UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

Coke & hookers then waste the rest.

so if you’re a man, who has a job where it’s possible to keep working after retirement age, then it may well be best to. This also alters the pension equation quite significantly.

S’what I’ve done. I was doing a job I enjoyed that payed fairly well, I’d paid off my mortgage so I kept on going. Until I got made redundant at the end of March, so I applied for my state pension. I’m 69 next month, I’ve got £948 pension, although that may go up 10.5% soon. I also got a £12,300 lump sum, which isn’t to be sniffed at.

I’ve also still got two of the six personal pension accounts I set up to pay off my mortgage, and a whole bunch of workplace pension plans set up by employers over the years, and they’re all in the hands of a local financial advisor who’s having to deal with a bunch of people who really don’t seem to want to let all that money out of their clutches. No idea why that might be… Hoping soon to find out how much I’ll have to top off my state pension every month. Be nice if it gave me a final salary equivalent.

24% is super generous benefit…or am I just an impoverished charity worker?

Both! 😅

I am a poncy public sector worker and I get 11% employer contribution. MrsDoris is private sector and gets 5%.

24% seems absolutely astonishing to me.

I put in 7% and my employer puts in 14%. I thought that was industry leading. Maybe it is for retail.

Pension planning is tricky. You don't know how long you will live for. Or how much a week you will need, immediate needs can be calculated, but in 5 or 10 years time, who knows

I hate threads like this, it makes me realise how unprepared/oblivious I am to what I should be doing. And I’ll be 40 in a couple of weeks so should probably get on it

I'll be 50 next year, have no clue about retirement!!

Mrs TJ had a 25% employer contribution in one job. It came about because they were on public sector payscales ( but a charity) but wanted to give the staff a significant raise and this was the easiest way to do it. Highly unusual tho

no clue about retirement!!

The basics are really quite simple. At 67 you should get about £10k per annum from the government to live on. On top of that, take whatever you have saved up by whatever means and divide it by the number of years your are going to live for. That’s your new annual “Salary”. Roughly speaking you should be aiming to have enough money to fund the lifestyle you’d like/need to live in for that period.

Assume you live to 87, and want to live on a £30k a year lifestyle you need another £20k for 20 years or £500,000 (it’s 25% more cause it’s taxed). Assuming you have nothing, at your age you need to save approx £2600 a month to reach that target at 67.

IANAFA of course and this is a gross simplification of all the facts I’ve assumed and more.

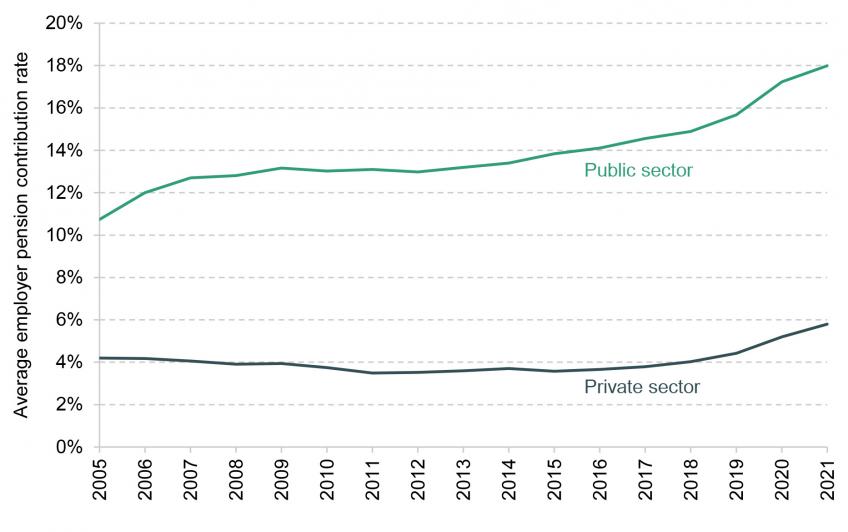

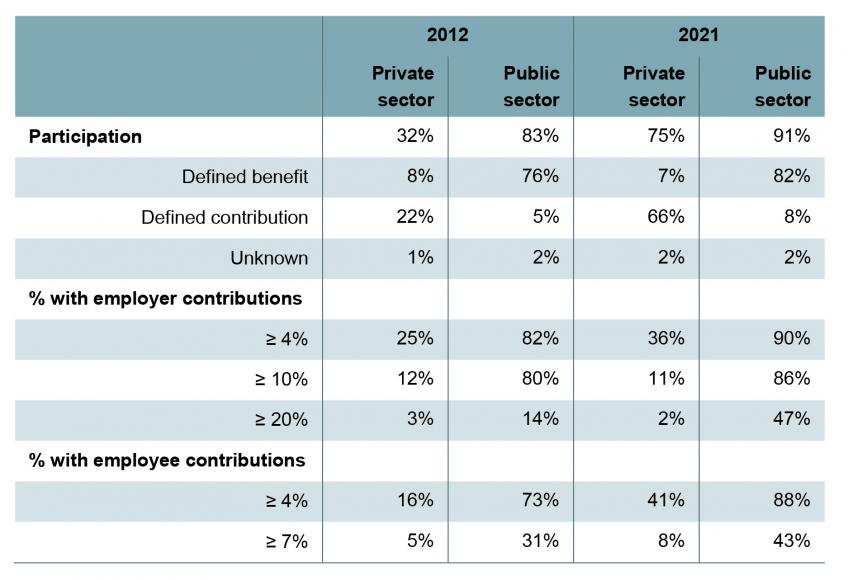

Average public sector employers contributions is 18%

47% of public sector employers contribution are greater than 20%

I guess the big question these days is what is retirement? For many people there may never be the opportunity to 'stop working'. But that is ok if there are jobs available and suitable for the people who want/need to continuing working. Clearly some jobs take a physical/mental toll on people and simply carrying on working is not possible.

Despite my job being office based which I could continue to do, I want to stop at 55 and take some time to travel. That doesn't mean I will never work again (but I'm also not naive and recognise getting a job at +60 may not be easy).

So we saved hard and I've been lucky in my career so now have a nice pension pot across 2 DB and 1 DC schemes which means removal of the LTA was welcomed. This pot plus savings in ISAs means I can realistically stop at 55 and focus on other things.

Was this the right decision - who knows!? I know people my age with no savings. They spent their late teens and twenties (some even their thirties,) paddling and climbing whilst I was working and paying into a pension. They now look at me and wish they had saved more. I look at them and wish I had paddled, climbed and travelled more.

Not sure what I'm trying to say to be honest. Enjoy your life, try and be happy, be nice to people and don't worry too much about retirement 🙂

and am paying a load into my company scheme, with annual lift outs to a privately managed Investec fund.

Lift outs sounds interesting. My company adds NI to my contributions so effectively i think i get my money doubled compared to taking cash, but my 6 year old fund is still worth almost exactky what i put into it. I was wondering if i coumd transfer some of the money out to a less shit fund...

There is so much conflicting advice as to what size of pot is enough to maintain a good lifestyle.

Agreeed, but its no surprise given that people cant even agree on what a decent/ liveable/ comfortable salary is.

I'm working on the basis of £600k pot being very very comfortable for a person as part of a couple. £2k pcm minus a tiny bit of tax perhaps indefinitely. More if you're happy to eat into the principal

I can realistically stop at 55 and focus on other things.

Was this the right decision – who knows!? I know people my age with no savings. They spent their late teens and twenties (some even their thirties,) paddling and climbing whilst I was working and paying into a pension. They now look at me and wish they had saved more. I look at them and wish I had paddled, climbed and travelled more.

Not sure what I’m trying to say to be honest. Enjoy your life, try and be happy, be nice to people and don’t worry too much about retirement 🙂

Lovely 🙂

The basics are really quite simple.

Yep, thanks I understand the concept of retirement and that I'll need some money. What I have no idea about is how much I'll have when I get there!

I’m working on the basis of £600k pot

Currently or at the end ?

I'm hoping/thinking 55, but i expect it'll be closer to 60 potentially.

35 years contributions in a 1/100 scheme means, roughly, you’ll get a pension of a third of your salary. That’s quite an income drop on retirement.

Yeah, but limited tax, no pension outgoing, no NI contributions, possible state pension, AVC pot all means that total annual income is a lot higher than it seems on paper. Coupled with no mortgage, no energy costs and limited costs to run a car...you should have a lot of disposable income.

So, assuming all debts including mortgage paid off, how much do you think you need as an annual pension to live a comfortable life? No luxury cruises to the far east but regular eating out and a bit of travel.

Was this the right decision – who knows!? I know people my age with no savings. They spent their late teens and twenties (some even their thirties,) paddling and climbing whilst I was working and paying into a pension. They now look at me and wish they had saved more. I look at them and wish I had paddled, climbed and travelled more.

I fall into the 'worked for a charidee most of my life, spent many happy days outdoors, now worry about my pot' category. Though with mrs_oab's health of recent, I think a case of 'one life, live it' is becoming our attitude.

For me its around £15000 a year cos that is what i have. I'm 62 so that will go up at 67. I do have a lump of capital tho which is a big safety net

You have 2 choices. Decide how much money you need and work until you have tbat much or decide when you want to retire and live on how much money you have then..

Coupled with no mortgage, no energy cost

no energy costs? how?

35 years contributions in a 1/100 scheme means, roughly, you’ll get a pension of a third of your salary. That’s quite an income drop on retirement.

That's the question, isn't it? Individually, I think it would be around £30k minimum. Council tax is still high, food is a lot, there will be other utilities, which could easily still keep outgoing at over £10k. I'd still want to be saving a little for unforeseen and children will almost certainly require support, so maybe another £10k. £10k of disposable income would be nice for stuff and things. As a couple, that could reduce to maybe £25k as the bills are shared?

So, assuming all debts including mortgage paid off, how much do you think you need as an annual pension to live a comfortable life?

its all a matter of opinion - but heres one orgs stab at it

https://www.retirementlivingstandards.org.uk/

minimum standard of living £12800 per year

moderate £23300 per year

comfortable £37300 per year

all for a single person, not couple

Currently or at the end ?

At the beginning of retirement. Or the end of working. Defo not now 🙁

I’m hoping/thinking 55,

Me too. But the missus just laughs at me.

.

35 years contributions in a 1/100 scheme means, roughly, you’ll get a pension of a third of your salary. That’s quite an income drop on retirement.

Yeahbut, as daffy alludes to there's loads of stuff that changes. Currently I only actually spend about 29% of my salary. The vast majority goes on tax, NI, pension contributions and savings.

no energy costs? how?

Massive solar/electric/ASHP system.

My solar plant means my electric will be zero cost this year. If I double the size of the array, couple it to an ASHP and a thermal store, it'll remove the need for oil at £900/y.

Water will be the only cost.

The comfortable level is well above average income and more than I ever earned as a nurse

Somewhat out of touch

Oh FFS TJ. Let's not do this again. That's why they've named it " comfortable".

Thats the whole point of what they're saying. It's the upper end, the lucky ones, the rich ones...

Of course it's above bloody average, the top end is always above bloody average. That's why it's top end.

HTH

it is very hard to assess, I set my target, which I will not achieve, on retiring early 60's with a £1M pot. The reality will be 2/3 of that at very best. Wife would probs retire same time, and has a poor NHS pension. So state pension will likely kick in somewhere around 6or 7 yrs post retirement, and using the various calculators I felt that an annual personal retirement income of 40k would be nicely comfortable, as an aspirational figure.

Also, the need is not linear, and I have very much witnessed that with my own parents, who retired early 60's, with my dad passing away a few years ago in his late 80's and my mum still around, aged 90.

In the first 10 years of their retirement they spent a shed load, as they were living overseas on their sailing boat most of the time, with travel back to UK a few times a year. By the time they got to their late 70's they were back in UK, and then sold their boat and life became a lot slower, and I reckon their spend probably halved. My mum is on her own and quite independent, no car anymore, and probably spends under 1k a month all in, with coffee shops, lunches a few times a week and twice a week cleaner/home help person.

So by my reckoning, hoping to live for 25 years post retirement, I think we can budget on retirement income in the first 10 years eating up 50 - 60% of the pot, then reducing commensurately for the remaining 15 years or however long we last..

Whether there will be any inheritance for our kids will depend on the latter I guess !

This is a somewhat depressing thread.

My employer pays 8% and I'm paying nothing. I need to start paying in soon. I'm 40. I do have a previous pension but that isn't much. I decided when I moved here to England and started this job that I needed the disposable income to help me live as I was living on my own, but then that makes it more difficult to sacrifice part of my income. I then got a mortgage for the first time last year which is a term length that should see it payed off before 65. Now with increasing rates and the cost of living, paying into the pension and taking on a larger mortgage next year (renewal time) means that I'd be taking quite a huge hit if I started paying into the pension. Not ideal at all, but that's the reality. I don't lead a lavish lifestyle at all.

The generalist

Its totally out of touch. They are saying that to be comfortable in retirement you need an income significantly higher than the average earnings for someone in work. Its baloney

My parents have a retirement income for both of them around that. Multiple 5 star foreign trips a year.. new car every couple of years. Way above comfortable and that was supporting two of them

Its infuriating how out of touch stuff like this is

Perhaps if they had put the categories as managing comfortable and well off it wouldn't look so much out of touch and unreasonable

I guess it come down to lifestyle expectations. If your used to having £3k pcm drop into your bank account from your employer then trying to survive on half that will appear impossible

If you have only taken home £1500 PCM then living on £300 a week will be fine. You live within your means. This would be a few years taking £16k,pa out of a ppp. Then, at 67 taking £6k, pa as you now get state pension. So £275k still alot of money.

Thats stopping at 57. Plus 20 years life 67 to 87 on state plus drawing down ppp.

This is a somewhat depressing thread.

My employer pays 8% and I’m paying nothing. I need to start paying in soon. I’m 40. I do have a previous pension but that isn’t much. I decided when I moved here to England and started this job that I needed the disposable income to help me live as I was living on my own, but then that makes it more difficult to sacrifice part of my income. I then got a mortgage for the first time last year which is a term length that should see it payed off before 65. Now with increasing rates and the cost of living, paying into the pension and taking on a larger mortgage next year (renewal time) means that I’d be taking quite a huge hit if I started paying into the pension. Not ideal at all, but that’s the reality. I don’t lead a lavish lifestyle at all.

@stcolin - I was in a similar situation and moved jobs to address it. I was surprised to find that there are still some VERY VERY good public sector pensions available (DSTL being the most recent example - their employer contribution starts at 26%!) and many multi-national private firms also have good pensions. Don't despair, but consider thinking laterally to address it. When you're sub 40, it's all about striving and surviving, but post 40 it seems more about strategy and long term planning for things you've barely considered (or willfully ignored as they're unpleasant to consider and seem too big to solve.) It's still doable - there's 25y!

Thats the whole point of what they’re saying. It’s the upper end, the lucky ones, the rich ones…

Plus those of us who've worked hard for 40 years since leaving school at 16!

But not those that have worked hard for 40 years since leaving school at 16 but had a poorly paid job?

Its totally out of touch. They are saying that to be comfortable in retirement you need an income significantly higher than the average earnings for someone in work. Its baloney

Just because you can live on this, don't assume others can and/or want to.

You for example never had kids, we still ensure our kids are doing ok - especially as they've kids now too. We want to be in a position to help in case they need it, just like my folks & grandparents were for us.

You've also got a flat on rent too haven't you?

You’ve also got a flat on rent too haven’t you?

The flat is included in the £15k.

Isn’t it... 🤔 otherwise the £15k figure is utterly meaningless

TJ. Tell us you did include the flat in the £15k

Yes I did include the flat income.

£15000 is not a lot I agree. I chose to retire at this point and have to live on what I have. I am extremely lucky in also having a chunk of capital although just to make you feel bad 😉 I only got that 'cos Mrs TJ died

A pension income for a single person of much more that the national average wage just to be "comfortable" is absurd. If thats so then only a small% of folk will ever be comfortable in retirement.. IIRC those numbers are from a financial services company and IMO its about trying to scare folk into using their services. to have a pension that big you have tohave been amongst the more well off folk

In the borders- are you really meaning to insinuate I have not worked hard since I left school?

.

.

.

.

.

.

.

.

.

..

Actually you are right I spent a lot of time part time and took a good few years out 🙂

I didn't get my shiz together till I hit 40 and have just retired at 53.

Max pension contributions each year, was 40k, now higher I think from the last budget.

These sites saying how much you need are crap. Only you know what you need so start logging your spending to determine where it's going.

Currently living off ISA and can access my private pension in a few years pending further government meddling.

With a few clicks you can download the complete calculations they've used:

(Doesn't stop people disagreeing with what Loughborough Uni selected for costs of course, but it is transparent)