UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

The whole policy of using housing as 'investment' is nuts, surely they are places to call home, places of community, places of security-- the morality of using a basic human need , shelter , as a method of extracting money (profit) is wrong.

The idea that someone should struggle all their lives, working long hours to pay for a roof over their heads seems very odd.We did invest in communal housing after the war, but that does not fit 'free' market ideology-- it also restricts exploitation.So the great thatcherite con trick is coming home to roost.

Prices aren't dropping because people still think that houses should automatically increase in value, year on year, regardless of the economic situation.

Well everything else keeps getting more expensive, so why not housing?

If you rent you can just move if you want a new bathroom or kitchen.

Yeah, but you can never pay off your mortgage.

In theory, if you buy a house you fix the monthly payment until the house is paid off. If you rent you will have to roughly have inflation increases over that period. So you will be paying significantly more of your monthly outgoings in rent after 20 years of renting than if you had bought.

Djglover - you are also renting out a property that is being paid off by tenants in my example.

Whilst demand exceeds supply, house prices will rise to the maximum people can afford. The only circumstance under which they'll fall sustainably is if we build significantly more and balance supply and demand.

house prices will rise to the maximum people can afford.

My point here is that they've risen to MORE than people can afford, with the extra bit being paid by the government in the form of housing benefit (5 million people receiving it, 93% of whom are working).

"you seem to be oblivious to world markets"... Bingo

Foreign investors are buying up lots of London/SE. When have filled their boots there they will move onto the next big towns and the ripple effect will be felt by most.

"The idea that someone should , working long hours to pay for a roof over their heads seems very odd."

Really? .... Which world do you live on where, the vast vast majority of people have not been "struggle all their lives" for pretty much the whole of history.

Foreign investors are buying up lots of London/SE.

Rich, successful foreign investors? Investors who obviously recognise a good investment?

Well everything else keeps getting more expensive, so why not housing?

Housing is not just getting more expensive, it's getting more expensive as a %age of salary, and has been, at a huge rate since at least the 70/80s, if not (as a general trend) long before that. Most other things have actually dropped in price as a %age of salary over that period (hence a general improvement in living conditions), it's only in the last few years that they have become more expensive.

Somehow, while we have tried to spend less and less on everything else, pushing manufacturing to China, forcing out small businesses, replacing small farms with massive, automated productions, we have been willing to spend more and more money on housing.

talking basic human need-- have we advanced as a species ?

housing does not need to be a commodity, the fact that it is does not make it right !

Foreign investors are buying up lots of London/SE. When have filled their boots there they will move onto the next big towns and the ripple effect will be felt by most.

In Nottingham, a lot of the new build flats were supposedly bought off plan by 'investors from Eastern Europe'. They then promptly crashed in price by ridiculous amounts (like £100,000 in some cases - this bit is definitely true, although who the first buyers were is just what everyone said at the time). It only makes any difference if they are buying things that there is a massive demand for (houses in extremely fancy areas in the South East), rather than being ripped off by our estate agents & developers (buying flats in city centres in the rest of the country).

"Rich, successful foreign investors? Investors who obviously recognise a good investment?"

You could argue that... or you could argue that.... in some quarters, there is soooo much money around that is almost boredom trades... Nowhere else to park that money.

A bit like when someone comes on STW and say I've got 100 quid spare what new bike part shall I buy? Just on a slighly larger scale

Housing is not just getting more expensive, it's getting more expensive as a %age of salary, and has been, at a huge rate since at least the 70/80s, if not (as a general trend) long before that

But that fails to take into account the effect of interest rates.

I think that when you calculate the monthly payments that you would have had to make in 1980 to buy the average house, that it would make up a similar percentage of overall take home pay to that of today. Simply put, lower interest rates helped drive prices up, but affordability remained broadly the same.

"housing does not need to be a commodity, the fact that it is does not make it right ! "

You may well be right... but that's a fight you will NEVER win.... Sorry

Rich, successful foreign investors?

I'd guess with this, you could argue that stamp duty is making houses at < 250k a much better investment than the higher end stuff for investors.

If you've got say, just over 2 million to invest, you could buy 8 or 9 250k flats/houses and pay 20,000 in tax or 1 place for over 2 million and pay 140,000gbp in tax.

This will further reduce the availability of low end housing.

It's all Robbie Fowler's fault. He bought all the cheap houses.

Foreign Investors are primarily buy up parts of Belgravia & Westminster because of the weak pound. It makes the houses cheap(er) and these assets are seen as a safe haven during a time of ecomomic volatility.

They're not buying on the fundementals of the UK housing market and its potential growth over the next 5 years.

They're not buying on the fundementals of the UK housing market and its potential growth over the next 5 years.

They're also quite clearly not betting against it or to a lesser extent have directly bet against a pricing crash.

The market peaked because of easy credit and very low deposits. The cost of housing is related to what people could borrow as opposed to what they could afford. You've effectively got the same people in the same size houses as you had 15 years ago, the difference is the supply and demand side of the market got out of control when people were able to borrow more than they could afford. The low interest rates have sustained the bubble, housing benefit will also be having some affect, as will poeples reluctance to understand that their property is only worth what someone else is prepared to pay for it which today is severely limited by what they can borrow. For those poor sods who didn't buy before the prices went mad in the early noughties I fear the future is bleak as the government isn't going to want to allow a sudden correction in prices, hence the current interest rates. When they go back up there will be a property blood bath.

Lots and lots of people, very small space

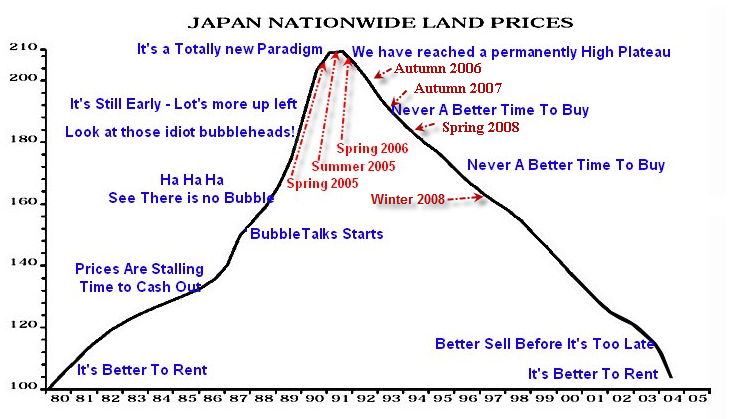

Bit like Japan.

[img]  [/img]

[/img]

The thing that's unique about the housing market in the UK is that we're the only country that had a credit/debt boom that hasn't had house prices reset to historical norms yet. The government's approach - current and former - seems to be "not on my watch". [url= http://www.power-to-the-people.co.uk/2008/09/gordon-brown-house-price-inflation/ ]If only someone hadn't let house prices get out of control in the first place...[/url]

The thing that's unique about the housing market in the UK is that we're the only country that had a credit/debt boom that hasn't had house prices reset to historical norms yet.

I'm not quite sure that's true. A lot of northern europe has experienced huge rises in house prices over the last 20 years, and while a lot have fallen in the last few years, I'm not sure that many have fallen to 'historical norms' yet. Certainly places like Spain and Ireland have, but Sweden/Denmark, and even the US are still much higher than before the bubble.

Ours have certainly grown the most (apart from Ireland), and have barely fallen at all, instead pretty much plateauing since 2007-8. To fall to 'historical norms', even accounting for inflation, you'd be looking at wiping probably 50-70% or more off UK house prices. Obviously that would be bad for homeowners and disastrous for those with outstanding mortgages.

Obviously that would be bad for homeowners and disastrous for those with outstanding mortgages.

I wonder what percentage of the population bought at the peak of the housing bubble as opposed to the numbers forever now locked out of the market or even locked into unsellable property due to a failed market.

I doubt the gov are thinking of the average man.. more the banks balance sheet.

Obviously that would be bad for homeowners and disastrous for those with outstanding mortgages.

As well as apocalyptic for the UK economy as a whole. This recession would look like a blip in comparison.

more the banks balance sheet

The capital adequacy stress-test scenarios included a significant drop in house prices - about 30% I believe, and my impression is that the banks could cope with this. But given the obsession in this country with property prices no government wants to let the opposition point to them as the one that caused the rollercoaster to stop, and of course they won't want their own property portfolios devalued!

Edit:

As well as apocalyptic for the UK economy as a whole. This recession would look like a blip in comparison.

Probably worth reminding people that average house prices dropped by about 35% between 1989 and 1995 and the world didn't end.

One difference between the US and the majority of Europe is that when you buy a house with a mortgage there the only 'colateral' that the Bank holds is the house. Consequently if you can't afford the payments, go bankrupt or it just loses all its value and not worth paying for you just give the Bank the keys and walk away. Here and most other places the debt follows you.

And I'd agree that Housing Benefit is one factor in maintaining house prices, but IMO the lack of availability of houses/land where people want/need to live is number one.

We bought in 2001 for £150k and sold this year for £250k, and the rate of pay for my role is pretty much where it was in 2001...

As well as apocalyptic for the UK economy as a whole. This recession would look like a blip in comparison.

Theoretically, low, stable house prices would be good for the economy. The price of houses now is so much more than the price of building them that lower prices shouldn't have to mean lower wages in the construction sector. People paying much less for houses would mean much more disposable income to spend on other things, so theoretically the price of food and other manufactured goods could rise enough to support UK production. Obviously we can't get from where we are now to low house prices without a huge disaster, and even then, there would be no acceptable way of keeping house prices at that low, or of getting people to pay more for other things.

However, I can't see how things can stay like they are now either. If they do then in a few generations time we'll be back to the middle ages, with a few huge landowners and everyone else spending their entire working lives trying to pay them.

Its all about the interest rates...

Who sets the interest rates?

Theoretically, low, stable house prices would be good for the economy.

Theoretically. But we know what happens when prices drop; interest rates shoot up. The problem is not necessarily that people can't take a hit on the value of the property, it's that they could not afford repayments with interest rates at 8%. Obviously, they'd all default, go bankrupt and their houses would be repossessed. The banks would then own hundreds of thousands of houses worth half of what they'd lent against them so they'd perhaps need bailing out and certainly wouldn't be in any hurry to lend money. Only cash rich investors would be buying (to let, and there would be no shortage of newly homeless tenants). Which leads us back to the middle ages......

But we know what happens when prices drop; interest rates shoot up.

I think you've got cause and effect the wrong way round. Usual process is that interest rates go up (for various reasons) and [i]then[/i] prices drop because people can't afford repayments - one of the mechanisms by which interest rates can affect inflation. Investors then stay out because prices are dropping leaving the market for people who need homes to live in. And don't forget, not everyone is mortgaged up to the hilt.

Feel free to pick holes in this theory.Would it make sense to buy a buy to let as your investment but then rent yourself?

No because any rent you receive will be subject to income tax (probably at the higher rate if you have a half decent job), thereby adding on a possible 40%.

I think you've got cause and effect the wrong way round.

Maybe, but the nett affect is the same. People become homeless and the banks lose money.

Result; entire country in dire straits.

Lots of greedy capitalist ispired people bought cheap houses as buy to lets and saw them as an investment, sadly a lot failed to factor in void propeties and the effect it has on the repayments, so if the flat or house is empty for a month youve lost say 400 quid, per month its empty, your repayments are 350 or hopefully lesss.But you still have to make the repayments.

You decide to rent to benefit claimants, some who dont care, and they wreck it bit by bit and move on, but hopefully you get your rent, but with the new bedroom tax next april, there will be enforced downsizing, and that means either reductions in rent to keep the good tennants or put in dont care tennants who will get a higher rate of benefit due to haveing bigger families.

Result a lot of reppos, and cheap homes, with whole areas decimated as the metal thieves move in, or the ex tennants just vandalise them.

In contrast to some saying no crash, the house i am in at the height of the boom in 2007 was selling for £170k, next door went for £107k a few months back and while the house i am in is currently on the market for £135k, it has had one viewing in two months.

The market is dysfunctional at the moment, some places are good, some are apauling, fundamentally very few people ever buy a house with their own money. They are given money by a bank and house prices are controlled by how much banks are willing to give out.

They are given money by a bank and house prices are controlled by how much banks are willing to give out.

Yep, a good argument for a statutory limit on lending at a fixed ratio x gross salary.

there seems to be a lot of people here making a link between housing benefit and high rent..

Am I missing something here..? Because in my experience housing benefit claimants are very much in the very lowest end of the market.. I didn't think that is was very likely that a rent covered by housing benefit would be anywhere near enough to cover a buy to let mortgage, or that people on housing benefit could afford to rent in the private sector..?

Round this way at least it's nigh on impossible to find a private landlord that will take on tenants on housing benefit, aside from the occasional well established slumlord..

Is there a glaringly obvious point that I'm missing..?

"No because any rent you receive will be subject to income tax (probably at the higher rate if you have a half decent job), thereby adding on a possible 40%"

Isnt that only on the profit(IE after the mortgage and maintainance are paid) though or did i get that wrong ?