HMRC says [url= http://www.hmrc.gov.uk/incometax/basics.htm ]£32,011 to £150,000 Higher rate[/url]

BBC saying today [url= http://www.bbc.co.uk/news/uk-politics-26572914 ]There have been calls for a rise in the level at which the rate kicks in, which is currently £41,150[/url]

So what is it?

Isn't the HMRC quoting the amount after your tax free allowance?

Is the HMRC figure after tax free allowance has been taken off?

32 + your 10 tax free

Grr, too slow.

After your allowable expenses and any tax-free allowances have been taken into account, the amount of tax you pay is calculated using different tax rates and a series of tax bands.

Ahh yes, clear as mud by them.

Cheers

Hmrc even tell you on your link....

Haha too slow

HMRC figure of £32011 is [i]taxable [/i]income, excluding the personal allowance of £9440. Add them together you get £41450.

As Brassneck said so £32,011 plus £9,440 2013/14 or £10,000 2014/15

craigxxl...are you an accountant perchance?

Whatever gives you that idea 🙄

Its a shit thats what it is.. 😉

Whatever gives you that idea

🙂 You always seem to have pretty accurate answers on these threads. Just, erm, docking some information for some possible questions. 😉

Hmm wish I was paying 40% tax

Hmm wish I was paying 40% tax

Why?

It's spank.

it's 40% up to £100K and then because of the loss of the personal allowance on a pound for pound basis for the £20K above that effectively becomes a 62% marginal tax rate i.e. for every £2 earned you lose £1 allowance and still pay the 42% tax and NI.

Which is nice work if you can get it but seems a bit bonkers when people on £150k only pay 45% tax on income over that.

Hmm wish I was paying 40% tax

Pitfall of being self employed - one good year and instead of being able to save for a rainy day, they just want to take 40% of it off me 🙁

They didn't give me anything back when I had several bad years after the recession struck.

Can't you setup a limited company and manage your business tax affairs through that ?

Can't really complain if you're earning over £100k, you're not exactly poor.

It's a good way of identifying the champagne socialists. They're the ones who think it should be a higher %age, but only start above what they earn.

Pitfall of being self employed - one good year and instead of being able to save for a rainy day, they just want to take 40% of it off me

Run it as a ltd company and keep the money in the company account rather than your own?

We'll never see the 40% band rise any significant amount for middle incomes, they'll just keep bumping the tax free element and call it a win for 40% tax payers.

Can't you setup a limited company and manage your business tax affairs through that ?

Yes, but general opinion is that you need to earn over around £50k to make the switch beneficial so the occasional (twice in 10 years) foray into higher band suggests it isn't for me just yet.

Pitfall of being self employed - one good year and instead of being able to save for a rainy day, they just want to take 40% of it off meThey didn't give me anything back when I had several bad years after the recession struck.

You should be thinking about going limited and saving quite a bit in taxes. If you're not due to it being a good year then make sure your payments on account reflect that too.

You don't "escape" paying 40% even if you have a Ltd Co 😉

footflaps - Member

Can't really complain if you're earning over £100k, you're not exactly poor.

You're not wrong, but I think robdixon's point is that people earning between £100,000 and £149,000 are paying a lot more tax then people earning £150,000 and over

[quote=bikebouy said]You don't "escape" paying 40% even if you have a Ltd Co

You do if your personal income taken out of the business is set to be below the 40% threshold 🙂

Our joint income wouldn't hit the higher tax bracket 😀

You're not wrong, but I think robdixon's point is that people earning between £100,000 and £149,000 are paying a lot more tax then people earning £150,000 and over

Only at the marginal rate, not overall.

[quote=shermer75 said]footflaps - Member

Can't really complain if you're earning over £100k, you're not exactly poor.

You're not wrong, but I think robdixon's point is that people earning between £100,000 and £149,000 are paying a lot more tax then people earning £150,000 and over

I believe that this is not the case.

Ay thats true, but why leave all that loverly dosh sitting in the Co Bank Account when there are bikes to pay for 😉

Pitfall of being self employed - one good year and instead of being able to save for a rainy day, they just want to take 40% of it off me

No, they want to take 40% of the [b]extra[/b] lovely money you've earned that year, not 40% of [b]all[/b] the money you've earned.

I've tried explaining that your tax rate is really total net earnings over total gross earnings, but people get fixated with the marginal rate at the highest level and think that's their tax rate.

If you have a pension and claim tax relief then you can end up paying a lot less than the tax bracket percentage as you get all the tax back on your pension.

I believe that this is not the case.

Correct, the gap narrows at an increasing rate, but you never pay more (absolute or proportionally) as your salary increases.

[url=  ]Fairly clear way of showing it[/url]

]Fairly clear way of showing it[/url]

If you have a pension and claim tax relief then you can end up paying a lot less than the tax bracket percentage as you get all the tax back on your pension.

Salary sacrifice share save schemes, Cycle 2 Work and child care vouchers are other good ones, as a sort of tax saving. You don't really see the money in you pocket, or maybe not for a while at least, but it makes something you have to buy more efficient tax wise.

Also useful for child benefit in the > £50K earnings, but that's a whole other thread I'm keeping well out of!

[i]You don't "escape" paying 40% even if you have a Ltd Co [/i]

*Cough* Starbucks *Cough*?

One benefit of being in the 40% tax bracket is getting 40% out of them on my personal pension

One of my colleagues, who is approaching retirement, put his entire salary into his pension one year and lived off his wife's salary. He paid no tax at all even though he's in the 40% bracket....

Salary sacrifice share save schemes

Our share save schemes are done on net salary 🙁

Shares saves (or whatever your company calls them) are out of net salary, share purchase are out of gross (provided held in trust for 5 years)

footflaps - Member

I've tried explaining that your tax rate is really total net earnings over total gross earnings, but people get fixated with the marginal rate at the highest level and think that's their tax rate.

You think that's tricky. Try telling people that a flat tax rate combined with an allowance at lower levels still produces a progressive tax system. We have had some fun with that one on here before!!! 😉

I must admit in my youth I thought it was absolute bands, so if there was a threshold at £100,000, I thought you effectively took home more if you stayed earning £99,999. 😳

MoreCashThanDash - Member

Our joint income wouldn't hit the higher tax bracket

You can't have a lot of dash then.

One of my colleagues, who is approaching retirement, put his entire salary into his pension one year and lived off his wife's salary. He paid no tax at all even though he's in the 40% bracket....

Haven't they clamped down on that now? There's a cap of £40k p.a. for this coming tax year, and a lifetime cap as well.

Sadly, not a problem I need to grapple with.

One of my colleagues, who is approaching retirement, put his entire salary into his pension one year and lived off his wife's salary. He paid no tax at all even though he's in the 40% bracket....

He must have only just been in the 40% bracket then, that's a spot of good fortune!

It was a few years back, before they lowered the limit to £50k.

Why would I like to pay 40% tax? Because my income would have more than doubled .

Ay thats true, but why leave all that loverly dosh sitting in the Co Bank Account when there are bikes to pay for

Dividends dear buoy, dividends.

And as for leaving any spare cash in the Co Account - well, your partner needs a salary too, dependent on how much her day job pays, because she is your company secretary, ISN'T SHE?

Oh and you know that car you use for work? 50 pence per mile for the first 10k and 25 pence thereafter can soon add up.

Add in pensions and...

VOILA, no corporation tax to pay and Ltd Company broke even this year 😉

That's a great result for you. Do you actually feel good about not paying any tax? Hospitals, schools, roads - do you ever think "hmmm, it would be nice if these were a bit better looked after" ?

shifter - MemberThat's a great result for you. Do you actually feel good about not paying any tax? Hospitals, schools, roads - do you ever think "hmmm, it would be nice if these were a bit better looked after" ?

If that comment is aimed at me, then wind yer neck in - it was a hypothetical scenario. I'm a Sole Trader and pay plenty of tax thanks.

However, even with the above, I'd still have paid plenty of tax. Where does your 'not paying any tax' nonsense come from?

Oh I see now, it was hypothetical. The sole traders I know are quite willing to share that they pay as little tax as possible so if you're paying plenty then I commend your public spiritedness. I'll put my neck wherever I like thank you!

Maybe the sole traders you know are a tad dishonest then? Money in/money out, pay the due rate of tax on the difference. You can make up any figures you like, as long as you can confidently back up those figures for the next 6 years.

So, you mump at me for having a pretend Ltd Company and utilising the tax system, then you seemingly tar me with the same brush as your dodgy mates, with your veiled praise of my public spiritedness.

Your neck still seems to be out, but I'm not sure why. What's your problem?

If your tax free allowance is reduced to £7k because of a company car, do you start paying 40% earlier or does it not work like that?

It does. If you have a K code then you've used all you tax allowance up and the excess benefit in kind is taxed on top of your salary.

If your tax free allowance is reduced to £7k because of a company car, do you start paying 40% earlier or does it not work like that?

Yes, you would start to pay tax at 40% at a lower salary than someone who didn't get a company car. Bear in mind that a company car is still cheaper than paying for the same car yourself.

Ok. So if you just tip into 40% by a few quid, does the bike to work scheme work at 40%?

Cycle to work payments come out of your gross earnings before taxes so reduce the taxable amount. If you were just in the 40% bracket then then the payments may drop the remaining salary below the higher rate threshold.

Thanks that makes sense.

If you are a sole trader/partnership you can't use the bike scheme.

But you *can* buy a bike through the business and it's an allowed expense and you can claim the VAT back 😉

You're not wrong, but I think robdixon's point is that people earning between £100,000 and £149,000 are paying a lot more tax then people earning £150,000 and over

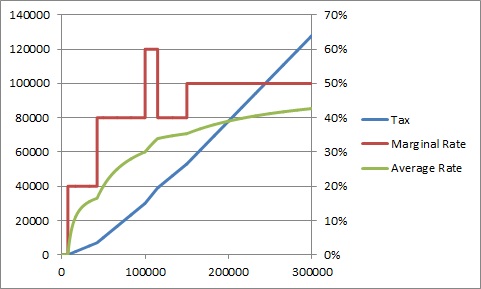

No, it's even more bonkers than that. The marginal rate goes up to 62% between 100k and 118k or so whilst they remove your personal allowance, then back down to 42% until you hit £150k then up to 47%. This is neither progressive nor regressive, it's just bonkers.

What's even more silly is that because its been implemented by removing your PA, it's almost impossible for the PAYE system to get your tax right, because your tax code becomes dependent on how much you earn, making the tax system even more complicated and difficult to administer. This has been done because the notion of high earners getting a "tax free allowance" is politically unacceptable, even though you could achieve an equivalent effect much more simply by reducing the £150k threshold.

Further, because the £100k and £150k thresholds are seen as the preserve of the "rich", there's never any discussion of raising them in line with inflation which means that ever more people will creep into these brackets. Already £100k today is probably equivalent to less than £90k when the change was introduced, and it will continue to affect more and more people, just like the 40% band.

I've no problem with higher rates for higher earnings, but it'd be really nice if it could be implemented simply and logically.

Marginals rates are meaningless, all that matters is the overall tax rate on all your earnings.

Plus you can easily avoid the higher marginal rates by investing in SIPPs etc.

Most decisions we make are "marginal" hence it is a central theme of economics. So would disagree with the idea that marginal rates are meaningless.

+1 Marginal rates are what drive decisions around whether it's worth working harder and trying to earn more.

No, it's even more bonkers than that. The marginal rate goes up to 62% between 100k and 118k or so whilst they remove your personal allowance, then back down to 42% until you hit £150k then up to 47%. This is neither progressive nor regressive, it's just bonkers.

Maybe, but the total rate still always goes up with earnings, just not in a smooth curve.

[img]  [/img]

[/img]

I like marginal rates because I can tell my boss to shove the overtime where the sun don't shine because for the next few years it'll net less than it did when I started at the company!

+1 Marginal rates are what drive decisions around whether it's worth working harder and trying to earn more.

Which always makes me wonder why high earners are de-motivated to work harder if we take to much money off them, yet low earners / benefit claimants will be motivated to work harder if we take money off them?