UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

Naive question, but if we go completely cashless, surely the costs associated to using cards in small businesses etc would come down as it is the only method rather than an alternative, so that argument is a bit redundant?

As for the elderly, well it would be phased out wouldn't it, so the currently elderly wouldn't have to worry.

And for low income budgeting etc, again that phases out as those used to cash get used to the new way of budgeting via a banking app or whatever and long-term there'll be people who never used cash will just get on with it.

Maybe everyone would need to be issued some sort of basic banking app and card attached to a gov.uk account or something so that everyone has access to an electronic account they can use? Then private bank accounts are a choice on top of that.

Crimminal walks into a ‘shop’ that is actually a front for a money laundering operation

Probably one of the rediculous amounts of turkish barbers there seems to be on every street...

Every time they overlook the small detail of paying the tax due on the £10 worth of takings.

If it goes through the till as cash or card, the tax is still paid. 🙄

Naive question, but if we go completely cashless, surely the costs associated to using cards in small businesses etc would come down as it is the only method rather than an alternative, so that argument is a bit redundant?

Do you really think that without cash the credit card companies will lower their rates?

They are there to make as much money as possible.

Another point is that I can check cash to see if it's legit. If I take payment with a stolen credit card , the victim is refunded by me. So I've lost stock and money.

The amount of cash in circulation is flat rather than growing. It usually goes up in a recession (which is what this feels like even if it's technically not) as people switch from cards to cash to help manage their budgets. Card volumes are flat at the moment, values per transaction have dropped. Long term cash use will decline but it will take a long time to die. Every clearing bank used to have their own cheque processing centres (several for the biggest banks), we're down to one shared by all the banks in Northampton but cheques still haven't died despite the cost of processing. Sweden tried to phase out cash but even they've not gone the whole way. Cash will have a long, slow death and will probably outlast me.

Canary Wharf is cashless. I know that to some, it represents a lot that is wrong with society, but it would be interesting to look at what it means for the myriad retail business that operate there.

If I take payment with a stolen credit card , the victim is refunded by me.

Is that actually the case? I thought in this situation the card company took the hit.

I must have spent less than £50 cash last year. The only useful cash I have is the £5 I have as a tyre boot rolled up in my bar ends. In fact I'm not sure when I last opened my wallet as I always pay with my phone or watch.

I don't see a need to spend with cash when a number of banks/cards are offering cashback with every purchase (eg 1% at Chase)

We pay in at the post office…no fees.

Who do you bank with?

Barclays charge me the same fees if I pay in over their counter or at the Post Office.

If it goes through the till as cash or card, the tax is still paid. 🙄

“if” being the operative word

If I take payment with a stolen credit card , the victim is refunded by me. So I’ve lost stock and money.

Interesting, I thought the CC provider refunded it directly; didn't realise the retailer got stung. Appreciate its probably too much work for a small amount but presumably you could find out which transaction was fraudulent, check the time, check the cameras and work out who it was?

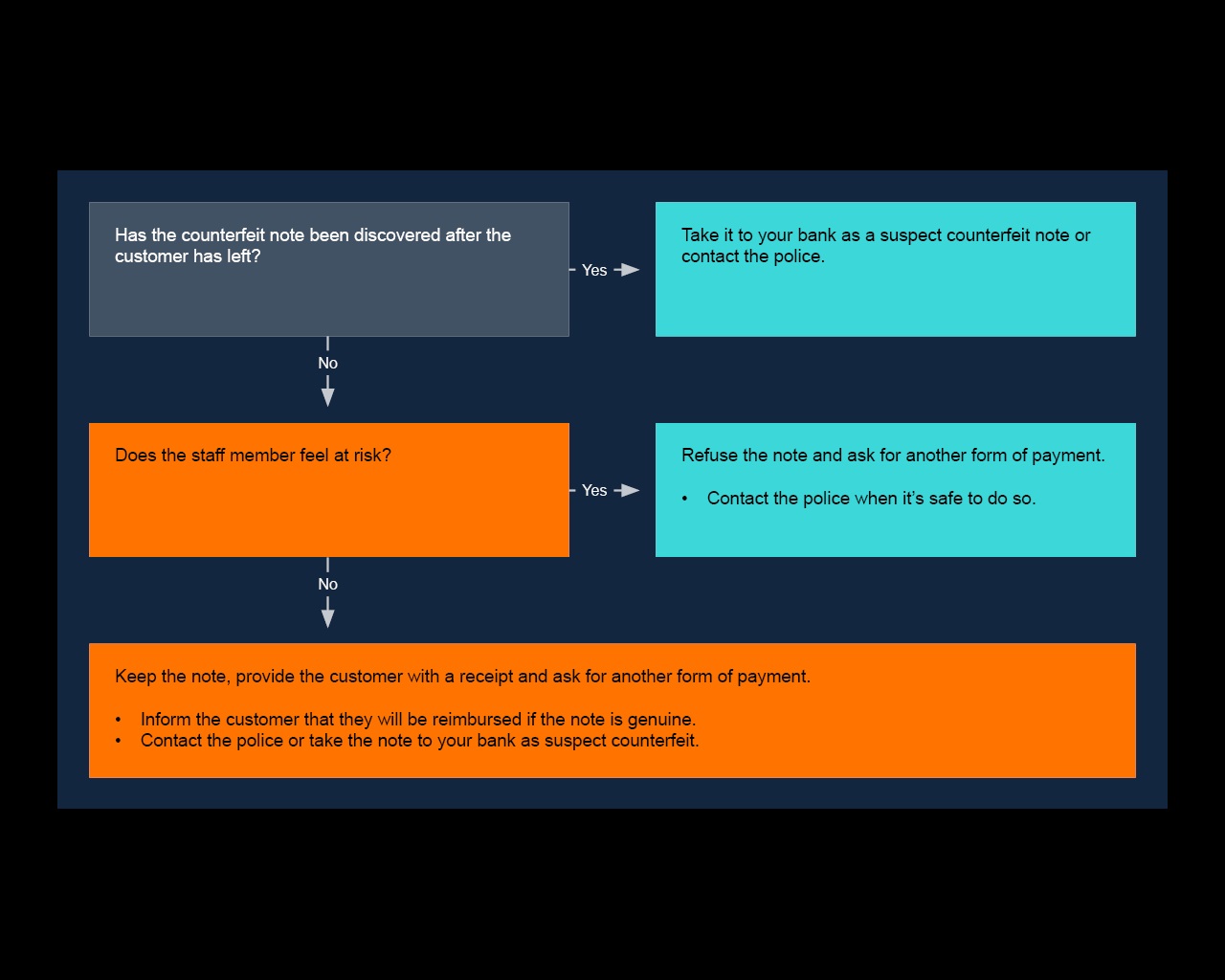

Have you (or any other of the small business owners on the thread) ever taken fake notes to the bank and had them rejected?

If the drawer is all ready open when you pay it won't be going through the books. Your 'local' Inspector of Taxes would appreciate a heads up!

Do you really think that without cash the credit card companies will lower their rates?

Well since lockdown card companies have been competing for business, in 2 years I have changed provider 3 times, each time for a better deal.

I've banked one dodgy note in 17 years.

Local Waitrose got stung last year with £50 notes. I'm probably more diligent than a Saturday girl on minimum wage.

Gobuchul I pay into a personal TSB account and then transfer it to Chase.

If I take payment with a stolen credit card , the victim is refunded by me. So I’ve lost stock and money.

I don't think that's correct.

How could you be responsible?

If it's contactless how would you ever know?

If they have the pin, how could you ever suspect it could be fraud?

Barclays charge me the same fees if I pay in over their counter or at the Post Office.

I'm with Santander (small business ac) bank charges are £40 a month with a deposit limit per year (over 250k?) And a 2.5k deposit limit per day at postoffices (unlimited at the bank). I don't think they do it anymore though....

“if” being the operative word

If you think that a business is a tax dodger don't do business with them - the point is the till logs the transactions which businesses base accounts on, regardless if it's cash or card. If they put the cash in their pocket and not in the till, then yes they are probably tax dodgers. But the same can be said for card machines, I could change the depositing bann to a personal account, Or sell business stock through a personal eBay account and not declare it on my tax return. Just because someone accepts cards, it doesn't mean that they aren't doing tax.

I don’t see a need to spend with cash when a number of banks/cards are offering cashback with every purchase (eg 1% at Chase)

Yes, because the card provider is still making money and charges more than 1% for the transaction 🤷♂️.

Interesting, I thought the CC provider refunded it directly; didn’t realise the retailer got stung.

When a retailer gets stung by a chargeback the retailer has to prove the transaction was taken in good faith with their card provider, this could include checking the time, check the cameras and work out who it was etc. obviously the retailer doesn't get paid for this. If you can prove it was in good faith the card provider usually has some sort of insurance that will cover the retailer and will payout to the defrauded customers bank. However the retailer will have a black mark on it's chargeback rating, too many chargebacks could mean a blacklisting by all card machine providers.

Gobuchul, we had a lady on the phone wanting to buy lots of stuff. All day she kept adding to her order. Fishy as ****.

I phoned World Pay to check the transaction was ok.They said it was.

I tracked the card down to being Australian and the lady on the phone wasn'tand when the lady phoned back I mentioned this and she hung up.

I phoned World Pay to give them a bollocking and to see what would happen to the Australian lady 3k out of pocket. WP said they would take it from us and refund her.

If I take payment with a stolen credit card , the victim is refunded by me. So I’ve lost stock and money.

1. Cardholder notices fraudulent payment on their statement or in app

2. Cardholder disputes the transaction with the card issuer (a chargeback)

3. Card issuer issues a chargeback to the merchant acquirer

4. Acquirer asks the merchant for proof of the transaction or provides or decides not to challenge the chargeback.

5. If the acquirer doesn't provide proof quickly enough, the chargeback stands. In that case the acquier charges the merchant.

6. If the acquirer provides proof, the issuer takes the hit. For example, when a South African bank was hacked and their cards cashed out in 7-11s in Japan, the issuer took the hit.

Someone always pays, it's rarely the acquirer or the card scheme as they just "switch" the transactions. The rules were designed to increase card use, so the cardholder rarely pays. It's usually the merchant or the issuer.

I phoned World Pay to give them a bollocking and to see what would happen to the Australian lady 3k out of pocket. WP said they would take it from us and refund her.

Ahhh - World Pay - now I know why you don't like cards.

We inherited World Pay on our 1st business, 99% online and the software was set up for them.

Absolutely bloody useless and incredibly expensive.

Customer service was terrible, web interface awful, paperwork totally confusing. They had a section titled "summary of summaries" FFS.

Also, you are talking about "cardholder not present" transactions, then you are responsible to take reasonable precautions to avoid fraud. Which you did.

All of the shop transaction are in person, there is no way I could be responsible for the fraud.

I tracked the card down to being Australian and the lady on the phone wasn’tand when the lady phoned back I mentioned this and she hung up.

Would you send stuff to an address that wasn't registered on the card?

Of course if the criminal had taken that money out of the victims purse or sock draw, they would be totally out of luck/pocket with no comeback whatsoever.

Rarely take my actual card out now, risk of loss or pocket scanners in crowded places (not sure if that was ever true or just a rumour)

Apple pay (or the android equivilent) requiring fingerprint or face ID, far more secure.

Not foolproof, as "hit him with this hammer until he gives you the phone and tells you the pin number" is still a possible way of robbing me.

Of course if the criminal had taken that money out of the victims purse or sock draw, they would be totally out of luck/pocket with no comeback whatsoever.

Unless they had home insurance 🤷♂️

Have you (or any other of the small business owners on the thread) ever taken fake notes to the bank and had them rejected?

One £20 note. It wasn't rejected so much as confiscated. I was told they could tell by the feel of the paper but they wouldn't even let me touch it so I could get an idea what they were on about.

Would you send stuff to an address that wasn’t registered on the card?

The lady wanted to pay over the phone and send someone to collect.

Unless they had home insurance 🤷♂️

do they just beleive you when you said you had X amount of cash?

One £20 note. It wasn’t rejected so much as confiscated. I was told they could tell by the feel of the paper but they wouldn’t even let me touch it so I could get an idea what they were on about

I was in Lidl once when the cashier confiscated a £20 note from someone who tried to pay using it. I think their obliged to do this. They customer wasn't happy at all. Understandably if they'd been handed it.

I stopped carrying a wallet at all.

Broadly similar here.

What's actually in my wallet?

Store cards? All on an app. Payment cards, Google Pay. A loose tenner, back pocket. Photo ID, OK this is valid but how often do you need photo ID right now? Police will give you a producer, the vast majority of places like Post Office collection offices who have posters up saying photo ID required never bother to check. What else, stamps? It's a handy place to keep them but I can't say as I've ever found myself halfway down the high street with a sudden urge to post something.

Cash is grubby, think of everyone's hands/pockets that they go through before they end up in your hand. Probably less colds/flu/germs with cashless

I was in Lidl once when the cashier confiscated a £20 note from someone who tried to pay for it. I think their obliged to do this.

This is an interesting one. What is the actual legal stance here, anyone know?

A store is well within its rights to refuse acceptance of payment, both via suspect notes and legitimate ones (despite what the 'legal tender' brigade might have us believe). There is no onus on them to be forced into accepting any form of payment at all.

A bank can and will confiscate fake currency without recompense, sucks to be you.

But can a store take fake money off people and then go "sorry, bye!" Let alone being obliged to even? This feels like shaky ground to me.

I provably use cash weekly, but always carry it.

Often spend less than a tenner in a shop or cafe and ask if they want cash or card - there choice if they want to give 20p or whatever to the card provider for each transaction. A lot of small businesses with small value purchases would prefer cash.

I've also been the only one on a ride able get a snack in a shop or cafe when the internet is down, because I carry an emergency tenner.

Doing away with cash altogether raises all sorts of issues around exclusion, as already mentioned.

But can a store take fake money off people and then go “sorry, bye!” Let alone being obliged to even? This feels like shaky ground to me.

If people try to deposit or use fake cash in the post office this is exactly what we are instructed to do. Same for most of the larger chain shops I believe.

Doing away with cash altogether raises all sorts of issues around exclusion, as already mentioned.

There is a bit of chicken and egg around this though. We could deal with those edge cases if we planned to remove the cash alternative.

But can a store take fake money off people and then go “sorry, bye!” Let alone being obliged to even?

I had this problem the other way round. Back when counterfeit pound coins were in the news they were pretty easy to spot if you looked. I got one in my change and told the cashier, she looked at me like I was insane, gave me a different one and put the dodgy one back in the till.

“It costs to use cash”

No it doesn’t.

Zippy - it does - in your case it costs your time, it costs the post office time, it costs TSB and Chase for processing the transaction, you might not get a bill directly but none of them are charities so someone is paying for the processing.

However it might be costing your customer too - there are fewer free cash machines than there used to be - so they may well be paying to get cash out. Even if they are not paying directly they may have the inconvenience of going to a cash machine, costing potentially both in time, or in some cases in parking costs etc!

I'm mostly cashless nowadays. Have my cards in my wallet, Google Pay on my phone and whatever on my Garmin. So I always have some form of cashless payment method on me.

I do keep a tenner in the back of my phone case for when I'm out on a ride and the coffee wagon only takes cash. Coins just go in a pot at home as I can't be bothered with shrapnel. I'm pretty sure the kids use it and spend it at the local tat shop on dodgy chocolate and energy drinks 🙂

In recent history there are only two occasions that I haven't been able to pay. 1st was the coffee van at Curbar Gap. Usually they take contactless but the machine wasn't able to connect to the internet as everyone at Chatsworth show was smashing the local cell. Was fine I used my emergency £10 and someone else managed to do it via paypal.

Second ocassion was the Cutlery Works in Sheff. They are card only since Covid which is fine until their internet goes down and they have no backup. So had cash but they had no way of accepting or processing it. Funnily enough it emptied out pretty quickly when no one could buy any food or drink.

I don't think we should go cashless for most of the reasons mentioned previously, there should always be an option to use cash.

No - the UK should not go cashless and probably won't go officially

But many changes take place without being planned.

When the big supermarkets are the only places with cash machines will they be tempted to charge for cash withdrawals, which would probably cause many to stop using cash altogether.

I only pay with cash to get some change for the occasions I need it. Mostly I pay contactless with my phone.

But if I am making a small purchase from a small business I do pay with cash, as I assume they don't have the negotiation power to get a good transaction rates.

Tim

No, I don’t always use cash but I do always carry it and I refuse to give a single penny to any business that will not accept cash

I think I'm the opposite; I object to businesses that will refuse to take non-cash payments.

Not until those of us who grew up without any form of digital payment are dead and buried and then only once digital payment is the norm and is accessible for all.