UPDATE: Reviews section refreshed, redesigned, searchable: Go take a look

It's half your age at the age you started at.

Ah ok. Errrm. God knows.

Looking at the figures from the calculator I won't be rich, won't be poor,but I'll do ok.

on the rate of return that is good to use, p76 here ->

they have real equity returns at 4%, property at 3% and both bonds and money markets are negative real rates.

Not read the full report but;

our analysis suggests that expected real returns have declined from a

range of 4% to 5.5% in 2012, to a range of 3% to 5% at present

that implies to me to be real returns ie after inflation of 3-5% or 5-7% total That is inline with previous posts and so the 4% safe withdrawal rate remains broadly applicable, no?

that implies to me to be real returns ie after inflation of 3-5% or 5-7% total That is inline with previous posts and so the 4% safe withdrawal rate remains broadly applicable, no?

sorry I wasn't questioning the drawdown rate, more the rate of growth whilst you're acquiring the pot

Ok ish? What exactly would you spend it all on each month if not having a mortgage?

It's kinda interesting how people are really... cautious... about how big a pension they'll need, but don't know what they'll spend it on.

Personally, I plan for the worse and hope for the best. With pensions doubly so!

Yeah, but - unless you have some idea of how much you'll need, it's not planning - it's just chucking money in a pot and hoping it'll be enough.

It’s kinda interesting how people are really… cautious… about how big a pension they’ll need, but don’t know what they’ll spend it on.

I plan a lot of holidays overseas, skiing, MTBing / walking in various mountain ranges etc....

Personally, I plan for the worse

What worst though? You've been on the planet for 60 years, you must know what monthly outgoings you'll have.

I know a few pensioners here in Spain who admit they would have a fairly sad existence in their home country, Holland and uk for e.g. here they live fairly well, run a car, modest house, eat out a few times a week (normally).

If you lived frugally I reckon you could live on 12k GBP here, assuming no mortgage and a buffer of cash if things go wrong. 12k pa would run a house with pool, couple of meals out a week, few coffees a week, car, gym in winter then the beach in summer.

What worst though? You’ve been on the planet for 60 years, you must know what monthly outgoings you’ll have.

Well I probably will at aged 60, but at age 39, and 6.5 weeks into being dad my monthly outgoings are in somewhat in a stage of flux! My main point of reference is knowing the life style my dad has had in retirement and knowing his pension.

Intrigued by this:

for the 75k earning – I wasn’t questioning this, just stating that if you earn 75k when you retire, you probably want to have a 50k pension to not have significant loss of lifestyle – whereas at 50k income you’d be ‘happy’ with 30k.

I'm not in either of those brackets, but close enough. Approximately 20% of my earning goes on tax and another 20% on pension. Approx 20 % of my gross goes on mortgage. Given that my percentage tax will drop hugely then assuming I've paid off my house by then only need to earn 50% as much to have the same disposable. That's before take Ng into account that the kids have left home and I don't need to spend a grand a month on food.

I can't see where you're coming from saying you need to earn 60-70% as much in retirement.

Given that my percentage tax will drop hugely then assuming I’ve paid off my house by then only need to earn 50% as much to have the same disposable.

And also no National Insurance to pay which is another 11% of earned income (my understanding is that if you've paid enough NI years you would not need to make any more contributions until state pension age if you retired early on other income)

I can’t see where you’re coming from saying you need to earn 60-70% as much in retirement.

Particularly when people are apparently living on 60-70% of their salary already in order to fund their pensions...

@wobbliscott 's post has given me a lot of food for thought. In 52 at the moment.

In fact, it's kind of got me fired up to do a bit of living in the next decade or so!👍

I'm used to living on not a lot of money which helps. Bikes being my only real costly luxury but I've got my couple of bikes pretty much how I want them now.

https://monevator.com/what-is-a-sustainable-withdrawal-rate-for-a-world-portfolio/

for the 75k earning – I wasn’t questioning this, just stating that if you earn 75k when you retire, you probably want to have a 50k pension to not have significant loss of lifestyle – whereas at 50k income you’d be ‘happy’ with 30k.

Well if you've been shovelling 40k pa into the pension and a chunk of the rest into ISAs for years then you're not likely to notice a dip in lifestyle...

I can’t see where you’re coming from saying you need to earn 60-70% as much in retirement.

You wouldn't need to earn that percentage IMHO

My wife and I are both retired. We are on 50% of our final salary but take home c 65% of our 'last working months take home'. In real terms we are better off. We now have no mortgage, no longer pay a huge chunk into the pension, no longer pay NI and have chosen to drop to 1 car from 2, so lower monthly there. Lockdown has shown us what we could live on with no extras.

Planned properly, 6 weeks in Spain or Portugal in February/March can be done very cheaply so getting away from dull and dreary UK is easy enough.

Posh holidays? Not really my thing but easily do-able every couple of years if you really planned for it...same with a new bike etc.

Thinking about the above and yeah, I dont think I would need anywhere near what my current level of income is to have a lifestyle I would enjoy.

As has been mentioned the obvious big difference would be not having the mortgage and overpayments (soon to be pension payments) coming out - that's probably worth 30% just there. We bought the house we could afford a few promotions ago and never moved up as we got more money which puts us on a good footing there. Then as above lockdown has made me realise that the simple things and a slower paced life are enough to keep me happy, and as someone said a less manic goal orientated use of free time will be a saving. Not being bound to the school holidays makes those about a third of the price too, and my hobbies are all relatively cheap things like running, hiking, cooking etc

I've rung around the historic providers for the pension scheme at work and found I have a couple of amounts so I'm not starting from zero either which is good but looks like I have some work to do if I want to beat the mortgage, squirrel a ton away in pensions and have enough to bridge a gap from say maybe 52 to 57

no longer pay NI

Make sure you keep your NI payments up to date with voluntary contributions if you want to get the max state pension. A simple check on gov gateway will tell you if up to date or short

Make sure you keep your NI payments up to date with voluntary contributions if you want to get the max state pension. A simple check on gov gateway will tell you if up to date or short

For those of us who didn't 'waste' their years away drinking in the Uni Bar we're already well passed them - it's only 35 years.

This thread has really got me thinking.

I have got 4 pensions in total from 4 different employers - only one is currently being paid into & is the one that is the largest, so I tend to concentrate on what that will give me in my retirement.

I generally have money left over at the end of the month - normally not a ton of it, but some. Currently with lockdown restrictions & no commute, there is obviously more.

I am currently overpaying the mortgage by a modest amount, but constantly wonder about the worth of doing that with low interest rates. I could put that money in an investment ISA & make it work harder. It would also be available if needed, whereas the mortgage overpayments are gone once the payment is made.

Or I could put the money onto my pension but again, that money is then not available should the need arise.

The rest of the money gets chucked into random savings accounts - one for house renovation work that needs doing (new boiler soon, hall, stairs, landing redecorating & a new kitchen at some point) and another which is just a random savings pot. But they earn bugger all interest so seems like a foolish way of doing things.

I think I need to review all of my spending & have a bit of a re-jig.

For example, I'm currently paying £150 a month into childcare vouchers, but we barely have any childcare requirements. We envisage will we need to use after-school clubs in the future & probably for a few weeks during the summer holidays, but we have a current balance of over £3k of vouchers which should keep us going for a while.

Anyway - good thread this. Certainly gives some things to think about.

stumpy01

Eggs and baskets. Don't concentrate on any one 'investment' or investment type IMO.

have a look at LISAs as well if you want a blend of locked-in and not. LISA is better than an ISA for retirement saving (but worse than a pension) - but the advantage is you can take your cash out of a LISA at any point with a minimal cost (something like 4%) if you have to. There's a bunch of limits as to how much and who (under 50s, 4k a year) but its always good to get some free money from the government.

as for retirement spending, everyone's different. I imagine that going from 7 weeks a year of messing around in foreign countries to up to 52 will significantly increase my spending in the first 5-10 years, although it might well slow down after that.

LISAs

unfortunately for me (and others....)

Anyone aged 18 to 39 can open a LISA

I would look at pension contributions now as there is a chance tax relief will change in the budget.

I see my pension as long term savings now as I retire (60) in 14 years, and no other investment can come close to the 40% bonus of tax relief.

If you've got old DC pensions, folks, check the charges and investments - might well save a few bob transferring them to a low cost SIPP with a decent range of index trackers, ITs etc

For those of us who didn’t ‘waste’ their years away drinking in the Uni Bar we’re already well passed them – it’s only 35 years.

Assuming you didn't get caught up in the opted-out pensions that were the rage a few year ago that don't count towards your numbers IIRC (could be wrong).

I checked the gov website about my contributions (like you assuming I'd have my 35 years in in the next year or so). Apparently not, even though I was in full time PAYE employment it came up saying I'd only part paid in some of my early years (no idea how or why) so I've potentially three more year that I wasn't expecting and far too late to get it sorted.

I'm also a bit confused about the 35 years. The gov website says 34 full years so I assume it will tick over to 35 in the next tax year, April? Which will give me full allowance.

I certainly don't recall having a job and paying ni between 16 to 20 so not sure how it's hit 34 really.

There are exemptions and years that count without contributing. IIRC my two years at college (16-18) count, but my uni years don't count (although I got a partial credit for part time work)

Never mind - I misread.

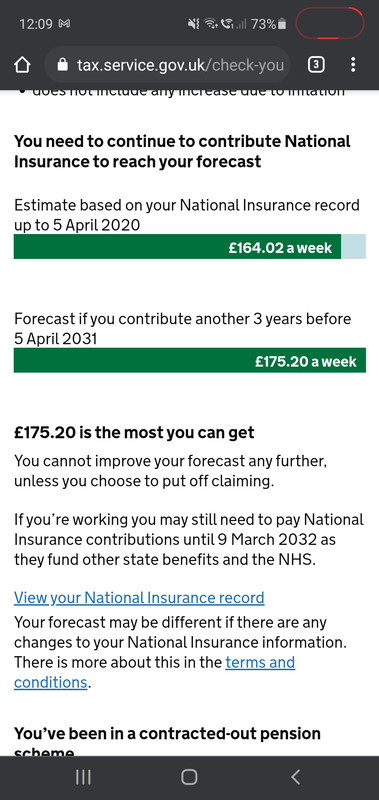

Yes I wasnt clear it shows me as having 34 full years of contributions in the forecast portal.

34 years of full contributions

17 years to contribute before 5 April 2037

You do not have any gaps in your record.

Which is odd as i was in higher education till 20 or so & did some slacking off in my late 20's.

Good result though.

40% bonus of tax relief.

whilst the tax relief is good, its worth remembering that its only for the initial ~25% (tax free lump sum) + 3kpa (difference between state pension and tax free limits) of income - after that you're taxed at 20% or (less likely) 40% on your income - still good but not as good.

I think he was referring to the tax relief on the money paid in, rather than coming out.

– still good but not as good.

As what?

Just to the OP. I am retiring soon on about 1/4 of what you will have. I do not care that i will be skint. I will not be working

As what?

its not as good as 40% off. In fact, LISAs, VCTs, and EIS can all be more tax efficient depending on your cirucmstances

its not as good as 40% off

It really is. You pay money into into a pension. The government instantly adds 20%. Then when you do your tax return, you tell them you put money into a pension and then they give you another 20% (assuming you are paying higher rate, of course). Then you get the compound growth on that 20% until you draw on it. I don't really think you can beat that with any of your other options.

Wait what? As a paye employee I need to do a tax return?

I was auto opted out by work, had no choice so I still have 3 yrs to pay despite 40 yrs of contributions

@stumpy01 - re: childcare vouchers, sure you're aware but you can't turn them back into cash. I'd have a clear plan on when and how you're going to spend that £3k

I have £300 in vouchers sitting there now with no way of spending them. Youngest is going to senior school in September so no need for before/after clubs anymore. Only way I can think of using the money is on private tutors who may accept the vouchers

It really is. You pay money into into a pension. The government instantly adds 20%. Then when you do your tax return, you tell them you put money into a pension and then they give you another 20% (assuming you are paying higher rate, of course). Then you get the compound growth on that 20% until you draw on it. I don’t really think you can beat that with any of your other options.

Its not as good as 40% when you're taxed 20% on close to 75% of what you withdraw. Its much closer to 25%.

An seis has a 50% tax claim and an eis is 30%. Both of those significantly beat pensions from a pure tax perspective (although they are generally riskier investments)

I still have 3 yrs to pay despite 40 yrs of contributions

I'm in exactly the same position: years to go, contributions to make.

At today's rates, Grade 3 contributions would cost £2340 for 3 years worth, @ £15 p/w.

At least I have 11 years to decide if it's worth it, for £10 a week

This is a fascinating post. I am 55 tomorrow, working in a good job and decent salary, with a fairly poor private pension. No mortgage, nice house, 2 teenage kids, and moderate savings (a year of net income] plus a good planned inheritance which is unfortunately not too far distant.

I haven’t really thought much about all of this until this thread !

I take it you are retiring in just under 4 hours?

Is there a school of thought that you’re better to spend now while younger and fitter and can enjoy life, work till 67 and accept you’ll be poorer when less able to do the good stuff anyway.