UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

Anyone done it? By massive (by my standards) would be approx. 40% of my takehome on a historically low interest rate, with a term that ends in my early 70s.

This seems absolutely stupid, but, it is the only way I can afford a family home in an area I'd be happy to bring up kids.

How on earth do people on 'normal' salaries even the national average afford anything in the south.

My house has jumped 7% this year (great, but the place we want to move to have jumped 12%).

Only people winning this stupid merry go round are those charging % in sales, tax etc...

I know poor attempt at a rant, but it can't keep going this way can it?

Does your wife/partner work? If we are talking national average range salary I'm guessing you will need two salaries coming in for anywhere considered 'nice' in the South.

How your kids turn out is way more to do with you and your Good lady, rather than some nice area, or well thought of school. A lot of people can't seem to comprehend this.

how certain are you that you will get a mortgage into your early 70s?

are you just raising the topic for debate or seriously considering a larger mortgage?

What multiple of salary is being offered by lenders these days?

Discussing it the other day, our joint income is about £42k, three times that just about buys the cheapest property in our village. Really worry for people coming through now, it's madness.

40% of take home doesn't sound [i]that[/i] high. That said you need to do the calcs based on rates rising, although I don't think they will anytime soon. If it really is a stretch then I'd look at other areas. Plenty of nice bits of the country outside the usual hot spots.

[i]Anyone done it? By massive (by my standards) would be approx. 40% of my takehome on a historically low interest rate, with a term that ends in my early 70s.[/i]

We had a 3x my salary (non working wife) in 2001, but interest rates were at 6 or 7% so it worked out at somewhere in the region of 33% of my net.

Didn't particularly worry about it, as I'd had previous mortgages with double-digit interest rates and we owed nobody anything else.

Turned out fine as inside 10 years the rate dropped to 0.5% and the value doubled - the future? No idea...

Reckon it's possible if ....

If ... you can see the property as a house and not a home.

By that I mean.... if it goes wrong, you can sell the HOUSE without emotion and not think you're giving up a HOME with all the emotion that it might cause to you and yours (important to get the mrs thinking like this... kids don't care where they live, as love as they are loved, right?)

It may well work out great and you may wonder why you ever worried... or it might cost you a few (lots really) quid.

Depends whether you are talking about your individual income or combined household? My mortgage is almost exactly 40% of my monthly take home, about 30% of the combined (though in reality all my wives is pumped into childcare anyway).

I don't really think it's the % that really matters, it's the absolute. 40% of a monthly take home of £1k would leave you in a much tougher situation than 40% of a £10k monthly take home for example.

you mean the monthly payment is 40% of your net monthly salary?

If so then yes, in 1989 I took out a mortgage where the monthly payment was more than 100% of my salary. fortunately my wife had a job paying the same as me, well until my eldest turned up in 1991 and the second in 1993.

That was a tough ten years but it does improve.

If you want to get a property you have to be committed. you are playing the long game.

I'm paying 40% of my take home in mortgage payments at the moent, but only so that I can get it paid off at 46, I wouldn't want to pay that much til I'm bloody 70.

I don't live in the Deep South though.

...but it can't keep going this way can it?

Well the other option is falling prices and negative equity.

The best we can hope for is 10yrs of stagnating prices, but there's little sign of that.

We're doing the same thing now. Our house (with 6 years left on the mortgage, we're mid 30's) is sold stc.

Made an offer on a place last week that would see more than double what we pay now per month for another 30 years.

As has been said, it's the absolute figure that counts more, our living costs won't change that much if at all. The extra per month on the mortgage is worth it for the new location, lifestyle etc.

What's the point of money in the bank these days? Enjoy it, if that means new house/location then go for it.

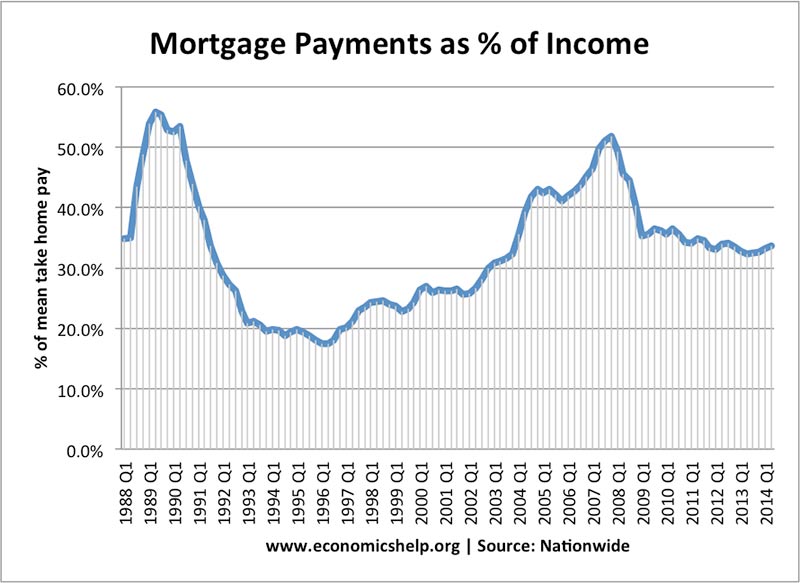

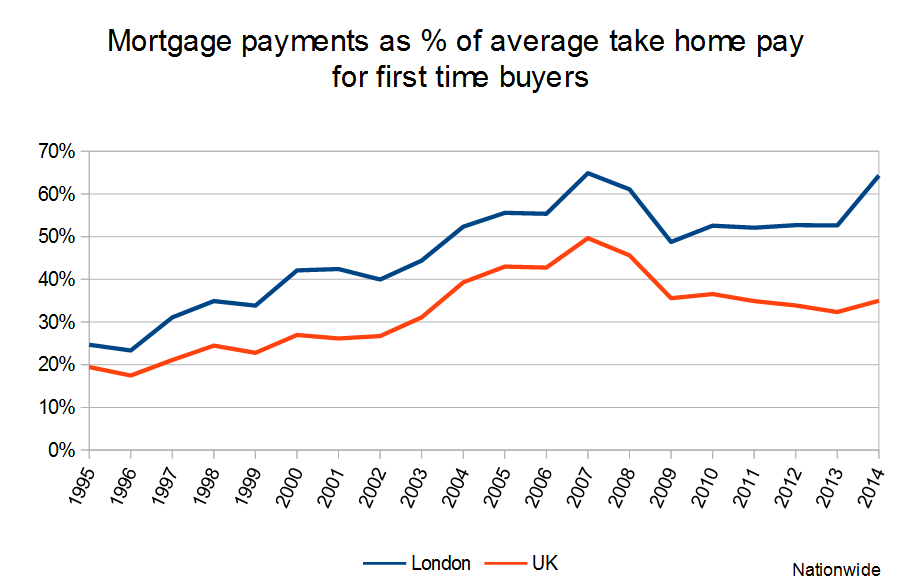

Graph time!

[img]  [/img]

[/img]

[img]  [/img]

[/img]

[img]  [/img]

[/img]

The best we can hope for is 10yrs of stagnating prices, but there's little sign of that.

June 23rd, apparently...

I'm 52, have a £220,000 mortgage that I need to pay off before I'm 65. It scares me.

Noticed on BBC today that house prices have slowed to c8% - so merely 5.75 times inflation.

Lessons learned from the Credit Crunch and longest recession in history = 0.

As for the OP, these days I think they've largely done away with multiples of income or % of income - it's all about income v expenditure so if you're pretty frugal otherwise it might be okay - I wouldn't worry too much about interest rates, the Gov / BOE have lost their balls about increasing them to slow house prices as it turns out that has the side-effect of slowing housing prices...

It's the early 70's thing that would worry me, not sure you should and I'm not sure any bank is going to gamble on your working till then.

I really don't understand how people in London can afford to live if their mortgage payment is above 60% of take home pay. What about other bills and that stuff called food? Also, who actually lends them so much that its this percentage?

Me, not a cat in hell's chance.

But then I'm very much of the view to keep fixed costs down to a minimum and enjoy the other stuff.

I wonder where you live? If you're in the south, it's definitely a very different situation to up north...

Average salaries are higher too so money left for bills will likely be higher even after a big mortgage. Also property in London doubles every 10 years pretty consistently so you can sell up after a while and buy something decent elsewhere so worth a bit of a stretch.I really don't understand how people in London can afford to live if their mortgage payment is above 60% of take home pay.

I wouldnt but thats just me , id rather put my time into my kids than slaving at my desk to live in a nice area.

A few years ago I had an interest only mortgage of £280k on a £40k salary in a very desirable area with repayments of approx £1200 per month.

Sounds nuts but we probably paid the same for our mortgage, as some do for rent.

We did have over £200k equity in the property and the property went up by over £100k in 2 years in the period 2008-2010.

I now have a much more manageable capital and interest mortgage on a smaller property on a less desirable but still reasonable area ,but it's not made anything like the same increase.

I prefer having a smaller mortgage now but as always it's a considered balance between risk NM ow and potential future reward. My brother has just moved from a the same size house in a nice area to a similar size one in a slightly less nice area and is now almost mortgage free.

in 1981 my folks found themselves with a mortgage repayments slightly over 100% of my dad's take home, mum out of work, 2 babies under 18 months old, an 18% interest rate and living off child benefit.

fortunately the interest rates subsided and dad got a promotion but it must have been terrifying! 😯

I pay 40% take home pay in rent for a house far too small for my kids - unsurprisingly can barely save anything.

40% of your take home? Or family take home?

We weren't far off the former when we took it out, but less on our joint income, and it was a high LTV (95%) and thus high interest rate (5.69%), the idea being that after the 4 year fix ends we'll be able to remortgage using any additional equity/anything we've paid off to get a better LTV against what I hoped would be a similar interest rate.

Fix ends next May and I reckon we'll do better on the interest as the base rate has obviously stayed lower than I anticipated. Both of us earn a reasonable amount more now too.

Not sure I'd do it without an end in sight.

We've no mortgage just now and have a house move and hopefully purchase on the horizon. The amount we've been quoted by the lender will allow us to buy what is (to us) a scarily expensive house, and mortgage payments will be 27% of our official take home pay.

I think anything above 30% would make me feel slightly uneasy, 40% I just wouldn't do.

We currently owe approx. £260k on a house worth around £550k.

(No we don't live in a mansion - just a converted bungalow in a nice bit of London)

Repayments are approx. £1300 PCM.

It is about 30% of our combined take-home pay.

I'd not want to spend anymore than this.

Interest rates will not stay at this low level for the course of a mortgage . I would check what the repayments would be if they went up to 10% or more and see if I could still service the mortgage at that rate.

I would go for it with the proviso that you may sell and downsize when you come to retire. Assuming a 25 year term hopefully any kids should have moved out making this a viable option.

Mortgage advisor suggested a 35 year term, to minimalise payments and have the flexibility of a low rate and overpay if you have the spare cash. Apparently past retirement is fine now. She even said some lenders on certain mortgages would go up to 100 years old! I thought they'd tightened up on this stuff. Will explain the prices still going up.

Want to live in Southampton where our work is. Work life balance is good, salaries okay. Obviously good parenting is important in bringing up kids right, but a good school gives them an even better chance.

3/4 beds in chandlers ford start around £500k, in the catchment for the right school add another £30k.

Can get a 10year fixed in low 3%s though noth sure I want to be tied for that long.

From the comments above looks like chucking a massive chunk of take home on a mortgage is the norm.

@Ramsey - my thoughts, so I've fixed for 10 years and I'm trying to pay back capital early.

How does one determine the right school catchment area ?

I live alone, have a mortgage 4.5x my salary, over a long period. Repayments are about 33% of my take home.

Each to their own, it does sometimes worry me, but not to the extent of making me want to move. I didn't choose to buy the house, it kinda became mine... Long story but I transferred the mortgage into my name 4 years after moving in. I don't think they normally given such a high salary ratio these days.

I could move to a smaller / cheaper place, but I like it here, feel that I am improving the house (adding value) and like the area / life style. I can understand why you may want to stretch yourself for the house / area you like.

Oh... my mortgage also runs into my 70's, but I am overpaying while I can to reduce the term (worth considering if you can at all once you've moved in. My mortgage also allows me to withdraw any overpayments if required so I see it as my house fund... pay the mortgage off early if possible, but also a reserve of cash incase the roof blows off)

OP I think it depends on what other savings you have, eg pension lump sum to pay down/off in the future or savings to tide you over when you are not earning.

FWIW I think my first mortgage was 40% of salary but I was expecting career progression/pay rises and I got a fixed rate (10% phew floating went to 16%)

My arse is getting twitchy about borrowing more off the bank to build MrsTGA her extension/new kitchen, although I'll be sticking at 20% of our combined take home just doing it for a few more years (until 60 instead of 55). Probably an unnecessary phobia of mortgages though, and it seems like that's not too bad.

As an aside, when she says 'you're not having a new bike before the kitchen gets done', that means the same as 'as soon as the kitchen's done you can get a new bike', right?

Would I do it? No. People borrowed 4-5times salary then the last recession happened. If inflation jumps could you afford to ramp up repayments?

People I know lived in houses 3times more than what we are borrowing, each to their own. I'd rather live in a normal sized house and relax. I've never been into one upmanship, who cares.

As for Chandlers Ford, 500k? WTF. Where do people work etc to afford that locally?;??! London? Inheritance or massive risk and a Audi/etc lease on the drive? In the last recession lots of people fell foul with their mortgage due to car etc repayments that threw them over the fiscal edge.

My mortgage is currently more than 50% of my take home pay.

Interest rates will not stay at this low level for the course of a mortgage . I would check what the repayments would be if they went up to 10% or more and see if I could still service the mortgage at that rate.

This. Absolutely.

Rates are at historically low levels, put there to stop total collapse of the system. They WILL go up during the term of your mortgage, esp if you go for a 35 year term...

I really would wait until after the referendum before making any decision about getting a tonne of debt to buy a house in London or SE. BTL changes are kicking in, prime London appears to actually be falling in price and inflation has begun to pick up (slightly)...

If you're being advised to take a 35 year term mortgage at that % of take home pay at current interest rates, I'd personally take advice from someone else - that's tantamount to mis-selling IMO - it's a staggering debt burden to take on...

Quick question, of anyone's brain logic is working better than mine.

If you start a mortgage that you can make a lot of overpayments into, and potentially pay off in 10-12 years, are you best to get as long a term as possible to reduce monthly payments and total interest paid over the life of the mortgage?

Its about 50% of mine and I'm paying all of it at the moment while Mrs CD is on maternity leave. Will be tough but manageable until the kid(s) are at school.

3/4 beds in chandlers ford start around £500k, in the catchment for the right school add another £30k.

Have you shopped in the CF Waitrose? It may put you off moving there!

Brooess +1

Anyone who says 'you can/should', get a second opinion from someone without a ulterior motive. Just because you can doesn't mean you should.

Why are we soo debt friendly in the UK?

I still remember my Mum saying 'never buy on the never-ever'.

Ours is £210k and won't be paid off until I retire but repayments are only approx 28% of joint take home pay. Got a couple of small short term debts which will be paid off next year then I'll start overpaying.

Doesn't worry me too greatly as the property is worth around £600k so if we needed to we could downsize.

How does one determine the right school catchment area ?

Reputation, inspectors reports, exam grades. "Right" is subjective, but plenty info available to make that judgement.