UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

I'm wondering how much longer it can go on for? A family member bought her house for around 80k in 2002 and got it valued last month at almost 400k (it's a 3 bed semi in north-west England).

If you had a deccent desposit and were OK'd for a small mortgage, would you be holding off or going all out to get on "the ladder"? What are the chances of seeing an 08 style crash? Unlikely, right?

You’d need more than a decent deposit and a small mortgage to get on the property ladder at the moment. ****ing huge deposit and mortgaged until you’re dead is more like it.

It's been done to death. I doubt itll crash. It may flat line but itll never plunge low in my opinion.

Where in NW as some places have gone insane

@ duncancallum: South Liverpool. Yes, it's completely insane. I saw a 1-bed going for 180k the other day. There's a flat at the end of my dad's road. It's up for sale, gets bought, and then a few months later up for sale again but for another 10-15k.

Nope I don't reckon it will, the country is just becoming unaffordable everywhere, as opposed to the cities & SE.

Its ok though, a lot of the soon to be newly-unaffordable-for-their-residents parts of the country voted for Boris. He'll fix it. Fo' sho.

It's not just the UK, if it is a bubble, it is a global housing bubble, and if it crashes, well then all bets are off - buy gold, guns, bitcoin, and head out to the Compound for the New Order to emerge.

What can be looked at from one perspective as a UK property bubble could be seen from another angle as a devaluation of paper money.

Calculating house prices in units of gold is quite interesting. At current prices, the ratio is close to the historical average.

Our entire economy is based on house prices not crashing, if they were to crash we would be in a huge recession with interest rates going up, jobs going down and the usual crisis' that it would bring.

Worst case is house prices going down a few percent, or steadying off, it's not just a supply and demand issue that's pushing house price increases over the years, it's the market it supports and household debts that it covers.

So long as there is access to cheap.credit the can will be kicked down the road.

I don’t remember a house price crash in 2008!! We sold our house not long after that and possibly there was a small blip but nothing that reduced prices long term.

I know there’s a few on here convinced they’ll be a crash, but I just cannot see it - although I expect the current insane growth to level off! COVID didn’t cause one, nor brexit - if anything the economy is booming now. There are a huge number of new-builds going up or planned here (SE) so maybe they’ll be more competitively priced when finished, or the builders will offer help-to-buy etc. Can’t see the price of established properties dropping though, especially those in desirable locations/with outdoor space etc. What would cause it?

As long as houses are seen as investments, not homes then growth will continue apace.

Looking at it from a sterile financial perspective;

A family member bought her house for around 80k in 2002 and got it valued last month at almost 400k

Works out at an average of just below 8.5%pa return which is broadly in line with other asset classes thought the period. I would suspect therefore house prices will continue to increase at this normal* level for the foreseeable.

*it’s clearly more batshit crazy than normal but house prices is what we as a society have decreed to use as the foundation of our entire economy.

So long as there is access to cheap.credit the can will be kicked down the road.

This for me entirely. I think the whole housing shortage/lacking of building is a bit of a red herring and it's ultimately cheap credit that will make/break the housing market. But, as had been said, the whole economy seems to be unpinned by the housing market so boris will do everything to prop it up.... scary stuff

The only way I can see it happening is if a LOT of social housing is built with right to buy taken completely off the table. Part of the reason for the price of housing is the buy to let market (or investment). The better off are pricing the less well off out of home ownership, then renting housing to the less well off for unaffordable amounts of money, profiting off the fact the lower paid can't get a mortgage for the same home.

This government will never build hundreds of thousands of social housing properties. They'll continue with the lower quality "affordable" housing. In my area that equates to earning over £50k a year (top 5% of earners) to afford to buy a 2 bed terrace.

If you had a deccent desposit and were OK’d for a small mortgage, would you be holding off or going all out to get on “the ladder”? What are the chances of seeing an 08 style crash? Unlikely, right?

First recollection I have of "houses are too expensive, how long can this go on" conversations was in the mid 90s, I wonder if that person is still waiting for prices to become "affordable"

I dont see anything changing without government intervention on a massive scale or large scale economic collapse. I'd not be waiting for either of those personally.

And exactly what was the long term impact of the 08 crash, did houses suddenly become cheap?

Probably the people who’ve taken advantage of it will disagree, but along with the other privatisations that’s been an absolute disaster IMO.with right to buy taken completely off the table

No.

We've been having this question on here for as long as I've been a member....certain posters have been predicting a huge crash is just around the corner for that entire period.

The 08 'crash' was what.....nainly people on 100%+ interest only mortgages ending up in negative equity because house prices stagnated/dipped a few %. I certainly didn't lose any money on my property during that period, neither did any of our neighbours that sold around then. That was hardly a huge crash and is probably the worst case scenario that we'll see in the next few years. A global pandemic doesn't seem to have too much of a negative impact on prices, so I'm not sure what exactly will in the next few years?

Climate crisis could shake things up. Ebola pandemic would probably cause a bit of a stir I'd imagine.

It is 100% a seller's market currently....potentially leveling off ever so slightly, but that is the market that you'd be buying in to. I'd still buy personally, but if it was somewhere that you plan to sell again in the next 2 years then I'd be a bit more cautious. Taking advantage of the current borrowing rates is definitely a consideration for you though too.

We might see house price drops in some small areas. There are moves to reduce the number of short-term lets and Air BnB properties around us. That might cause a few extra houses to appear on the market.

You can never know when the next crash will be, the only thing that is certain is that you get older and start to run out of time.

I bought my first house last year, aged 40, as I could hear the clock ticking. I managed to get it at a reasonable price - and I'd manage to put down a healthy deposit through years of saving. And I knew I didn't want to buy a flat.

So I can withstand a correction.

I spent many years just hoping for a correction, but it didn't materialise. But that's not saying it won't happen - when you get crazy activity like the last few months, it's often the sign of a market top.

No!

I can't see it happening... At least not unless the country goes properly bankrupt and then the value of your house will be the least of your worries.

We've seen time and time again governments saying 'there is no magic money tree'...

But yet there clearly is a magic money tree when it suits.

If you buy a house and then stay in it for a long time it doesn't matter if the prices go down as you won't be selling it. What caused the disaster in late 80's was interest rates of over 10%. Imagine if interest rates went to 10% now and how many people would be returning their keys and losing any equity they had in their house.

It’s very location dependent

Even within the same town.. In my locale I can get a LOT more for my money if I'm prepared to buy in one of two areas that are... How can I put this politely...

'wretched hives of scum and villainy.'

I'd rather a smaller place in a nicer neighbourhood.

Labour shortage -> wage increases -> inflation -> interest rate rise -> disaster

The UK has been a demand led market for decades and I can't see it abating any time soon. There are half the amount of houses on the market in my town than there were last year. Went to see a completely rundown one in a decent area today. It went on the market Wednesday and there have been 19 viewings so far. Everything is in high demand at the moment, which would normally push inflation up but no one can buy anything, so it's all a bit weird. Currently trying to nurse my bald rear tyre as a replacement isn't possible for a few months at least yet.

Labour shortage -> wage increases -> inflation -> interest rate rise -> disaster

would interest rate rise be such a bad thing?

would interest rate rise be such a bad thing?

Won't cause a crash, the BoE/FCA has mandated for several years that all mortgage applications are stress tested at higher interest rates specifically to prevent this scenario.

So long as there is access to cheap.credit the can will be kicked down the road.

Until someone gets cold feet and starts to realise the likelihood of it ever getting paid back is zero. See also 'sub-prime'.

In my opinion there will be a large uptick in repo's as people who are recently mortgaged to the hilt see their food/clothing/etc prices go up by 10% and the repayments are too much for them.

Even within the same town.. In my locale I can get a LOT more for my money if I’m prepared to buy in one of two areas that are… How can I put this politely…

‘wretched hives of scum and villainy.’

I’d rather a smaller place in a nicer neighbourhood.

It isn't really 'more' for your money if your quality of life isn't satisfactory. A home (as opposed to a house as investment) is more than the square footage on the floor plan.

I'm in total agreement. Even the newbuilds that aren't boxy little shacks are so close to each other that if you trip over going out of the patio doors you end up in next door's 'garden'. I suppose this is an advantage on a lot of newbuilds, though. Being built on flood plains mean packing the houses on top of each other so you can run planks from roof to roof and reach high ground. 🤷♂️

One side effect of banking laws introduced after the 2008 crash was ring fencing high street banks deposits (so the investment arm can't invest them). This has meant that a lot of high street banks are sat on billions in savings which they can't invest as they normally would; so they are flooding the mortgage market with cheap loans as it's pretty much their only way of generating a return on the money. Combine that with people saving more during CV-19 and it has created even more cheap mortgage offers...

would interest rate rise be such a bad thing?

From a moral point of view or a practical economic one?

If people are mortgated to the hilt and rates go through the roof, what do you think will happen?

If people are mortgated to the hilt and rates go through the roof, what do you think will happen?

They'd have to really rise to cause a significant increase in repossessions.

Current stress test is 3% rise combined with capped loan to income multiples.

https://www.fca.org.uk/firms/interest-rate-stress-test

What happened on 08 was more of an overstretched mortgage crash, the house prices recovered and mortgage defaulters didn't, prices dipped for how long?

Unless you change your house every other year it's not really the right question, will mortgage rates rise? maybe a more realistic one, house prices along with pretty much all prices will always go up in the long term, the rates we pay to borrow the money to buy them is the problem.

Dannyh gets it.

It's not just the mortgage rate going up it's costs in general

Right to buy was a great policy abysmally implemented. The proceeds should have all gone back into building new housing stock immediately, if done properly it could have been self sustaining, even with discounts what the properties were sold for should have been more than the cost to build a new house.

Cheap credit at ridiculous multiples of income have created this mess, a massive interest rate hike and immediate capping of what people can borrow, maybe back to 3.5 times salary are about the only way house prices will return to affordable levels. Meantime more and more wealth will be concentrated with fewer people as more are forced to rent, people with parents with property might have a chance themselves, how people without help will ever get on the ladder I have no idea. Social mobility peaked in the 80s with funded university and affordable house prices, social mobility has been going downhill ever since driven by the policies supposedly designed to increase it, student loans and loads of credit.

The proceeds should have all gone back into building new housing stock immediately, if done properly it could have been self sustaining, even with discounts

I am not sure about that. It would have slowed things down but ultimately if the state are giving things away cheap it would eventually hurt.

For the OP I am tending to go with no. It should do but we currently have our entire economic model built around propping it up so whilst said bubble would should burst everything else will be sacrificed first.

In the past idiots who over extended would have been screwed by the high interest rates but now the savers will be sacrificed to save them which becomes a vicious circle.

That and all the donations to the tories by the housebuilders to keep the shit first time buyers schemes going helps prop it up.

They’d have to really rise to cause a significant increase in repossessions.

It's not repossessions I thinking about, it's the reduction in disposable income which will reduce consumer spending which will then be another drag on the economy.

Of course we need a dramatic reorganization of the economy but that would be better done proactively whilst we still have the means to live well in a different way; rather than to try and rebuild after a catastrophic crash.

We live in strange times. Was recently listening to an economist on r4 who was arguing that everything indicates we should have much higher inflation and would be in recession, but western governments are stuck in a cycle of printing money (which is what in effect is happening), which means all bets are off

I'm not going to pretend to understand economics, but didn't interest rates reach something like 15% in the 80s? House prices were much cheaper on paper, but the cost of buying was not - unless you had cash, of course.

Those kinds of interest rates would be game over for most buyers at current prices, and with records levels of money printing, and manipulation of inflation figures, how are we to avoid inflation and rises in interest rates in future? Do the old rules no longer apply - are we living in a new economy? Or is my understanding of it completely wrong?

They’d have to really rise to cause a significant increase in repossessions.

Current stress test is 3% rise combined with capped loan to income multiples.

https://www.fca.org.uk/firms/interest-rate-stress-test/a >

‘The PRA and the FCA should ensure that mortgage lenders do not extend more than 15% of their total number of new residential mortgages at loan to income ratios at or greater than 4.5

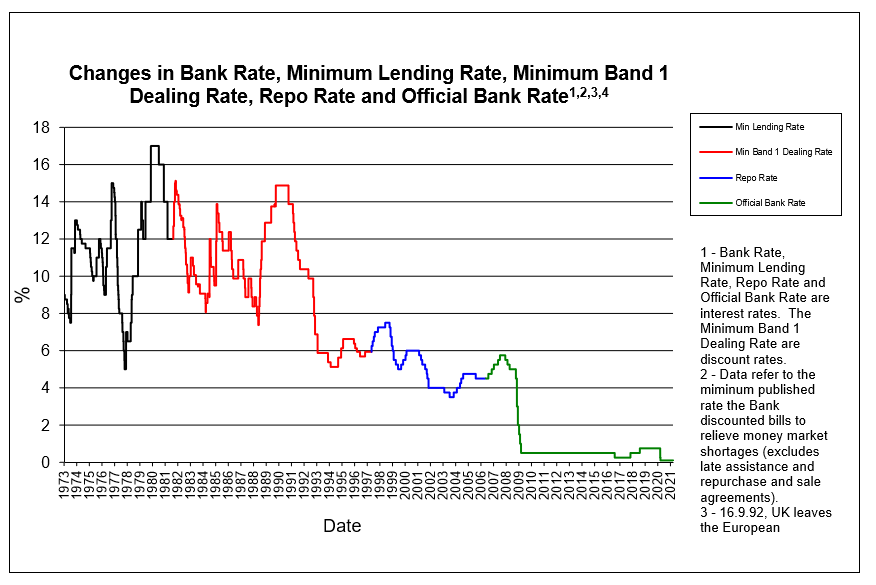

Prior to the financial crisis in 2008 , mortgage interest rates were around 5% and the income multiple you could borrow was closer to 3.

We're still dealing with the consequences of the crisis and interest rates have been artificially low for a decade because of it.

That stress test doesn't sound like its stressing things enough to be honest.

^ That chart is terrifying for somebody looking to buy a house at current prices.

Our entire economy is based on house prices not crashing, if they were to crash we would be in a huge recession with interest rates going up, jobs going down and the usual crisis’ that it would bring.

Can you explain this some more. I've heard it loads, but not the detail behind it. Note that I'm specifically interested in the causality in the direction stated. I totally get that if interest rates go up and jobs go down and we hit a huge recession then house prices crash, but I don't understand the immediate causality of the reverse as you seem to have stated it.

Is there one?

Do the old rules no longer apply – are we living in a new economy?

Gordon Brown abolished 'Boom and Bust', just before the 2008 crisis...

.

It's not called an economic cycle for nothing