How the hell is that going to help inflation?

I could write more but you get the point. Does anyone think this is a good idea or is it the only tool they have on the box?

Excellent news for us savers. Will check the interest rates going up in the next few days on my ISA.

it will help inflation but both cutting spending and making the uk more attractive to invest in. Whether it'll help it much is a different question.

if you think 3.5 is high, it'll likely be a chunk higher by the middle of next year.

It’s pretty much the only tool in the box and it’s not fit to try and quell inflation that is driven by external political factors in my opinion. If it were demand led inflation then fine - but a lot of people are just trying to get by paying for increased energy costs / costs of the basics / will be fighting mortgage increased costs now if homeowners and probably increased rent if they rent from a btl landlord who has increased mortgage costs.

We’re middle of the road in terms of income and can manage the energy price rise but our fixed rate mortgage going up steeply in July / August is going to be tricky I think. Just hoping we don’t see much more than 4% base rate next year really.

One of the MPC members last month even wrote an article suggesting they don’t think increasing the base rate is going to help much - and will drive us into a deeper recession.

Basic and insufficiently explained reasoning for the higher rate:

Sensible thoughts (in my opinion) from one of the mpc members:

Old timers will tell stories of a time it was was 15% after black Friday. But then again homes were 2.5 times wages. These people own homes and houses now.

I am smugly sat on a fixed rate mortgage for another 3.5 years, with only 5 years of mortgage left. No loans.

Some savings. This is good news for me.

Whilst I feel for people with things like mortgages 3.5% is still very low compared to not many years ago.

Have a look at this and scroll down.

https://www.bankofengland.co.uk/boeapps/database/Bank-Rate.asp

The pertinent question is not so much that interest rates have risen to that level, but why an earth they were at the crazy low levels only a few months back,

Yea, pretty much what Joe and Slab said.

In a convoluted way anything that drives investment into the UK will help, because that increases the value of the pound, which makes imports cheaper, which drives down inflation (whilst driving up wages due to increased productivity which solves the buying power side of the cost of living crisis).

The price of oil is still hovering around HALF what it was 15 years ago, the rest is down to the £:$ rate.

It's one of those cases of cross your fingers and hope that the short term pain is worth it in the long run.

One of the MPC members last month even wrote an article suggesting they don’t think increasing the base rate is going to help much – and will drive us into a deeper recession.

However, a recession would probably help bring down inflation - it's just there will be a lot of collateral damage in the process.

They have one lever and one target!

masterdabber - true, but as Caher pointed out the value/cost of houses in relation to wages is higher now.

masterdabber – true, but as Caher pointed out the value/cost of houses in relation to wages is higher now.

Indeed, though I sometimes wonder in a supply constrained market like UK housing, if low interest rates are actually what caused part of the house price rise.

My father, a professor of politics not economics but still a bright man dealing with social science statistics, had a theory that house prices naturally settled to 3-3.5 times salary. Whenever there was house price inflation it was followed shortly afterwards by wage inflation. Until lower interest rates broke that link.

Now if he was right, then a return to more normal interest rates will probably lead back to unrest until get wage inflation.

And all the signs are that he might have been right.

Normal times used to be around the 5% mark, the artificially low rates since 2008 were never allowed to recover as it would have stifled the housing market growth bubble. Wouldn't be surprised to see it go up to 6-7% before dropping back down slightly over the next 18 months. Lots of pain for people who are highly leveraged.

Normal times used to be around the 5% mark

Even that’s low historically.

Interest Rate in the United Kingdom averaged 7.13 percent from 1971 until 2022, reaching an all time high of 17 percent in November of 1979 and a record low of 0.10 percent in March of 2020.

https://tradingeconomics.com/united-kingdom/interest-rate

Just to balance out the 'rich white blokes of STW' who are sitting pretty with their ISA's and stock portfolios, we'll be lucky next year to hang on to the house that took 10 years to save up for. We've slashed spending this year and in October 23 we'll be going from thin ice to deep shit.

The only way I'll be mortgage free any time in the next 25 years is if I drop dead.

My father, a professor of politics not economics but still a bright man dealing with social science statistics, had a theory that house prices naturally settled to 3-3.5 times salary. Whenever there was house price inflation it was followed shortly afterwards by wage inflation. Until lower interest rates broke that link.

I've always figured they must settle at

Household income - other bills - desired discretionary spending = monthly repayment.

Because ultimately everyone's bidding the max they can for homes. So there's 2 factors,

1) Almost every house is now dual income, which means that really prices were always going to double compared to historical averages.

2) Low rates drove prices up.

So if an average person has the capacity to pay ~£150k over 25 years, then it doesn't matter to them if that's a £132k mortgage at 1%, or £38k at 15%, they're both the same.

masterdabber – true, but as Caher pointed out the value/cost of houses in relation to wages is higher now.

I agree and totally understand that point. But is that a healthy situation? I understand that many people are in the situation of having to take out these massive mortgages in order to get on the housing ladder and many have done so at the very recent low interest rates available.

I am smugly sat on a fixed rate mortgage for another 3.5 years, with only 5 years of mortgage left. No loans.

Some savings. This is good news for me.

Not quite as far advanced as you, but I rolled the dice last year and fixed at 1.6% (best rate I could get with only 25% equity at the time) for 5yrs too, currently reaping the rewards of my pessimism/realism... Shortened the term of the mortgage and upped the payment too, to take advantage of the low interest rate and clear more equity. When the 5yr term ends, I'll be 45 and only have 11yrs left and have more than 50% equity in my home... Not bad considering I was a first time buyer (and on a horrendous rate for the first 2 years as was self employed!) at 38...

Got savings too as was considering a house move previously, which has obviously been shelved (when my stepkids have moved out in a couple of years once they've gone to uni, I'll probably be glad we didn't move!), so be happy to see a better return on those... Even better is I've got about £10k on 0% credit card and finance on my eBike, and that cash is sat in my savings earning interest! 😂

But can't help but feel conlicted, as for all the reasons I was 38 (and in a relationship) until I bought my first house, it's going to make things even harder for first time buyers yet again...

The pertinent question is not so much that interest rates have risen to that level, but why an earth they were at the crazy low levels only a few months back,

I think that is right. They were stupidly low and no room to manoeuvre if they want to stimulate the economy in the future. The thing is - everyone knew they they could only go in one direction, perhaps they are going quicker than people expected but anyone borrowing long term in the last 10 years has surely known that 3.5% BOE base rate was quite possible in the life of the loan.

Lets be clear at current inflation rates if I lend you £100 at base rate you pay me back £103.50 in a year, by which time that is worth about £92 in today's money.

I suspect is also a bit of a message to the government from the BOE - we are going to keep putting rates up until you either sort shit out or something happens to fix it. Now is BOE base rate the right tool for the type of inflation we have - probably not, it effectively increases the cost of mortgages which pushes up cost of living BUT that doesn't mean its wrong to increase the rate - their objective is not necessarily to help with cost of living which is a government social policy.

Inflation can help pay your mortgage off quicker if you get a pay rise. Just over pay as much as you can.

as Caher pointed out the value/cost of houses in relation to wages is higher now.

https://fullfact.org/online/house-prices-1990-2020/

Average house prices 1990 - 2020 have increased 4-fold

Average wages over the same period have increased 3 fold, on a like for like basis.

So the disparity between house prices and multiples of salary are not as high as some would lead you to believe. However - I suspect that he devil's in the detail and while i have no data to support, I hypothesize that the breadth of salaries is wider now, and in particular the 'lower paid but vital jobs' like teachers and nurses are now further below the average than they were comparatively in 1990. Secondly, the huge disparity in house pricing across the country, so in some areas there genuinely is a ratio of average salaries to average house pricing that is multiple times higher than 1990.

I know I shouldn't read below the line on some news sites, but can i also say how happy I am that some are rejoicing in cashing in on the increased rate on their savings while nurses in full time employment are visiting food banks. How marvellous for them!

Excellent news for us savers.

Not really. If you hadn't noticed we're entering a period of financial repression across the western economies where inflation and interest rates will be manipulated to bring down national debts. It's what they did after WWII, it's what they're going to do to get rid of the covid and post-2008 debts. Your savings are going to shrink, not grow.

https://www.investopedia.com/terms/f/financial-repression.asp

Interest rate moves are a crude tool but the Bank of England don't have much else they can play with.

One part of putting up interest rates is to reduce consumer spending, that's the bit which doesn't really work when you're in the middle of a cost of living crisis - people aren't spending on niceties right now!

The other bit of interest rate moves is the impact it has on international money flows and the exchange rate. If the UK becomes more attractive in the money markets due to the better interest rate then money flows into the UK which creates demand for sterling, that demand strengthens the pound and our imports become cheaper. That'd combat imported inflation at least.

There will be more people struggling after the current rate rise and unfortunately the current view is that it'll top out at 4.5% which is going to be a big issue for thousands more households.

Inflation can help pay your mortgage off quicker if you get a pay rise.

https://giphy.com/gifs/uq6ILNBI6g3As

Average house prices 1990 – 2020 have increased 4-fold

Average wages over the same period have increased 3 fold, on a like for like basis.

That must be very localised. Whilst for instance in Reading you may earn 37K try and find any house 234K.

One of my mates, a chippy has a 750k house which he bought off the council for 30K in the early 80's.

That must be very localised.

It is an "average" that will also include all the houses sold for £1 with interest free loans to do them up in all the deprived areas in the north too...

So not at all representative of most peoples real world situation...

one of my mates, a chippy has a 750k house which he bought of the council for 30K in the early 80’s.

My next door neighbour bought his house brand new in 1971 for £2750... I bought my almost identical house next door in 2018 for £195k... 4yrs later it's now "worth" about £240k...

Avg persons wage in 1971 in the UK was about £3500 per year... Or 1.25x what my neighbour paid for his house...

Avg persons wage in 2022 in the UK is about £28k... Or approx 0.125x what our houses are worth now...

In real terms, house values have gone up 10x as much as wages have in 5 decades, at least where I live... And I live in Worcester, a relatively affordable area compared to many places across the country, especially in the South East!

https://fullfact.org/online/house-prices-1990-2020/Average house prices 1990 – 2020 have increased 4-fold

Average wages over the same period have increased 3 fold, on a like for like basis.

So the disparity between house prices and multiples of salary are not as high as some would lead you to believe. However – I suspect that he devil’s in the detail and while i have no data to support, I hypothesize that the breadth of salaries is wider now, and in particular the ‘lower paid but vital jobs’ like teachers and nurses are now further below the average than they were comparatively in 1990. Secondly, the huge disparity in house pricing across the country, so in some areas there genuinely is a ratio of average salaries to average house pricing that is multiple times higher than 1990.

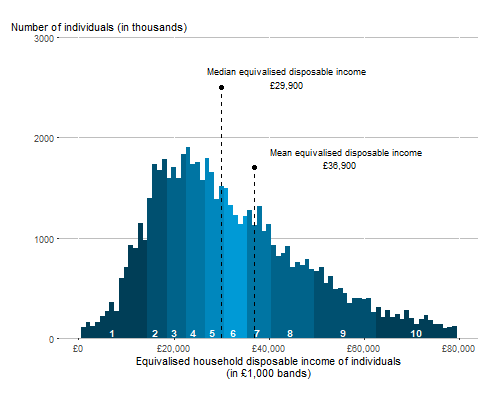

This also highlights the trouble with using the mean for the average UK household income, it skews it. If you use the median it's £31,400, compared to a mean household income of £37,100 for 2021, (2020 data below).

There are two basic contradictions.

First, inflation vs recession. The traditional cause of inflation is too many people spending money and so competing for goods and services, the price goes up in a buyer's market. So to stop inflation, you put up interest rates to reduce people's spare money and make it more profitable to save. But now, we have a recession, to avoid that Government want growth (not to Truss extremes but still want it) which means people spending money. The current inflation is driven mainly by increased prices further up the supply chain, so it's not going to respond to supply and demand in the way economic theory suggests.

Second, house prices. Governments have tried to keep prices high, because if they fall people are stuck with negative equity. Hence the reason for the stamp duty holiday to stop them falling in the pandemic. Low interest rates and two income households enabled them to keep rising. Building societies still remember the last time prices dropped, and don't want to get caught having lent more than the house is now worth, as repossessions then mean bad debts, so they insist on big deposits and high salary coverage. So both rising house prices and falling house prices are seen as bad - what we really need is a way to freeze them until they're affordable.

lower paid but vital jobs’ like teachers and nurses

There's a whole lot of hard working well qualified people who earn much less than teachers or nurses. I'm one. I really doubt if reference to the average wage is very useful. Perhaps the modal wage might be more informative?

What I'm really saying is our concern ought to be aimed at assisting those who are most vulnerable - the poorest.

Old timers will tell stories of a time it was was 15% after black Friday. But then again homes were 2.5 times wages. These people own homes and houses now.

However, surely it’s not ‘old timers’ who own their homes pushing up property prices - it’s those willing to pay 8 times their combined salaries. They took a gamble (with only poor choices available) that interest rates would stay low, the cost of living would remain stable, that they’d stay employed, … Unfortunately things are not going to plan.

Very few people warrant having a finger pointed at them imho. Apart from landlords 😏

However, surely it’s not ‘old timers’ who own their homes pushing up property prices – it’s those willing to pay 8 times their combined salaries.

^^ That. ‘rich pensioners’ could easily have paid their mortgage off 20 years ago.

Hence the reason for the stamp duty holiday to stop them falling in the pandemic.

Aside the pandemic wouldnt have necessarily pushed prices lower but instead given a useful freeze to the market. There would have been unlikely to be negative equity vs just low sale rates.

As it was they just stoked prices higher and threw away needed tax money.

Great plan Rish!

Possibly only beaten by the eat out to spread it about

what we really need is a way to freeze them until they’re affordable.

How long are people going to need to wait?

If Starmer wants to be a gammon he needs to put forward a 100% tax on Forriners buying our houses.

That will burst the London bubble.

British Homes For British People.

Depends which commentator you listen to on rates. The bank I work for is working to 3.75% in Feb or March and that it probably won’t go higher. Although that view is from a few weeks ago and changes all the time. Depends if you’re coming from a dove ish or hawkish viewpoint really.

Mpc 9 members - 6 voted for 0.5% rose today, 2 wanted lower or to hold and 1 wanted 0.75% again. So they’re getting further apart. I think for Jan they should hold fire and see what effect (if any) the rises they have already done make. I’m not convinced they’ll make any difference as everything is driven by politics / war / Brexit at this moment in time.

Looking at all the disasters in economies over the years I remain to be convinced any changes in base type rates really help anything. Most of it is based on confidence in the market outside of political conflicts. That’s just on a layman basis though - I’ve never studied economics properly.

Feeling smug having fixed at a low rate for seven years. Was stuck on 4.99% for years after 2008, whilst all around me were getting nice low rates. I was in negative equity and household income had dropped.

Taking the opportunity to overpay a bit.

Really feel for those that will struggle. It's not easy especially if something like the heating or fridge packs up destroying your budget or growing debts.

A quick (& far from exhaustive) googleshows that average earnings in the UK in 1990 were £14k (rounded up slightly) and the average house price was £57k. So just over 4x earnings.

Figs for Nov 22 are £33k and £295k respectively. Which is a growth of approx 2.5x on the salary and approx 5x on the house prices. So not sure where the 3x and 4x stay referenced above came from (I got involved because that seemed iffy to me).

So, in simple terms this equates to house prices being 4x average annual earnings in 1990 and over 9x now. Obviously this is highly simplified, doesn’t factor in regional variations, different ways of measuring, dual income households etc. Or indeed the interesting point that a small mortgage at very high interest rates would incur similar repayments to a large mortgage on much lower rates.

Either way the state of our housing market, particularly in the SE but increasingly elsewhere too, has to correct at some point to a more sustainable multiple against income. How, when or why? Your guess is as good as mine..

I don't think interest rates are the only lever. The government could do something proper about energy prices - either at the supplier level or the demand level - and that would result in a reduction in headline inflation figure.

Access to cheap money (anyone remember self certification mortgages? ) and the spike in buy to let is what got us in this situation. When the financial system collapsed in 2008/9 what should have happened was a large swath of the population taking a bath because house prices went through the floor.

Gov's couldn't allow that to happen so massive quantitative easing and effectively zero interest interest kept the economy alive and allowed house prices to continue inflating until we get to, well, here.

state of the rest of the economy - it doesn't matter if you didn't get a pay rise because your house is up 20% this year. hoorah!

The housing market in this country is fundamentally broken - its too often an "asset class" for overseas investors and pension funds rather than something that builds homes for people to live in.

The insidious side effect of house price inflation is that its allowed the gov hide away from dealing with the lack of productivity improvements and the poor

And of course, like all bubbles, its great as long as the bubble keeps gettting bigger.

It is an “average” that will also include all the houses sold for £1 with interest free loans to do them up in all the deprived areas in the north too…

You mean one street in Liverpool?

Old timers will tell stories of a time it was was 15% after black Friday. But then again homes were 2.5 times wages. These people own homes and houses now.

Not so sure - bought my first house with a 17% deposit and maxing 3 times my salary, and lost all that money when I sold it 5 years later.

The problem is everyone got used to silly low interest rates, and no one from the government down to us ordinary folk thought what would need to be done and prepared for when they had to go up.

There is no sensible economic logic to this.

Make money more expensive because it's already more expensive.

It benefits the asset class and drives inflation.

A while back several economists I follow were talking about an engineered recession. They were spot on.

Inflation will come down because of the nature of reporting it YoY. That can still mean things are getting more expensive just at a slower rate.

Basically the small guy gets shafted to keep the big guy happy.

If recession was the mechanism by which we control inflation - that's like giving a drunk a car to slow traffic down.

I personally don't think things have actually bitten down hard yet.

There is no sensible economic logic to this.

Yes there is.

Basically the small guy gets shafted to keep the big guy happy.

There you go, I knew you’d get it.

The UK is being run exactly as predicted back in 2016 by those warning were a vote to leave the EU would take us. We know who this country is being run for, and it sure as hell isn’t “the little guy” or SMEs or workers.

The low interest rates combined with buy-to-let meant that in some areas every house that came on the market was bought (at inflated prices) by people who only wanted to rent them as holiday lets, not even living in them as holiday homes. Not unsurprisingly this meant that local working people had as much chance of buying a home as winning the lottery. If these people suffer some financial distress, and these same houses come back on the market at reduced prices, I consider that a win.

I have hopes that the proposal to double council tax rates for unoccupied/holiday lets comes about, and frees up some housing stock.

Excellent news for us savers. Will check the interest rates going up in the next few days on my ISA.

Inflation at +10% and you might get 4% interest..., crack open the Champers!