If ever you wanted to know what could go wrong with paying people to dig holes in the ground and then fill them in, look no further than England’s coronavirus test and trace system.

The idea behind a crude Keynesian fiscal stimulus such as we’re seeing is that it does not matter much what government spends the public’s money on. That cash will end up as people’s income, which they will spend. It then becomes someone else’s income and multiplies the original public expenditure significantly to ease a nation itself out of a metaphorical economic hole.

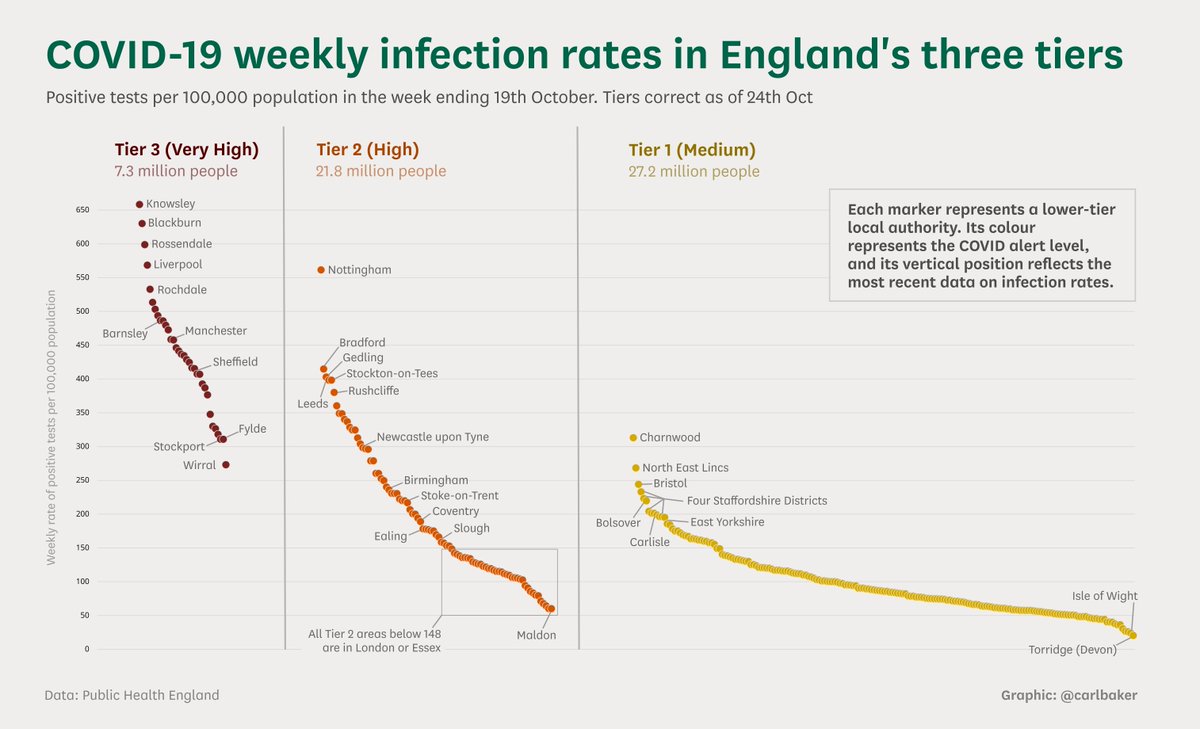

The test, trace and isolate programme was introduced in England in May. It was expected to bring huge returns to the economy, with the Treasury allocating £12bn to it this year, comparable to what the government spends on nursery and university education. The promise made by Matt Hancock, health secretary, was that it “will help us keep this virus under control while carefully and safely lifting the lockdown nationally”.

This was not one of the speculative moonshots the prime minister’s team are so hopeful will transform the economy. Instead, it was a supposedly a careful investment of 0.6 per cent of UK national income with huge returns all but guaranteed. The service would allow the economy to reopen safely, emerge from a Covid-19-induced more than 20 per cent drop in output, and limit pernicious long-term economic scarring.

Not only would the government spending form the income of employees in the test and tracing system, it would also enable many more people to resume their past livelihoods, generating returns far in excess of the cost. If it contributed to a recovery worth 6 percentage points of national income, a tenfold return would have been achieved in a matter of months.

The problem has been that the money was not spent well. Test and trace has been mired in crises since birth. This autumn, it has failed to deliver sufficient tests, been slow in informing people they have tested positive and allowed a spreadsheet error to miss almost 16,000 positive cases. Trust has evaporated to the extent that the UK’s scientific advisory group has assessed it was having at best a “marginal impact” on transmission of the virus.

There is a strong case to go further and say the £12bn has so far had a negative rate of return. By allowing people to believe the nation had built a world-class system, social distancing slipped, the virus spread and the country is again thinking about local or national lockdowns, with inevitable severe economic costs.

How governments spend money matters. As Andrew Bailey, governor of the Bank of England, said this week, “there is scope for sustained public investment, but it does have to be on projects that earn a rate of return and [our] history is quite mixed on that front”.

Latest coronavirus news

Follow FT’s live coverage and analysis of the global pandemic and the rapidly evolving economic crisis here.

In the wider field of economics, an increasingly fashionable view is that governments should use fiscal policy and heavy borrowing to run the economy hot so as to use all available resources and minimise unemployment. The only downside, according to schools of thought such as modern monetary theory, is a bit of possible inflation, which can easily be tamed.

The lesson from British public-sector investment disasters, including the Humber Bridge, advanced gas-cooled nuclear reactors and the NHS electronic patient record system, is that the growth-enhancing promises of investment projects are often overstated and multipliers might be very small.

What test and trace has added to the picture is that if government gets it wrong, returns and multipliers can be negative. In other words, if you’re going to turn on the public spending taps, make sure you get it right or you will end up with a horrible mess.