Happy Sunday STW!

So last night we were having a chat about house prices. Yes, I know, terrible way to spend a Saturday night. Apparently, some time ago I'd said that the only thing to make prices plummet would be a pandemic. Well, that's happened and nothing has changed. It's back to business as usual, living in a building site with flats and conversions going on all around.

So I swear, the earth could become a post-apocalyptic waste-ground inhabited by ghosts and a poxy terraced house would still go for £175k.

So what would it take for prices to REALLY plummet. And I don't mean was £175k last week, now on at £169k... I'm talking about £30k or something, houses becoming places to live rather than assets to buy and sell. Lots left empty, no profit in rental/buy to let etc... Houses cheap enough that pretty much anyone who wanted a home could buy one? Older STW'ers, has this happened before?

All that might happen is that prices stagnate and incomes slowly rise so that the income multiple reduces. But, it would be over a long period of time.

Once everybody gets spaceships.

some time ago I’d said that the only thing to make prices plummet would be a pandemic. Well, that’s happened and nothing has changed.

The economic impact of the pandemic hasn't even started yet. We're in a weird limbo. That's going to hit like a tsunami when the furlough scheme ends in October

Then we'll see how the price of anything, let alone houses, stands up to mass unemployment. The Worst-case predictions are unemployment of 5 -6 million

The only people buying houses will be opportunistic landlords snapping up the properties that have been repossessed from the newly unemployed who can no longer make their mortgage payments

The only people buying houses will be opportunistic landlords

And investment funds, registered abroad for tax purposes.

Binners, who's going to live in the houses snapped up by the scumbag landlords? Those 6 million will be shoved into old offices at £420pppm paid for out of housing benefit. Whilst billions of 'luxury flats' are still flying up all over the place... it's weird.

House prices won't fall until there is an adequate supply of affordable, social rental housing for the maybe 25% of the population who probably will never be able to afford to own their own home, who are currently forced into the private rental sector, so pushing up demand and rents and the housing benefits budget.

I'm in no way blaming private landlords for the situation, it's the result of 30 years of Tory policy and 13 years when New Labour did **** all to address the problem.

You can get a house for £30k but you probably wouldn't want to live there.

If you bought a speculative plot for £10k then got planning and built a modest two bedroom house on there with your own labour it still wouldn't be £30k.

We have folk talking about spending £30k to build a garage.

A nice static caravan will eat up £50k.

I've just put in for planning for two semi detached bungalows in my garden, estimated build cost £90k each.

The economic impact of the pandemic hasn’t even started yet. We’re in a weird limbo. That’s going to hit like a tsunami when the furlough scheme ends in October

This is what I fear. We've been considering extending our house for a while but have put additional borrowing on hold until the economic picture is clearer.

With the amount of for sale signs going up and how quickly they are selling it seems many others don't share my concerns.

House prices will only go down is they are not selling for whatever the price at the time is. That will only happen if people either can't afford to or decide not to move so mass job losses for the middle classes or interest hikes are the only thing I can see lowering prices. Not sure how likely either are.

"I’ve just put in for planning for two semi detached bungalows in my garden, estimated build cost £90k each."

Why? Seems a bit excessive just to get out of mowing the lawn...

EDIT: Could somebody please tell me how to quote. It's all changed around here.

The pandemic isn't going to be enough on it's own. Even lumping Brexit on top won't be enough as the rich will just invest in BTL's and screw the poor people as per usual. They would feast on building up their portfolio at repossession auctions, do minimal work to the properties and wait for the govt to pay them to house the homeless families via the benefits system.

The other option is Civil war.

It would have to be large enough to bankrupt the country and violent enough that the cast majority of infrastructure and businesses would be destroyed. Only then would the wealth be completely stripped out of the country enough that house prices might fall enough that the majority could afford to buy but then there would be no jobs so we'd still be stuck.

Basically it's not going to happen any time soon. It's easier for me to resign myself to the fact I'll most likely never own my own place but continue to save money so that if a massive price correction does happen I'm in the best possible position to take advantage of it. But that correction will never happen as the health of the country would have to deteriorate so far to make it happen that it will never be allowed to happen.

That is really depressing to write but it's true.

so mass job losses for the middle classes or interest hikes are the only thing I can see lowering prices

The middle classes are about to experience the mass unemployment that deindustrialisation visited on the working classes at the end of the 80's. It's started already. Employers are already viewing this as an opportunity to massively reduce both their wage bills and the nature of their contracts. See what British Airways are presently up to as an example.

The immediate future in an economy with few jobs and millions of highly-educated, highly-skilled, desperate people chasing them, is part-time, zero-hours on massively reduced rates of pay and no holiday, sick pay or any other perks.

You're going to need a degree to make coffees in Costa for minimum wage.

Those with large amounts of ready capital are going to have a field day increasing their property portfolios, that they can then milk the housing benefit system to rent back to their unemployed former owners

While interest rates remain low and they will for a long time under this paradigm - this is how things will be.

The BoE is running out of ground with adjusting interest rates to control the economy.

But there will be a paradigm change eventually.

But also like Binners, I agree we have not felt the worst of the pandemic yet in terms of economic fall-out.

Not so a much a plummet, but we might see a small drop once the Stamp Duty exception ends in early 2021, plus furlough scheme should have ended by then.

I’m talking about £30k or something, houses becoming places to live rather than assets to buy and sell.

I dunno who you hang out with but everyone I know just buys a house where they want to live and lives in it. Why do you have to paint us all as capitalist pigs?

Anyway. A £30k drop isn't much, pretty sure that happened in 2007 and that was because of credit restrictions amid a recession. I don't think house prices will plummet suddenly as people will simply not sell at too low a price; or if they need to move they will rent the old one to someone who cannot buy because either their low wages can't afford the still high buy prices or they cannot find a house to buy because no-one is selling.

I meant 30k total not a drop... 🙂

And I wasn't calling you a capitalist pig honestly. Most people I know are exactly the same. Although a lot of them then become obsessed with 'the game'. "this time next year this place will be worth eight times what I paid for it, If I put a stud wall up the middle of each room it'll be worth TWENTY TIMES MWUHAHAHA! etc etc

Not going to happen.

maybe 25% of the population who can’t afford their own home

I’d say closer to 50% going forward

Lucky news for landlords. Self-fulfilling prophecy. I remember a bright fellow who back in the Right To Buy selloff got a new job that paid well so he decided to buy the family council house that had been home to a big family for decades. He moved their mom out to a smaller council home. He said ‘I’m buying the family home to safeguard it so the whole family will always have somewhere to live if they need it’. The former home somehow instead got done up and sold off quickly for him to buy a bigger house/investment in the country for him and his wife 🤣

That was over 30 years ago. Today? Watch this and read the comments

If it doesn’t make you weep then you’re already raking it.

Interest rates rising to 15% would do it, that completely wrecked the house prices back in early 90's. A lot of people just had to hand the keys back as they couldn't afford the mortgage and the house was worth a lot less than the mortgage.

Another thing would be for the government to build say 5 million houses which were actually affordable (government acquired "free" land, houses sold at cost) with deeds that only ever allow the buyer to sell at purchase price plus inflation. That would cause oversupply and allow people paying ridiculous rents to actually buy and the whole market would drop massively.

Just let me know first so I can get the half million out of my house before the massive crash...

So what would it take for prices to REALLY plummet.

Severe population decline. It's a supply-demand thing. Supply is not going to massively increase, so only a massive decrease in demand would do it. Millions of deaths due to pandemic would do it, so would deporting millions of people. Or pandemic + Brexit being so bad that anybody who could leave, did.

*Just to be clear, that’s not the same guy in the video. Just the same situation where houses have been viewed increasingly (by their owners) less as homes, but as business opportunity, currency and leverage. The UK home rental market is also about to explode and set it’s trajectory.

The smart investor loves a war etc.

But this is the way it will most likely go (in the UK)

- Housing will become more expensive as the percentage of income

- Limited supply means house prices continue to rise, therefore:

- Growth/switch to the private rented sector will continue

- Growth in wealth inequality. Rising house prices benefit homeowners (typically older people). However, it reduces living standards of those without a home. The UK will increasingly become divided between those who own a home and those who don’t.

- Upward pressure on rental prices. The shortage of housing will put upward pressure on the price of rented accommodation. Housing costs will take a bigger share of people’s incomes (affecting their discretionary income)

One day I hope that our great-grandchildren will wonder what we were thinking when we decided ‘why make a home when we can build a pyramid scheme’?

Just when you think it’s gonna happen Elon Musk gonna watch Armageddon, fly up to that gold laden asteroid, fly bk with a 100t weight load of gold and buy all our houses, then jack up rent for all. Mwaaahhhh haaa haaaa

In the west of Reading terraced houses were being bought and turned into HMO's. However, there is a steady migration back to Eastern Europe so prices are dropping. Not sure if a family would want to buy such a property though.

In the west of Reading terraced houses were being bought and turned into HMO’s. However, there is a steady migration back to Eastern Europe so prices are dropping. Not sure if a family would want to buy such a property though.

Was happening in the Fens a year or so back - landlords who saw the market for shared housing converted them, and were just beginning to see that they were either going to have convert them back to family houses or sell them as unattractive properties to someone else to do the conversion.

The Eastern Europeans who were planning to stay were already looking to buy/rent nicer, more modern family homes.

A 90% reduction in the population?

What happened to that poster from here who’d pop up fairly frequently ranting about how overpriced his local property market was and how his lowball, what he thought he should pay offers kept getting refused. Except every time he did, the market had risen another few % and got even further out of reach.

I bet he’s still waiting for the big crash....

Interest rates rising to 15% would do it, that completely wrecked the house prices back in early 90’s. A lot of people just had to hand the keys back as they couldn’t afford the mortgage and the house was worth a lot less than the mortgage.

This!

I bought my first property for £55,000 in the late 80's and promptly watched it drop by ~30% while my mortgage went up every month (and for about 6 months I really do mean every month).

The only thing helping me keep my sanity was we bought it second hand while new ones less than 50meters away were still selling for £65,000 which would have put me nearer a 50% loss.

At the same time I (and many others) found themselves being Ade redundant regularly (about 4 times for me and roughly every 12-18 months).

I have just checked now and my first house last sold in 2006 for £134,950

In all honesty, I agree with some of the comments above. We have not seen the real financial impact of Covid yet. I would be surprised if house prices did not drop significantly as more and more people find themselves without a job

The same as Spain and Greece following sub-prime.

People can't pay the mortgage and can't afford to rent either, the banks repossess, the people move in with parents or grandparents and the banks hold onto the property dripping it back onto he market in the hope of avoiding a total price crash. New developments stop and some are never finished, many existing properties sit empty. A Spanish funded development locally has been finished this year having been started in 2006 with an original delivery date of 2008.

As others have said, it's about supply and demand. An economic crash might force people to sell up or get repossessed, but unless we are wanting to cull all these homeless families, then the lack of affordable accommodation hasn't actually gone away.

So it's about building suitable affordable social housing for those who need it, and taking the pressure off the rest of the market.

There's a post lockdown mini boom just now.

I can't imagine prices not crashing, given the inevitable impact on the economy from Covid, which is barely in evidence yet.

why make a home when we can build a pyramid scheme

I don't think the pyramid scheme was planned. There just weren't any government plans to prevent it, so the natural actions of people with money created and sustained it. And this is Toryism in a nutshell. Let whatever happens happen, people (including Tory ministers and donors) take advantage of it, and if you are disadvantaged then it's your own fault obviously because if I became rich why can't you? And of course they prefer this explanation rather than actually thinking about their privilege and power and how much they are screwing people.over by doing nothing.

It's like creating a zoo with no cages, and if the lions eat the visitors then hey, that's your own fault for being too slow. Except the only shop selling cheap food is in the zoo and the expensive one is outside away from the lions.

You can get a house for £30k but you probably wouldn’t want to live there.

If you bought a speculative plot for £10k then got planning and built a modest two bedroom house on there with your own labour it still wouldn’t be £30k.

We have folk talking about spending £30k to build a garage.

A nice static caravan will eat up £50k.

This +1

While land values in big cities and the South might be stratospheric and pushing up prices, the rebuild cost of a house in a lot of The North is probably higher than the houses value!

You want a terraced house for £16k, here you go, and it's far from the cheapest house in town too! I used to work with a guy who ran the project to install central heating into social housing in Teesside, he reckoned the value of the copper alone was higher than the property values in a lot of cases, just have a look at auction catalogs, plenty of houses sold for <<£1000, with the heating ripped out!

https://www.rightmove.co.uk/property-for-sale/property-78252430.html

There’s a post lockdown mini boom just now.

This ^ , my bro put in his maximum bid of £118k for a 2bed house in our wee Galloway town, sold to a developer from Yorkshire for £140k who buys properties for holiday rental, he already owns3 properties in my mother’s street alone, stopping ****s like this buying properties would be a start

With the amount of for sale signs going up and how quickly they are selling it seems many others don’t share my concerns.

My work colleague, who’s air hostess wife has just been made redundant and who is constantly now complaining about the lack of commission he’s currently earning, is trying to buy new £430k 4 bedroom house near Harrogate. Not only has the bank increased the deposit from 10% to 15% which he’s mitigated by the current stamp duty removal leaving him no cash for decor and repairs, the survey just turned up some damp issues.

Rather him than me, it feels so 2019...

^^^

How is a £430k new build house damp?

But yeah, some people attitude to risk is more cavilier than others.

...he already owns3 properties in my mother’s street alone, stopping **** like this buying properties would be a start

This. When homes are used for living and not treated as a commodity might help. One of the guys in our cycling group has 10.

How is a £430k new build house damp?

Apologies - new to him not a new build.

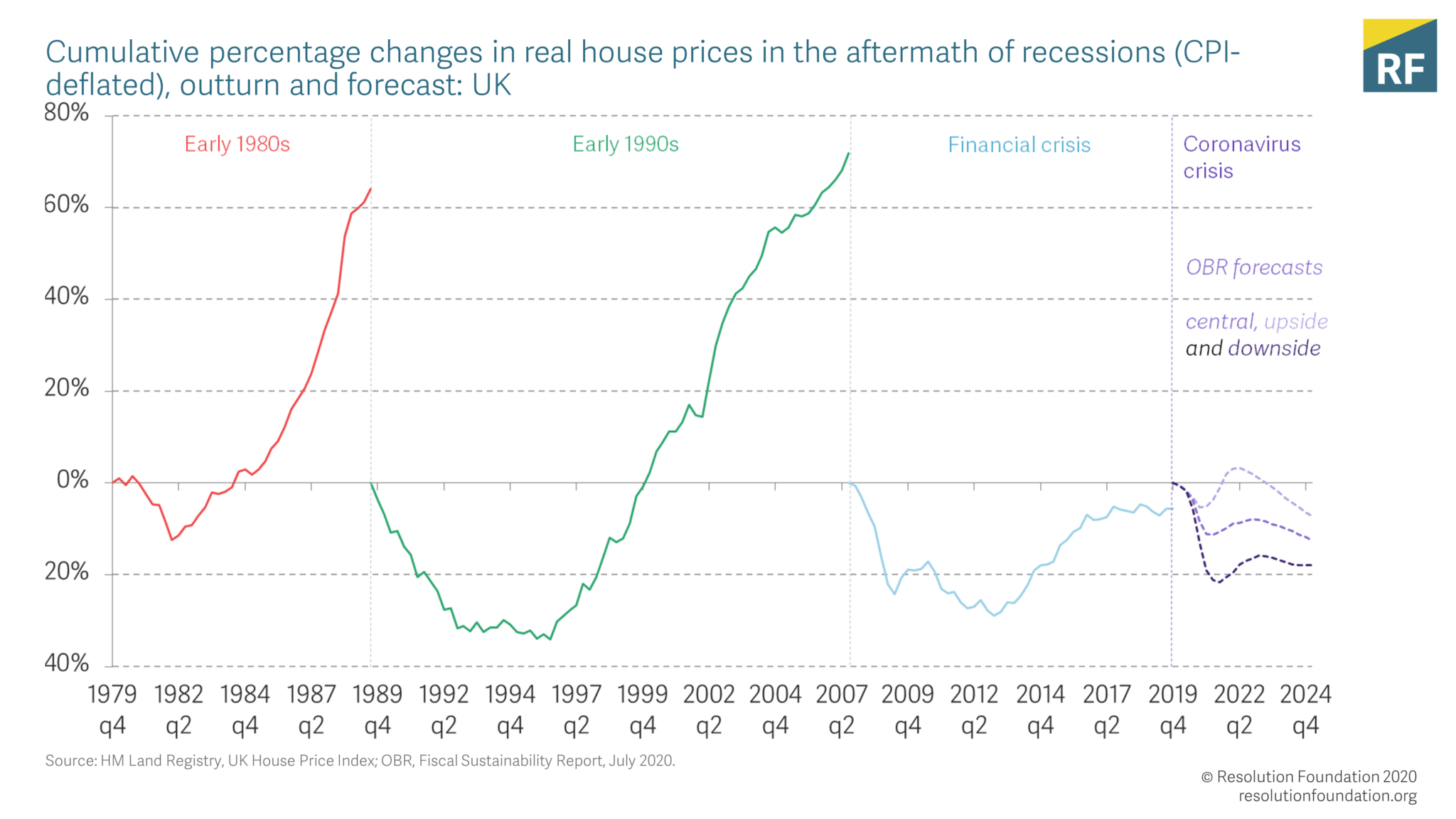

Well here is a more informed forecast:

https://www.resolutionfoundation.org/publications/housing-outlook-q3-2020/

In housing you'll getting an increasing concentration of ownership, they have the money to keep the market buoyant. But it will be standards of living that REALLY plummet as the keys and cars get given back. Apparently a high proportion of urban dwellers looking to buy are looking for a rural relocation so the pattern will be uneven.

In a localised way - oversupply. This happened on the south coast of Spain - loads of British pensioners retired out there - development companies built concrete ghettos on flood plains and just kept building - the pound dropped against the euro and they all tried to come back to UK. Houses that were bought for 100k euro now lucky to get 20k.

Something so bad we'd all loose our jobs and not be able to afford them. A friend predicted doom and gloom and was holding on for a huge drop about 10 years ago. He's still renting and I'm 4 houses down the line. If anyone here really knew they'd have much better things to do with a Sunday than come on here. If you can afford it buy one if you can't and you're down South those prices will never be reasonable I'll wildly predict!

If anyone here really knew they’d have much better things to do with a Sunday than come on here

ISWYDT. But forgetting the ironing, what should we ‘really know’?

If a house could be bought for 30k in most of the I'm we would have much larger problems. This is not something you should hope for. This would be below the cost of building!

I agree houses are overpriced in some ways at the moment but a crash to even a fraction of that extent would hurt more people that it helps.

Probably the best outcome is a small to moderate drop with a stabilisation in price for a long period.

As to what it takes I think this is what may happen. 10-20% drop and stagnation or very slow growth.

Eyewatering tax on 2nd properties will do it, because everyone BTL ing is driving the inequality at the bottom layer. But all the Tories, and loads of labour I'd bet, are all private landlords so it won't happen. It should but it won't.

Why do people want house prices to plummet? If they do the economy is proper goosed.

The economy is goosed and a direct consequence will be falling house prices.

I’ve just put in for planning for two semi detached bungalows in my garden, estimated build cost £90k each.

Poor lamb. Time for some crowdfunding darling?

The economy is goosed and a direct consequence will be…

…more people renting, and a greater proportion of their income being spent on rent.

Why do people want house prices to plummet?

So they can afford to not be homeless?

Why do people want house prices to plummet? If they do the economy is proper goosed.

Because they want the possibility of buying a house and not paying ridiculous amounts of rent. You don't need to go back that far to a time when a nice flat in a nice area could be had for around £200 mortgage. Now a very shitty bedsit in a shitty part of town is £400 a month rent.

The impact on those who have purchased a house at the very high current prices won't be happy but the answer for them is not to move. If you don't move then it doesn't really matter what the price of your house is doing.

Yes it does quite a lot - as you will be paying way over for your mortgage and in negative equity. Paying say £500 a month for a house when you could be renting same for £200 for example, or buying same for £200 a month, and in a very precarious position if there is any sudden drop in income such as redundancy, illness, death of a partner etc.

Negative equity only matters if you are selling the house. The house was purchased based on the fact the owner could afford it. Stay in house for 30 years and they will be fine.

Some people will face redundancy, illness, death etc,. but those would hand the keys back and go and rent one of the cheaper properties.

Not saying any of that would be great but it would reset the prices. The thing then would be controlling them so they don't just all go back up again and be in same situation in 20 years times.

Building enough houses would steadily lower relative prices. It's not in the interests of anyone involved though. Particularly not developers, and while it's not reasonable to expect them to be charities, it would be nice if they weren't ****s. The state needs to get involved again and build decent quality social housing that is affordable. Not going to happen in this lifetime.

Negative equity only matters if you are selling the house. The house was purchased based on the fact the owner could afford it. Stay in house for 30 years and they will be fine.

All well and good..... Then your job is made redundant and to get a comparable job in your skill set you need to move across the country.....

Negative equity only matters if you are selling the house.

Not quite. When it comes to your next mortgage deal, the loan to value ratio will become dire, and your mortgage payments will increase, at a time when your income is likely to have been reduced (if house prices have taken a dive, you’ll be lucky if you avoid what is likely to be happening in the job market).

Anyway, there won’t be a big drop in prices, just a slump… and more people will be trapped in the rented sector, not fewer. An economic downturn doesn’t help people buy their first homes, that’s just a fantasy. It does help some people buy extra houses though.

That makes sense kryton.

Few months of no sales bubbling over

Those in flats wanting gardens .

Those who were thinking about moving wanting to do it while there's a stamp duty relief and they have a job ..... It's much easier to keep a mortgage with a lesser paying job than it is to get one..... There are mechanisms you can trigger to help you keep the house. Where as you'd never get lent to with out or with a low paying job....even if the cost is less than rent

Because they want the possibility of buying a house and not paying ridiculous amounts of rent. You don’t need to go back that far to a time when a nice flat in a nice area could be had for around £200 mortgage. Now a very shitty bedsit in a shitty part of town is £400 a month rent.

What is the obsession with 'having' to buy a house?

In a world where buying an average car costs more than £200 a month, and a mobile phone line rental can easily be half that a month, it's exceptionally unlikely, unless you can go back in time 40 years.

I'm sure everyone who has a house & a mortgage isn't quite so motivated to see house prices drop to a level where they cost as much as a mobile phone each month.

@twinw4ll has found the only surefire method of wrecking property prices - build a couple of cheap houses in your own garden 😂

And as much as more cheap/affordable housing is great for those looking to get onto the property ladder, it isn’t going to affect the value of existing, desirable houses in the slightest.

really? Have you seen the difference between paying a mortgage & renting? (Not to mention the stability aspect... I know renters who’ve been “moved on” almost yearly!)What is the obsession with ‘having’ to buy a house?

The answer to the OPs question is as simple as supply and demand.

If the availability of housing were to match (or even exceed) the demand you'd be on your way to arresting house price inflation. Unfortunately we've engineered a situation over several decades where supply is throttled to ensure housing is a profitable investment...

So I don't know about actually driving house prices down, it sounds like a great idea to those not (yet) on the "property ladder" but then so much of people's finances are tied up in their homes once they buy one, especially the boomers. People are now counting on their house increasing in value year on year.

Boomers who TBF were told to buy a house both as a home and as an investment over and over throughout the last 50 odd years. Maggie made it even easier by bumping the supply side briefly during the 80s with 'right to buy' (but subsequently everyone sort of forgot to replenish social housing stock)...

So yes "Derek and Jeanette" cleared the mortgage on their lovely four bed twenty odd years ago, and have just sat on (in) what is now an appreciating asset, and their pensions (part funded by property investments) more than cover their living costs so there's no real need to sell up and downsize. They'll just let the kids squabble over the house as part of the estate when they pop their clogs (or let them flog it to fund their end of life care)...

People like to tell you that interest rates spiking in the early 90s stalled House prices, but it didn't stall them for that long, same goes for the 2008 crisis (that was even caused by a US housing bubble) but again we've seen a pretty steady increase in house prices since. The general trend has been up and up for most of the last 40 years...

The housing market in the UK is vexatious, held up by old people, and used by the finance industry to drive profits. It is ultimately just another example of the intergenerational wealth gap...

A pandemic (a 'proper one' that wiped out a few million old people) might have an effect on the housing market, but then all the surviving Gen-Xers and early Millenials (ahem) would swoop in and repeat the patterns of their parents by buying up housing stock, not downsizing when their kids leave home, and throwing money into pension and investment funds, who in turn will buy up and convert old office blocks for their children and grandchildrens generation to pay excessive rents on while aspiring to be able to buy a house one day...

The trick is to break that pattern without bankrupting huge swathes of the population. Let us know when you figure out how to do it...

I've no idea of the answer.

If you look back at the cause of the current situation, it was the banks allowing bigger mortgages.

When we bought in mid 90s,it was only something like 2x or max 3x your income.

Early 2000s that was relaxed and prices doubled in a very short time. Then a crash. But prices remained stuck up there due to the terror of negative equity.

The solution is for all of us comfortable home owners to support a government policy to provide good quality affordable social housing.

What is the obsession with ‘having’ to buy a house?

If rent was very, very cheap then guess there wouldn't be.

But would I rather pay £1000 a month in rent for 60 years or would I rather pay £1000 for a mortgage for 25 years (and own the house at the end)

Can you guess which I would go for and why?

The solution is for all of us comfortable home owners to support a government policy to provide good quality affordable social housing.

Where have you been for the last 40 years. That is never going to happen.

Not in this country now, no.

Cougar

Subscriber

Why do people want house prices to plummet?So they can afford to not be homeless?

Aye but if house prices plummet, means the economy is properly goosed, so they won't be able to afford the cheaper prices either...

What is the obsession with ‘having’ to buy a house?

It's not an obsession. It's just good sense if you can afford it. Why give money away to some other well-off person you can keep it to yourself? I don't see why wanting to do this is such a bad thing?

Houses prices are driven by the availability of credit. Not by supply and demand, there are plenty of houses for sale.

So for house prices to fall the amount people are allowed to borrow would need to fall.

Inflated house prices benefit no one other than mortgage provider and they have driven it by allowing people to borrow vast amounts of money.

In a low interest economy it was the only way to maintain their profits.

There’s a post lockdown mini boom just now.

This ^ , my bro put in his maximum bid of £118k for a 2bed house in our wee Galloway town, sold to a developer from Yorkshire for £140k

The other half of my Mum's semi det just sold for 25% over the asking price

Have you seen the difference between paying a mortgage & renting?

The difference between the mortgage I've just taken out and the rent my girlfriend is paying is about six quid a month.

Why give money away to some other well-off person you can keep it to yourself? I don’t see why wanting to do this is such a bad thing?

Because, this. It's not like car rental where you get a brand new house every three years. You can pay an amount of money off your mortgage or you can pay pretty much the same amount off someone else's. Why would you buy a complete stranger a house?

The only compelling reason I can see to rent is if you don't have the deposit, it's why my OH is renting. I'm told by my mortgage advisor that in the current climate (as of a couple of months ago anyway) all mortgage lenders are asking for a 20% deposit apart from HSBC who he says are so obtuse to deal with that it's not worth the hassle. This may (will) change once things calm down again but if you're looking to buy say a £200k property tomorrow you're going to need forty grand in your back pocket.

A friend of mine has a house in the Fens. He's tracked down the deeds to all the purchases over the years, and has them on the wall in the hallway. House was built in 1790 as part of a 160 acre farm estate. and was bought with a mortgage for £110, and then remained in the family for 5 generations until it was sold in the 1930's for £400...(at this point it was still a working farm) Sold again (as just the house) in early 1970's for £20,000, he bought the house in the early 1990's for £250,000 ish....It's an extended 4 bed farmhouse with a couple of acres of garden/paddock (all the farmland and outbuildings have been sold off, or knocked down in between the war and the 1970s)

TBH I don't really know what that says about the value of houses, but the rate of House price inflation that happened post war is astonishing...

TBH I don’t really know what that says about the value of houses, but the rate of House price inflation that happened post war is astonishing…

So I had a play with the BoE's inflation calculator.

was built in 1790 as part of a 160 acre farm. and was bought with a mortgage for £110

£16,700 today.

sold in the 1930’s for £400

Assuming 1935, £28,662.

early 1970’s for £20,000

Assuming 1972, £265,881.

early 1990’s for £250,000 ish

Assuming 1992, £521,276.

Anyone any good with graphs? (-:

Houses prices are driven by the availability of credit. Not by supply and demand, there are plenty of houses for sale.

+1 . It's much more nuanced than lack of supply. Plus the houses being built aren't necessarily usually the ones in demand.

So I had a play with the BoE’s inflation calculator.

Those inflation calculators don't really work for giving a feel for historical prices, becasue people didn't live in the same way, buy the same things, or expect the same levels of material wealth as we do now.

A better way of looking at it might be that in the 1790s a farm labourers yearly wage might be £18 a year. So the cost of the farm was 6 times a skilled labourers annual income. Probably still a much lower ratio than today. But it would have been much harder for a labourer to borrow any money at all, unlike today.

At the same time £1000 a year would put you firmly into the ranks of the lower gentry, but most of those would have been leaseholders rather than freeholders.

A huge wedge of our economy is based on the value of property, as others state it's nigh on impossible to see a plummet in house prices that doesn't decimate the the economy, as stated before, the economy is based on debt, both from people taking loans to buy stuff, and the companies who manage the loans and so on, you start the domino effect and it'll be a disaster.

I've been thinking about how you'd get house prices to £30,000.

a) turn Britain into the equivalent of 1980's Beirut or 1990's Mogadishu. Cheap house if you can except a high chance of a horrific death.

b) Re-run the black death, and wipe out a significant portion of the population. Cheap house if you are happy to loose all you neighbours.

c) Government and local council financed and run house building and leasing scheme (ie council housing 1950's/1960's style, plus buying existing houses and renting them out at below cost). This would take decades to plan build enough good housing stock do push down the cost. Cheap house for you children.

d) remove planning and building regs, allow rapid development of overpriced cost cutting designed/built on the outskirts of towns, who's design life will be less than the mortgage used to buy them. Cheap house now until you get the heating bill and the roof starts to leak.

I would like c) but I think d) is closer to the reality

"oooo! You youngsters have it easy! When Albert and I bought our first house we had to work 14 hours a day to pay for it!"

Now, to afford the same style/size of house, the "youngsters" would have to work about 28 hours a day. But the quality would be worse-you know the sort of thing "skilled" "craftsmen" "lovingly" forgetting to put any cement in the mix or meeting basic fire regulations.

There really is * all left in this doss hole worth shouting about if you have no bank of mom and dad to lean on.

(Squeak! Clunk! Squeak! Clunk!)- Oh look! Here comes the edge case to prove the other 5.5 million people wrong: "I had nothing and saved up all my sand and I bought a * hole in a * hole and had nothing and did all the work etc, bollocks, etc....

From internet land somewhere-if the price of a factory made, Sunday chicken from Tescos had matched house price inflation, it would now cost you about £53 for a Sunday cluck, based on a 1970's "average" house.

Noticed how many trailer parks there were in the UK, say in 1980. Probably not, 'cos there was hardly any.

Noticed how many there are now? Unlikely to be that many in STW Acorn code areas but there are now **** 'undreds. That's the only "home" most people will be able to "own", post covid, post brexit.

The thing is, if a price crash happens, who will end up paying for the home owners landlords and people with 2nd homes?

The renters-because they haven't lost anything.

Winner! Winner! £53 chicken dinner!

The renters-because they haven’t lost anything.

Yes, but as a Landlord my mortgage just rocketed in cost due to the huge financial crisis, so I am upping your rent. A lot.

people are willing to bid a proportion of their income on a given house. Lets say its a mortgage payment of half of everything that's left over after you've paid for other essentials (food, clothes, fuel).

in the last 50 years, 3 very significant things have happened

interest rates dropped, so the amount you can borrow whilst meeting that criteria has increased

wives work a lot more, probably increasing the spend by 50%

everything else essential - food, clothes, fuel - has got cheaper compared to the average salary.

longer mortgages are also commom place.

ignoring the impacts of inflation (and based on todays prices, to take that out of the equasion), a family willing to spend £500 a month @7% interest over 25 years (out of a £1500 single income) in 1970, and so offered £75k for a house might find that they're pulling in £2500 now (wife works part time), they spend less on food clothes etc (£300 instead of £500), so they're willing to spend £1100 on the mortgage, which is now 2% over 35 years, so they're now willing to offer £330,000

thats a price rise of 4.4x, which is more than the 3.6x change which has actually happened in the last 50 years

if any of those things change, house prices will change, but so, probably, will an average individual's attitude to how much their willing to spend. every generation complains that houses were pric

in the last 50 years, 3 very significant things have happened

Also don't forget that access to debt has increased. Its a lot easier to borrow a lot more money now than it was in the 1970s. Even in the late 80s mortgages were strictly 2.5 x joint income (even if you didn't need an interview with the bank manager). Now you can borrow more, people are willing to pay more.

To really plummet, to some of the figures in this thread, where the land is worthless, there is no vlaue to the location and you are merely paying for the build cost... nothing that I (as a 29 year old non-homeowner) would want to live through.

To stabilise, to become less of "an investment" to the BTL crowd, and become a practical means of having a roof over your head; without screwing over millions of other people in the country who currently own, or worse, are mortgaging their homes:

-Re-vamp the buying and selling process to make is simpler, and cheaper; Scotland is way ahead of England here but still far from perfect. People paying 5 figures on surveys, stamp duty and so on feel the need to get that money into their property value somehow.

-Stop the population growth, this could be happening already

-Stop the requirement for both halves of a divorced couple to maintain a full sized family house if they wish to share custody (or a reduction in people splitting up while having dependent kids, some sort of societal cange?)