I'm looking at getting a mortgage in the next few weeks, I want to pay a 10% deposit and borrow the rest over 20-25 years. However, when my current house sells, I want to make an overpayment of around 30%.

Is there a certain type of mortgage I need to be able make an over payment rather than a two year fixed?

Thanks in advance.

Any mortgage with Natwest they would let us overpay up to 10% of the mortgage per year.

when do expect to make the overpayment?

Most trackers allow overpayment without penalties.

All the fixed rates I looked at had the same 10% per year as NatWest.

I'd Make the payment within the first year, or put it in an account until the fixed term is up maybe?

Most mortgages allow you too make an over payment of around 10 % per year.

If you plan to pay of a 30% you may want to consider getting a mortgage with a short tie in period ie 6 months (or when you expect to have the lump sum) as you will be bringing your loan to value down considerably so will be able to get a much better rate once you have done that rather than locking your self into a longer deal.

May be worth getting an adviser on the case..?

If you want the details of my mortgage adviser email (in profile) me - i am NOT on commission:)

EDIT - run the number either way to see what you would be better off with anyway.

10% a year without penalty here too.

I would opt for the advised service your lender would offer and ask them. You could take it on the SVR or any other product with no tie in, make the overpayment and switch it to a fixed. Also I'd probably fix for longer than 2 years iiwy unless you're loaded and happy to take the risk.

You could consider an offset mortgage, to allow you deposit the cash and get the benefit of it reducing the interest you pay. Get one with a 2 year deal and you could re-evaluate then and perhaps reduce the balance at that point. Alternatively go for a tracker with no erc as suggested above.

As the person above has suggested, offset may be an idea. Not aware of any fixed rates allowing that size overpayments in one go (without penalty)

jekkyl - Member

Also I'd probably fix for longer than 2 years iiwy unless you're loaded and happy to take the risk.

Far from loaded and not brightest bulb, so a lot of the info goes over my head. I bought at the right time about 15 years ago, allowing me to upgrade now.

Planning on buying a house that needs renovation and stay in mine until it's ready. Then sell the current house and make the overpayment from the sale.

Far from loaded and not brightest bulb, so a lot of the info goes over my head.

🙂 it's free.I would opt for the advised service your lender would offer and ask them.

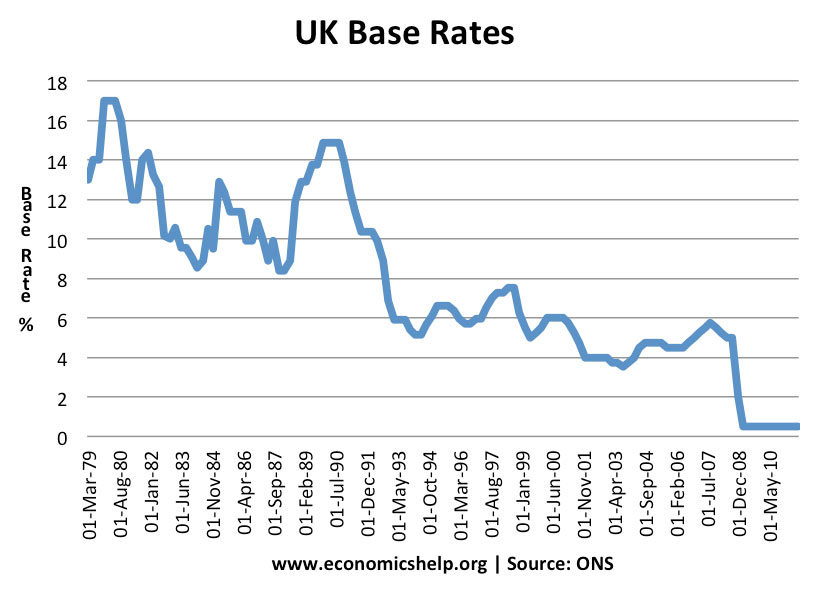

rates are at an all time low, we are entering a period of economic uncertainity, don't mention the b word. Fix for longer than 2 years!

[img]

[/img]

[/img]

Thanks for all the replies, a bit more to look into.

Do not mention that you are wanting to make a big payment during the term. I was having an off the record chat with my mortgage company about some extra borrowing. I needed 50k for my dad who's pension was due to mature but not in the time frame he needed it. I mentioned that I'd be getting the money back in 6 months. I was immediately told the chat was no longer informal and a note would be placed on my account as I'd enquired about short term lending. 👿

We've always used an offset to allow savings or overpayments to benefit us. We can pay off any amount during the term, though not 100% of course

Tracker rate for unlimited over payment and the ability to then switch to a fixed at any time, maybe when large reduction made. All penalty free

I'd go for a 5 or even 10 year fixed with an offset facility. The offset is effectively paying a big lump off (i.e. reducing the amount you're paying interest on) but leaves you flexibility to take it out of the offset if you need.

First Direct mortgages allow unlimited overpayments.

An alternative would be to invest the money and overpay by 10% per year over a number of years?

That sounds like our mortgage, which is a tracker. It's with Coventry Building Society and early redemption charges are only £125 when we are in a position to finish it early. 2.3% at the moment.We've always used an offset to allow savings or overpayments to benefit us. We can pay off any amount during the term, though not 100% of course

Spoke to HSBC today, agreed in principle but as it's classed as a second home, they want a 20% deposit.

Doable but only just.

Why classed as a second home? If it is you could be in for stamp duty woes

As I'll still own my current home until the new one is refurbished. It is under the limit for Stamp duty.

You might still pay stamp duty upfront as owning 2 homes even under stamp duty levels. Within time limits you might be able to vlaim it back when current home sells.