UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

Whilst talking about bonds and annuities, what's the hive thoughts about any potential fall out from the US Presidential election in November? Are you likely adjust your investments before any potential chaos and spill over?

(I'm heavily invested in US Equity at the moment and likely retiring anytime between the next time my boss makes another stupid decision and the end of this year...)

Interesting thread ... I have an old, small value pension that I could potentially throw a reasonable amount of £s at for the next 5-7 years which would probably make it a worthwhile thing. Off to see my IFA next week to see if he has any words of wisdom, but cyncial self doesn't really trust/ like him and am wondering whether to just transfer it somewhere like II and then I only have myself to blame ... decisions. ...

Annuity rates have doubled the last year according to my last statement, cash pot has fallen a bit but the purchasing power of an annuity has doubled. Best tip is diversification where poss.

Whilst talking about bonds and annuities, what’s the hive thoughts about any potential fall out from the US Presidential election in November? Are you likely adjust your investments before any potential chaos and spill over?

Perhaps one of the IFAs that are lurking on this thread may want to answer 🙂 We all know what a helpful place this is with people chipping in with their own area of expertise when asked.

poolman

Free Member

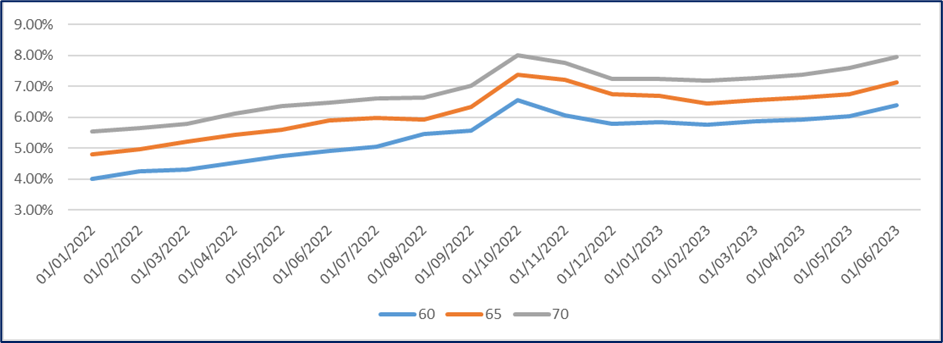

Annuity rates have doubled the last year according to my last statement

Do you mean rates to BUY an annuity have doubled?

My wife has just moved jobs. The new pension is with Standard Life. They have an annual fee of 1% for a vanguard index fund! I’ve found a global index tracker she can use there with decent performance at 0.6%, but no way we are transferring her pot to them at that level!

we’ve had a chat today and she’s going to move her old workplace fund tonight to II, which will give her £1500 cashback, no transfer fee, no fund buying/selling fees. With a Vanguard global fund, it’s under 0.3% total fee including the £12.99/ mo flat fee SIPP charge.

No Vlad , the annuity you can get per £100k of pot has doubled as global interest rates are back from the zero they were post the Global Financial Crash.

I don't think the outcome of US election is likely to be the most likely determinant of annuity rates this year as i don't think there is much differentiation on economic policies (I stand to be corrected on that). But whoever is in charge in the US does have to deal with a booming government deficit which could mean that there is a budgetary crisis (it usually gets resolved) and there is a sizeable body of intelligent people who think that there will be a crisis of confidence in the US dollar in the medium term (although the likely successor to the US position as the world's reserve currency - China - have chronic problems of their own).

In my experience, most workplace pensions held through the large providers are poor value, both in respect of their fees and the performance of their funds. I managed to get a cash alternative paid into a platform of my choice for me to do what i could do, but i got lucky there i think. IFAs can be pricey beyond the initial advice - annual fees based on assets, plus fund management fees plus admin fees etc.

Asset allocation (equities vs bonds vs cash etc and UK vs global equities etc) trumps index tracking vs stock picking. Try and get an asset allocation model and then invest using index trackers. Or just hand it over to Vanguard.

wow @claudie

My ‘managed’ pension made 4% after fees last year, Vanguard 60:40 made 10% and 80:20 made 12%

A small DC pension I've got with Standard Life was worth the same in October 21 as it is now. It's had a little up and down has never been higher than it was then.

That said, even the little chunk of final salary pension I've got has taken a big hit in real terms - it has inflation increases, but they're limited to 4% which isn't a lot when inflation has been over 10% for a few years.

though this is some good news on annuity rates at least

Oct 21 was a big booming high on the back of Covid. Most portfolios are still struggling back to that point.

Just dipping backing in here, and interesting to hear the comments.

What is crazy, is the more that I think about this, the more I google about Vanguard and Royal London and watch YouTube videos, the more confused I think I am getting and I'm nearly at the point of saying, "**** it, let them sort it".....Maybe that is a deliberate ploy with the world of finance to make consumers pap themselves about financial decisions.

For context, I am hoping to retire at 55 (summer 2025), or certainly go part time. Had it been a little further on the horizon then maybe I would have been more confident just sticking it all in a Vanguard 60/40 and watching it for five years or so. But it sort of feels like I'm going to need decent advice about drawdown, crystalizing and all that stuff sooner rather than later..

But it's such a lot of money in fees and annually, their fee is probably going to result in the growth not beating inflation.

And another but, and argument for their advice, what they have done so far is pick out that an old Aviva one started lifestyling a couple of years ago and is already in 50% bonds, 25% cash and 25% equities, so it's been static for a couple of years. Getting that out of there (which I probably wouldn't have noticed until D-day) will probably cover fees. I think.

Edit - ignore. Didn’t read the above post properly.

the more I google about Vanguard and Royal London and watch YouTube videos, the more confused I think I am getting and I’m nearly at the point of saying, “**** it, let them sort it”…..Maybe that is a deliberate ploy with the world of finance to make consumers pap themselves about financial decisions.

I think this is definitely a thing.

Rockhopper - I’d set aside a few days to listen to some podcasts on how to do drawdown. People talk about the money ladder.

Basically, different investments have a different time horizon. Working upwards, you want 2 years worth of money in cash or money market funds so it is available. The next few years is short term low risk investments such as bond heavy funds. The rest is for 7-30 years so should still be invested as it was before retirement. In normal market conditions, you keep trickling money down the ladder to keep the cash and bonds topped up.

The theory goes that most down terms are short term so you don’t want to be taking money from your long term funds in a downturn, so if there is a crash, you can use your 2 years cash, then bond funds to ride it out, not withdrawing from the long term funds until they recover.

In your situation, the £500 initial consultation fee is reasonable, the monthly fees are ok, but the £10k to transfer is just outrageous. That can be done for free.

From what you’ve said, he’s also recommended a situation which he knows will make you worse off!! Would you really trust your whole retirement planning off the back of that?

I want to spend my retirement riding bikes, walking the dog, pottering about the garden and the occasional holiday. Not, listening to finance podcasts, watching the market obsessively, fiddling about with pots, ladders , horizons and trickles. Think I’m in the market for an annuity…

Yep - that’s exactly the point of an annuity. Buy & forget. The pension freedoms were to give those who wanted the ability to manage it themselves via drawdown. But with an annuity all the market risk is priced in, so you won’t see the upside of a good market, and they’ve already priced in the downside to what they will pay you.

If I had retired last year, my annuity would’ve been under £20k, whereas a sensible drawdown would’ve been £50k. But I’ve been actively involved in my pension investments and quite enjoy it.

See, my thought process is with Robola, I don’t want a Ferrari, or a speedboat, and I’d be happy wiling away my retirement tinkering, walking, a few holidays, a bit of volunteering, but not in anyway shape or form, worried or looking or trying to outperform the pension market.

Fair play, it wasn’t a dig at you.

That is a sizeable difference, but the sensible drawdown is in a market doing ok. It may not always be like that.

Another factor I keep in mind is cognitive decline; I might be capable of managing these things early in retirement but it is quite sobering seeing how quickly my older relatives lose the capacity to think rationally about financial matters.

Sensible drawdown allies for market crashes, although it certainly is the case that the timing of a crash can make a substantial difference.

You can also buy an annuity at any stage, so if you felt unable to keep managing, you could cash out as you got older.

No offence taken! I think the pension threads on here really benefit from open and frank discussions. There is no right answer, we are all different. I often see points I hadn’t considered from other posters which change my views on things.

You don't need your advisor to transfer out of poorly performing pensions. I said up thread I want to transfer an Aviva to my Vanguard. Started the process on the Vanguard website 6 days ago. Vanguard have my Aviva cash now.

It was done online on the Vanguard website. Read a few statements then a few clicks. I didn't even need to contact Aviva. Vanguard do that. 10 minutes work. The only info I needed was the name of the provider I was transferring from, my reference, and my current value which I got in 2 minutes on the Aviva website.

£500 for an overall assessment of finances and a suggested plan is fair enough. Nobody works for free. It looks like a bit of a loss leader with the big profits being made once you sign up for a ruins and ongoing management.

10k to consolidate pensions is laughable. IMO. I'm sure as this is Single-track there will be an IFA here who can explain why it costs £10k to gather pensions together and invest them in one place

Half of my pension is managed and, as said earlier, the vanguard 60:40 is massively out performing it over 1 and 5 years so today is the day that I'm cutting ties and switching to the interactive investment sipp mentioned above and moving it into the vanguard fund. This is quite a big deal for me as the pension company has been my security blanket for the last 5 years but this thread has really opened my eyes to fees and performance. I also really like the money ladder analogy. So, thanks to all of you for your input - great thread. I must admit to being a bit over invested in Vanguard but it appears that nothing comes close to the performance for the low fees

@irc, I hear you. I did actually think I might just get that poor Aviva one into my existing workplace one asap as there is a fairly easy and streamlined way of transferring in but then I thought it might be a bit disingenuous of me, if I haven’t even told the IFA what I have decided. (Or paid the £500 fee)

Yes, £10k is crazy daft money to give up for what is, essentially, six template letters.

While there are some knowledgeable people kicking around on here, I was thinking of setting up a new pension and paying into it direct from my small ltd co (sole director/shareholder). Is that called an employer contribution?

I'm currently looking at a provider which applies a tax rebate to each payment I'd be making, but as I'm proposing to make payments from the company's profits rather than from my salary then I can't see that's right?

That’s quite niche - hopefully someone on here has done similar. Can you get advice from Pensionwise, the govt service?

With respect to being overexposed to vanguard, the whole point of the global tracker and life strategy funds is that they are inherently diversified and rebalanced.

My Vanguard Lifestrategy 100 is actually a fund of funds, composed of about 15 different Vanguard index sub funds, diversified globally and by market cap (small cap/large cap etc) The 80/20 will be the same but with a diversified bond portfolio making up 20% of it. They are designed to be a simple one stop , buy and hold product.

While there are some knowledgeable people kicking around on here, I was thinking of setting up a new pension and paying into it direct from my small ltd co (sole director/shareholder). Is that called an employer contribution?

I’m currently looking at a provider which applies a tax rebate to each payment I’d be making, but as I’m proposing to make payments from the company’s profits rather than from my salary then I can’t see that’s right?

Yep, you're right, you just make the payment from the company account, it is an Employer contribution so no tax rebate should be claimed by the provider (make sure they know it's an employer contribution, not an employee/personal contribution). I've done exactly the same in the past when I was self-employed through a LtdCo

I want to spend my retirement riding bikes, walking the dog, pottering about the garden and the occasional holiday. Not, listening to finance podcasts, watching the market obsessively, fiddling about with pots, ladders , horizons and trickles.

This describes me to a tee but my timeline is a LOT more imminent than yours (like I said up thread, mentally, I could retire tomorrow though in reality it's likely later this year).

I'm in analysis paralysis at the moment as I've just been throwing funds into my pension for last 18 years without really paying much attention but it's now dawned on me how much past fees have are into what I'll have available. And the advice I've been paying doesn't seem to have translated to a better performing fund than a low fee index EFT.

So, I'm moving stuff over to EFTs but I've just realized there are so many different types of EFT and no idea which one(s) to choose.

Another complication for me, is I'm (probably) too heavily in cash/low risk at the moment but it seems even more risky to switch out of low risk to higher risk (for better reward later) just as I'm about to retire/with a short time horizon AND (US) markets being so high at the moment...

Luckily, I've still got about 17 years of a very old Civil Service final salary pension as a security blanket should I make some catastrophic decisions! (Granted, my civil service salary 18 years ago wasn't much!)

A final salary safety blanket is very nice indeed. I have similar with an RAF Officers pension from 60 for my 12 years service.

How are you holding the cash? Have a look at money market funds. Basically you will be getting the interest rates banks can get as opposed to what they give to clients, with a risk rating of 1 they are considered the safest place possible and currently paying 4-5%.

You are right that there is thousands of ETFs available. I’m not an IFA and in no way qualified to offer you financial advice, but when I get to retirement I will be holding about 3 months money in straight cash, 2 years money in Money Market funds, 3 -5 years worth in a vanguard 50/50 lifestyle fund , and the remainder of the pot for long term in a Vanguard Diversified Global equity fund.

There are lots of podcasts and YouTube channels you can google to talk about how to set up for sustainable drawdown. Try Meaningful Money, James Shack and Many Happy returns/pensioncraft.

So, I’m moving stuff over to EFTs but I’ve just realized there are so many different types of EFT and no idea which one(s) to choose.

Are you sure you wouldn't be better off with the low cost lifestyle funds if you can't decide what to invest in?

Are you sure you wouldn’t be better off with the low cost lifestyle funds if you can’t decide what to invest in?

I might be if I knew what lifestyle funds are!

....wanders off to Google......

Lifestyle is usually the term associated with the standard workplace pension scheme fund, where as you get closer to retirement, you augomatically move out of growth funds, towards more stable, but low return, funds.

The vanguard lifestrategy is slightly different, in that you put it in the fund with the level of risk you choose, and it contains diversified funds, but doesn’t automatically change.

How are you holding the cash? Have a look at money market funds. Basically you will be getting the interest rates banks can get as opposed to what they give to clients, with a risk rating of 1 they are considered the safest place possible and currently paying 4-5%.

A word of caution...

My main take away from that video is that regulators/govt have completely failed to regulate banks/institutions and the required liquidity they hold.

I’m a bit late to this discussion and apologies if it’s already been said, but Royal London are not only available to IFAs. I have 3 Royal London funds in my SIPP through Interactive Investor, all of which have done well. I’d never go back to using an IFA - can get much better returns with lower fees very easily, just with a modicum of research.

Vanguard isn’t a bad option but there are some pretty poor performing funds in their portfolios which affect the overall returns.

For those people who have used an IFA (whether paid by commission or fixed fee), how often and for how long do you expect them to be "available" to work with you or do work/research on your behalf?

Or more pertinently, has an IFA ever told you to piss off (in a nicer way, of course!) cos they have to spend too much time looking after your affairs? Or tried to charge you extra cos of the workload you generate?

(Reason I ask: I want my IFA to run multiple "what if" scenarios to help me decide on asset allocation, drawdown options and different retirement date scenarios. When I last asked her about it, it involved a two+ hour meeting and I only got documentation for one scenario, so I'm not sure how keen she's gonna be to figure out at least three different scenario types and mix them together... particularly as I just asked her to close an expensive, high commission fund and transfer to a MUCH lower commission fund 😄

This is all such a minefield isn't it.

As i get closer to the 55 year milestone, the thoughts of pulling a chunk of it out at 55 loom high on my radar, not really because i 'need' anything desperately... but because it's tax free i guess, so therefore in my mind makes sense to take it while i'm not being taxed on it.

There's the downside of having 'less' when i get older of course... but my logic is that by the time i'm 70, i won't need as much anyway as i won't be spending fortunes on bikes/life/mortgages etc... So my needs will be lower.

By taking TFC at 55 you are reducing the tax free sum you are ultimately going to get, its growing in a very tax advantageous environment (including IHT) so leave it till you actually need it.

By taking TFC at 55 you are reducing the tax free sum you are ultimately going to get

But surely there's a limit to how much you realistically are going to need anyway ? There's no point having say £3000 a month if you've got no mortgage and debts ?

The scenario question by Vlad would be whatever your client agreement states. You may get more than one face to face meeting but retirement income scenarios is likely to be covered by an additional fee. This work would best be done simply via cash flow modelling, so make sure your IFA offers this service.

There are a number of ways of taking some of your tax free lump sum. If you have a SIPP you can crystalise some of the SIPP then take 25% of that tax free. You can leave the rest invested which means that when you come back to take more of the tax free cash the whole pot may have grown meaning if you manage it carefully you may end up with more than 25% of the whole, tax free.

I realise I have worded that poorly so here is video explaining it.

But surely there’s a limit to how much you realistically are going to need anyway ? There’s no point having say £3000 a month if you’ve got no mortgage and debts ?

Yes and you have to factor in future income streams against your outgoings. I have quite a detailed analysis of our outgoings against our income, including current pensions, SIPP drawdowns, future one of tax lump sums then state pension. Even though I will take around 8% from our SIPPS for the next 3 years, in around 7 years (assuming investment growth around 4%) we will actually stop taking out of our SIPPS (if we choose to) and they will hopefully be worth more than they are now, in around 10 years... (of course this is market dependent) At around 75 our income (factoring a few % for inflation) will be very healthy and I dont think we will need it. Given my mum developed Dementia and lost all of her assets to pay for her care I would prefer to go before that happened (easier said than done I know) My analysis stops at age 80.

That video about drawdown, I get it, but don't necessarily understand it....