anti the UK and our allies on almost every issue it just fits right into the pattern and looks like more of the same. ...but that's probably for another thread.

Only the tories can be blamed for austerity

dont forget the lib dems who despite some orange washing had a faction rather strongly in favour as well.

As for the momentum statement.

The actions taken by new labour did weaken the UK system in a way that ensured we would be hit hard by the 2008 crisis which did in turn help lead to austerity. Especially since the 2010 policy approach was to fail to provide any alternative approach to what the tories were suggesting.

or anything else that’s far more relevant to voters in this country.

You should ask some of those six formers for some help since there are some rather ****ing obvious potential implications for the UK economy with the current escalation in tensions. Just go and fill up your car to see.

She was one of the few who predicted it.

Lots of people predicted it. But that's not the same as acting to prevent it. In the dotcom bubble everyone knew it was going to burst, but people were getting cash out of it all the time. People kept inflating it because they were playing a game of see how much money you can make before the music stops.

Given a problem that we have too much debt there are various solutions.

Bit of a leading statement....

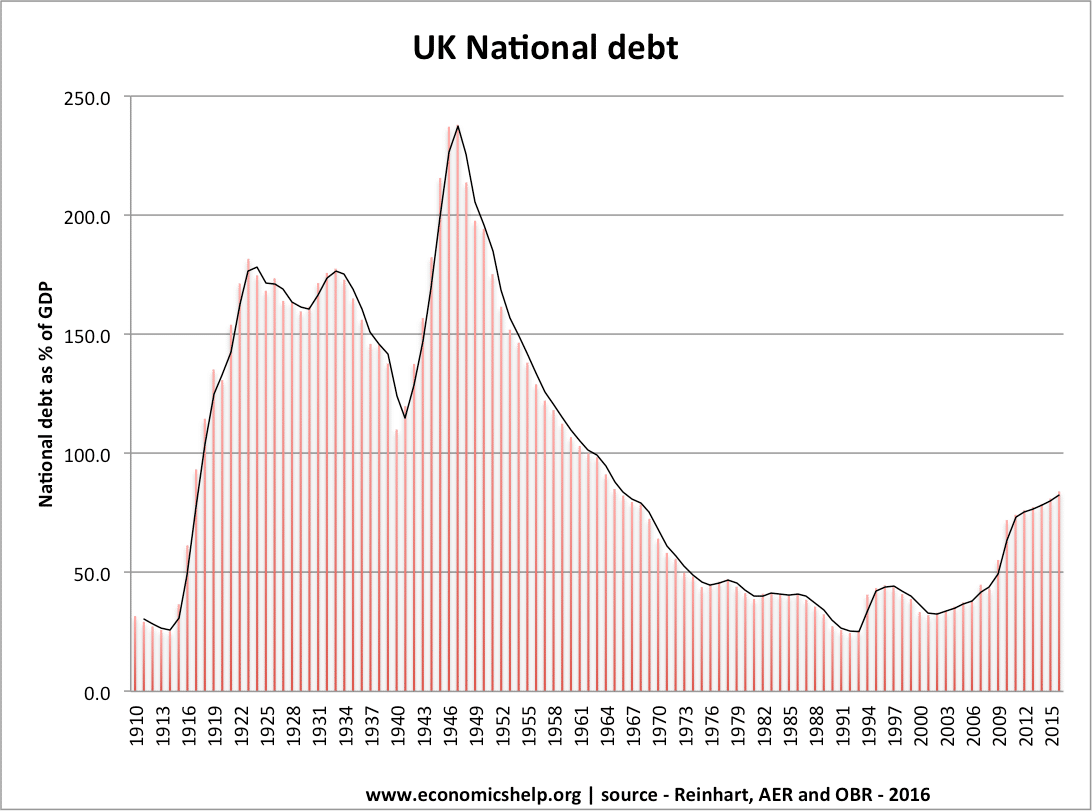

By historical standards it's not that high as a ratio of GDP..

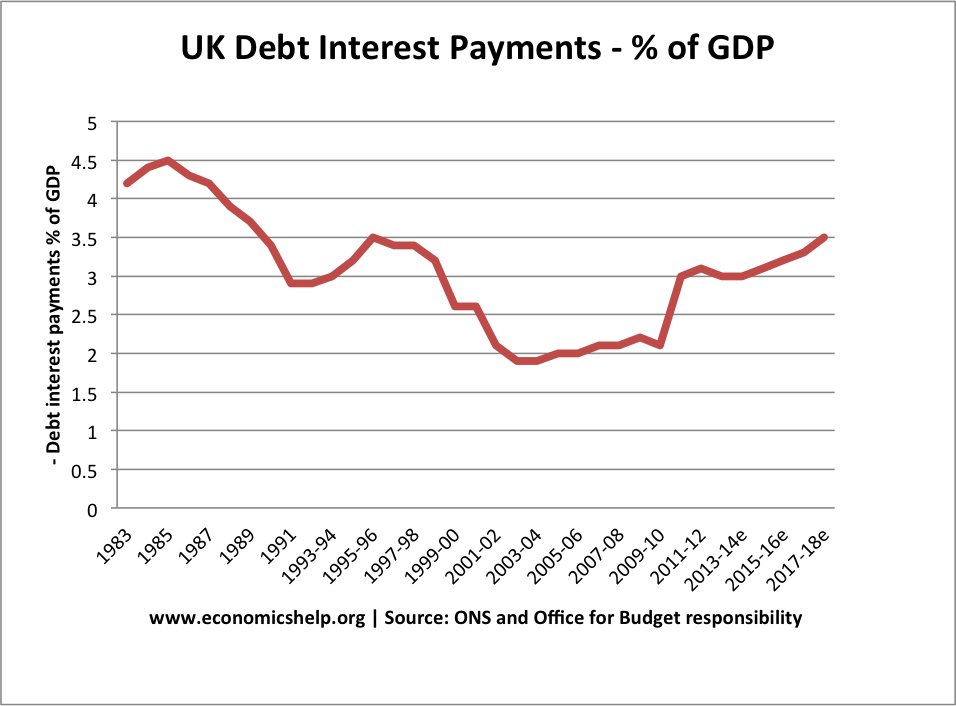

The cost of the interest as a % of GDP was affordable..

The policy of austerity, which shrinks the economy, reduces growth and GDP so actually makes the current debt worse situation worse. Osbourse and Mervyn King were moneterists rather then Keynsians and didn't believe in investing to grow your economy out of a recession. Instead they shrank the recession into a 10 year depression. There was no economic necessity or justification for it, they wanted an excuse to shrink the welfare state.

There was a BBC documentary on, not long back, detailing the run-up to the crash. One senior guy in the City referred too it collectively as 'the suspension of disbelief'. Everyone knew it was unsustainable and that it was going to end badly, but it was all a bit "don't mention the war"

It's alright with hindsight saying that the banks weren't properly regulated. It's obvious now that they weren't. But George Osbourne, as shadow chancellor, was forever banging on about the City being over-regulated. So just imagine the mess we'd have been in if we'd had a government who thought that?

Also worth remembering that the financial tools being developed were so complex that senior people in the banks didn't even understand them. So how do you effectively regulate that? Who do you send into these organisations to try and propose suitable regulation, given the massively complex and opaque nature of everything

I do have a certain sympathy with Brown as, on the surface at least, it looked like the City was the golden goose that was providing enormous amounts of tax revenue, so probably enjoyed fairly lax scrutiny as long as the money kept rolling in.

Obviously, given the subsequent enormous taxpayer-funded bailout, that's something of a moot point now, but you have to view it from how it looked pre-crash from the treasury. Hindsight is a wonderful thing

By historical standards it’s not that high as a ratio of GDP..

Not sure that graph supports that given the base line is chosen to include both world wars! It's twice as high as the average over the last 40 years. That's immense.

The cost of the interest as a % of GDP was affordable..

At current rate. If interest rates quadruple which is nearer to the historic norm?

People kept inflating it because they were playing a game of see how much money you can make before the music stops.

Especially since if you call stop before the bubble actually pops there is a risk of getting sacked since you aint making the profits others are.

The linking of austerity to the 08 banking crash is total horsedrop

Austerity has been invented by the tories because they want to neuter the councils who resist privatisation of services.

This country has more than enough cash swilling round to fund stuff properly but the tax system is so completely fudged we don't collect anything like the amounts we should. Every chancellor since Lawson and Lamont have decided to write arcane tax break laws to boost a business sector but this has just created the small armies of taxdodge services run by banks (Barclays wealth etc) to subvert these.

If we taxed stuff properly there would be money for councils, and we could chip away at the bank debt, but instead the deficit gets bigger and bigger

(Gordon probably should have gone harder in sequestering the assets of the failed UK banks in return for the bailout and definitely should have thrown the idiots in jail. He wasn't responsible for CDOs CDSs or the hubristic ramping of pricing and takeovers and risky lending. Mervyn King knew what was going on and did nothing about it, just gave a load of mealy mouthed flannel about how he wasn't responsible for the FSA even though he should have been calling out the dodgy behaviour and giving the FSA the tip-off on who to go target)

Austerity has been invented by the tories because they want to neuter the councils who resist privatisation of services.

Austerity was invented by the Tories as a meaningless phrase that gave them the look of being financially responsible whilst spending money like water.

When interest rates go up or if the economy slows [1] servicing that debt is not going to leave much spare cash for the good stuff we all want.

Cue people claiming we can reduce debt by borrowing more... Well we are borrowing more and it isn't working.

[1] Quite likely - we've had 10 years of growth, albeit modest so there's a downturn around the corner at some point. Unless people are claiming that boom and bust is *really* over this time.

outofbreath

Member

Cue people claiming we can reduce debt by borrowing more… Well we are borrowing more and it isn’t working.

Of course, it depends on what you spend the money you borrow on- not all spending leads to growth or savings. Borrowing money to buy a house so you don't have to rent, saves money. Borrowing money to upgrade a factory, increases revenue. Borrowing money to spend on hookers while you live in your rented house, doesn't.

Saying "we are borrowing more and it isn't working" doesn't really say anything about the concept of borrowing to reduce debt, it's just a comment on the people doing the borrowing and spending.

Saying “we are borrowing more and it isn’t working” doesn’t really say anything about the concept of borrowing to reduce debt, it’s just a comment on the people doing the borrowing and spending.

Well plenty of the borrowed money is going on classic Keynesian stuff like building needless Aircraft Carriers and subsidising the housing market, it's certainly not going on "less stimulating" (FWOABW) stuff like the disabled and social care for the Elderly.

When your monetary stops working all you're left with is the Fiscal and nobody can accuse the current Goverment of not getting stuck in on the fiscal side. (Ditto all the other EU countries and the USA for that matter, we've all been taking the same desperate steps since 2008.)

This stuff isn't some kind of clever new trick, it's bog standard economics and the Civil Service Economists plus everyone in Government or who is likely to be in Government is well aware of it.

Having said all that, stimulus at this stage of the cycle is deemed a very bad idea and the entire world thinks Trump is mad to try it now, so maybe the next government (of whatever complexion) won't be going down that road.

Borrowing money to spend on hookers while you live in your rented house, doesn’t.

Oh! Blast and damn it!

Thats where I’ve gone rong.. 🤷♂️

There was a BBC documentary on, not long back, detailing the run-up to the crash. One senior guy in the City referred too it collectively as ‘the suspension of disbelief’. Everyone knew it was unsustainable and that it was going to end badly, but it was all a bit “don’t mention the war”

It’s alright with hindsight saying that the banks weren’t properly regulated. It’s obvious now that they weren’t. But George Osbourne, as shadow chancellor, was forever banging on about the City being over-regulated. So just imagine the mess we’d have been in if we’d had a government who thought that?

Also worth remembering that the financial tools being developed were so complex that senior people in the banks didn’t even understand them. So how do you effectively regulate that? Who do you send into these organisations to try and propose suitable regulation, given the massively complex and opaque nature of everything

I do have a certain sympathy with Brown as, on the surface at least, it looked like the City was the golden goose that was providing enormous amounts of tax revenue, so probably enjoyed fairly lax scrutiny as long as the money kept rolling in.

Obviously, given the subsequent enormous taxpayer-funded bailout, that’s something of a moot point now, but you have to view it from how it looked pre-crash from the treasury.

I agree.

Without trying to make out I'm anything but a bit of a fan of economics.

I was working for one of RBS subsidies between 2000 and 2009. As part of a sort of test for a promotion in 2006 I was ask to write a few hundred words on the future of the UK economy over the following 10 years. I wrote that we were due a recession and housing market correction. I 'passed' but was told privately not to share my theory as it was wrong and potentially damaging.

The thing is, to lots of people the 2008 recession was solely the fault of the Banks, they gambled with other peoples money, lost and we had to bail them out, the bastards! And if we'd regulated them better it wouldn't have happened.

That sort of partly true. Make no mistake the sale of US sub-prime Mortgage products (MBS/CDO) was a scam. It's not a case that Banks were gambling with things they didn't understand as it's sometimes stated. They knew exactly what was being offered and it was a low-risk vehicle. What they didn't know, because the ratings agencies were in bed with the scammers was they were in fact very high risk, at the first sign of an economic slow-down huge amounts of them would default, worse still that would almost immediately and automatically reduce the asset security of the mortgages to below the debt - in other words "toxic".

But, the 2008 recession was caused by the exactly same thing as the previous few. Namely, we (well, the UK generally) all collectively lost the connection between income and expenditure.

How many times in the 2000s did you hear someone bore you to death about how much money they'd made from their house?

Home many times in the 2000s did you hear someone explain to you that by switching cards every years they could spend whatever they liked, and never have to pay it back?

Home many times in the 2000s did you hear someone say they'd self-certed a massive mortgage, they were going to be so rich!

Home many times in the 2000s did you read about house prices rising at multiples of inflation/wages and everyone thought it was a good thing!

When the first cracks started to appear we had to actually ask people about their income and expenditure before we lent them money for the first time. I was alarming to say the least. The 'rich' people we'd financed cars, vans, boats and whatever else to for years were actually potless. I had to explain to someone who was a bit full of himself to say the least, they he couldn't afford a new SL, in fact, he couldn't afford to keep going on the way he was. His income was pretty massive. At least £10k a month, the only problem was he spent no less than £11k a month, every month.

He blustered and got a bit embarrassed. Told me I was stupid and wrong and how his accountant put some of it as dividends, and how this rental place paid him £800 a month and that one £600 - but I was right, he thought he was rich, but he was actually deeply indebted. It was a nice ride I suppose. He spent £12-£15k a year more than he earned, but it was okay his 'portfolio' earned more than that, so he'd rack up the debt on the credit cards at 0% then re-mortgage the rental places on the 'special property magnate interest only mortgages' to pay it off and start all over again. The daft thing is that in 2019 that sounds like the stereotypical flash prick, but in 2006 that was aspirational, 'everyone' was doing to some extent. Pre-crash lots and lots of people thought, in fact knew, that you could make fortunes, way more than you're piffling salary just buying houses and selling them again. It was free money, it was never going to end and it was easy. Until it wasn't

Austerity to continue if the UK breaks up..

https://uk.mobile.reuters.com/article/amp/idUKKCN1TK324?

I thought things would be improved once the subsidy junkies were punted overboard?