- This topic has 0 replies, 919 voices, and was last updated 4 years ago by Cougar.

-

EU Referendum – are you in or out?

-

teamhurtmoreFree MemberPosted 7 years ago

TOJ – IIRC that comment is actually coming from Michel Barnier who is the EU’s chief negotiator. Newsnight had good coverage on this last night

oldnpastitFull MemberPosted 7 years agoJunkyard – lazarus

– stealing off savers

no matter how often you say this or something like it it is and will always be what you term post truth politics or complete BS if someone else says it

Its just is not true even the phrase held artificially low is BS

Artificially low interest rates is exactly stealing from savers.

Anyone with lots of savings on deposit has lost out massively over the last few years, in order to benefit people with debt.

mtFree MemberPosted 7 years agoI’m a little surprised that Michael Fish has not complained, is he still out there?

teamhurtmoreFree MemberPosted 7 years agoOf course it is oldnpastit, but governments rely on folk being economically and financially illiterate so that they can get away with it.

We have seen a massive reallocation from the financial prudent to the financially imprudent. Its a travesty that only survives through ignorance. Cash savers have “lost” around £160bn or £6,000 per household (according to HL study)

meftyFree MemberPosted 7 years agoArtificially low interest rates is exactly stealing from savers.

This is true and as one of them it hurts! However it could be argued that it goes some way to addressing inter-generational wealth imbalances.

cchris2louFull MemberPosted 7 years agoThe credits cards spending was huge at Christmas.

At some point it needs repaying .KlunkFree MemberPosted 7 years agoWe have seen a massive reallocation from the financial prudent to the financially imprudent.

and it’s creating a nice debt bubble….

the bank has it hands tied now (missing numerous chances to raise rates gradually to ween us off credit)

teamhurtmoreFree MemberPosted 7 years agoThis is true and as one of them it hurts! However it could be argued that it goes some way to addressing inter-generational wealth imbalances.

alternatively, it has increased imbalances by creating a wealth effect through property (bad for younger generation) and asset prices (ditto).

teamhurtmoreFree MemberPosted 7 years agoNo necessarily kimbers, the devaluation has already increased inflationary pressures and expectations which will put pressure on rates and those who remain addicted to debt financing. There is no such thing as a free lunch or having you cake and eating it, unless you are a Brexshiteer or a Scottish Nat

kimbersFull MemberPosted 7 years agono necessarily kimbers, the devaluation has already increased inflationary pressures and expectations which will put pressure on rates and those who remain addicted to debt financing. There is no such thing as a free lunch or having you cake and eating it

whos going to have the balls to pull the rug out in the middle of brexit though, the treasury/b o e/ sensible politicians are still worried about the economy, housebuilding is still a joke (garden cities then garden towns, now May promises garden villages 😯 ) the ftse is soaring to record highs-itll crash hard when the borrowing stops and we learnt from last time that whoever is in charge gets the blame regardless of actual fault.

teamhurtmoreFree MemberPosted 7 years agoIt’s the responsibility of our independent Central Bank. They have only two jobs to do: one is the manage inflation within a target range. Current rates are incompatible with inflation expectations, so the challenge is obvious and cannot be ignored

kimbersFull MemberPosted 7 years agonah they know whatll happen to the economy if they did rise

they will try a small rise at first,

but they wont be bold enough for fear of upsetting the economy and risking their independence- judges, ambassadors any civil servant that dares upset the brexiteers plans better get ready for a barrage of hate from the increasingly emboldened right wing pressJunkyardFree MemberPosted 7 years agoArtificially low interest rates is exactly stealing from savers.

Anyone with lots of savings on deposit has lost out massivelylost out massively on what they may have reasonably expected is true theft is not true as a description of that unless you wish to redefine the word.

Cash savers have “lost” around £160bn or £6,000 per household (according to HL study)

indeed they have “lost” but they have not been robbed or the victims of theft as you claimed that is still what I challenged and we all know its not theft.

It may be unfair on the “financially prudent “* but it is not in any meaning of the word the crime of theft/stealing.

Please be accurate in your descriptions or go report the “crime” that has never happened ,then take them to court and get back to us on your “success”.

* which means wealthy really as who else has savings? and its not possible to be “financially prudent” for those on a low income as they just dnt have enough 60 % have less than 1k saved its because they dont earn enough to save rather than lack of “prudence”Still lets all worry about the better off minority as they must be the ones really feeling the pinch in this financially austere timePS

If rates were artificially low, then attempts to raise them should be successful. But recent attempts by central banks to raise rates have all gone poorly. Japan tried in 2000 and 2006, Sweden in 2010, the ECB in 2011. In each case the economy soon went back into recession and/or deflation, and the central bank had to cut rates back to zero to prevent an outright depression.

still feel free to argue with OHD economists because if you want three opinions ask two economists 😉

http://econlog.econlib.org/archives/2015/04/what_does_it_me.html#

teamhurtmoreFree MemberPosted 7 years agoAt the moment kimbers, they will try and hold off as long as possible – but the lower for longer approach merely stores up future problems. Did I mention, no such thing as a free lunch?

So more stealing on the way….

…still no harm in flooding markets with liquidity at a time of artificially low rates is there? Lessons….history….failure…

JunkyardFree MemberPosted 7 years agoIt is still not stealing that is just an outright untruth delivered by yet another purveyor of post truth BS

mrlebowskiFree MemberPosted 7 years ago* which means wealthy really as who else has savings? and its not possible to be “financially prudent” for those on a low income as they just dnt have enough 60 % have less than 1k saved its because they dont earn enough to save rather than lack of “prudence”Still lets all worry about the better off minority as they must be the ones really feeling the pinch in this financially austere time

You’re not really bitter at all are you..

fifeandyFree MemberPosted 7 years ago60 % have less than 1k saved its because they dont earn enough to save rather than lack of “prudence”

I’d love to see some facts/figures on that.

All i see everywhere is people pissing money away on monthly subs (smartphones, netflex, 100000mbit internet etc) and then wondering how it is they have no money. And that’s before we get to interest payments on the debt they have built all so they can view facebook in 1080p whilst on the bus.your statement being true for 10% I could quite believe, but 60% seems a little far fetched.

teamhurtmoreFree MemberPosted 7 years agoOne only has to look at how quickly market rates responded to a change in ECB stealing this week, to see that rates are artificially depressed – eg, Portugal.

Central Banks are deliberately distorting/mispricing risk thereby stealing off investors who are not receiving the correct return to compensate for the risk that they are willing to take.

mtFree MemberPosted 7 years agoPost truth? Is that a different set of lies to the Pre truth era? Perhaps its the same lies but said by some you don’t like and who you don’t want to agree with. Given the post truth verbiage on here i’d remind us all that “the person in the room you like the least is the one thats most like you”.

Now the soon to be Free State of Yorkshire there is only one truth. Our beer is without question the best. Once we are out of the EU, UK and the rest of the world beer will be free, its gonna be great.

jambalayaFree MemberPosted 7 years agoLow interest rates have been essential to prevent numerous EU countries going bust and to achieve the same for massively indebted individuals.

As @firefly says there are many people with no savings who have fancy smart phone and go out every Fri/Sat night apending £££. That’s before we talk about holidays and cars.

@tmh the Cambridge Paper is worth reading, only 60 pages and a lot you can skim. Very little chnage in services as tariff free and few cross border restrictions (eg Indian call centre / management consultancy / advertising and marketing …)

teamhurtmoreFree MemberPosted 7 years agoPost truth? Is that a different set of lies to the Pre truth era? Perhaps its the same lies but said by some you don’t like and who you don’t want to agree with.

Best ignored, other than noting confirmation that governments rely on people misunderstanding what is going on

Jambas, low interest rates are keeping zombies afloat, distorting markets, mispricing risk and largely impotent when corporates and households are deleveraging. Your new friends (Wynne Godley et al) at Cambridge would not have approved!

JunkyardFree MemberPosted 7 years agoYou’re not really bitter at all are you..

you are not really able to negate the points made so you just shot the messenger rather than addressed the message

I’d love to see some facts/figures on that.

moneyfacts is the source for the amount the reasons are mine not theirs- imagine checking the figure before posting if only this would catch on LOOKS AT JAMBY IN PARTICULAR 😉

how quickly market rates responded to a change in ECB stealing this week

and you say I troll – too obvious THM too obvious you like to press buttons but that just made me chuckle

Central Banks are deliberately distorting/mispricing risk thereby stealing off investors who are not receiving the correct return to compensate for the risk that they are willing to take.

Are your pants on fire?

Its a risk to put your savings in a bank now is it 😀 again too obvious and far less funny

As @firefly says there are many people with no savings who have fancy smart phone and go out every Fri/Sat night apending £££

yes anyone who does not have savings is clearly profligate with their money rather than living on the margins of affordability- you checked that as a fact before posting didn’t you and will show us income rates and saving to prove their is no relationship between the two I assume

teamhurtmoreFree MemberPosted 7 years ago@tmh the Cambridge Paper is worth reading, only 60 pages and a lot you can skim. Very little chnage in services as tariff free and few cross border restrictions (eg Indian call centre / management consultancy / advertising and marketing …)

I read it – hence my earlier thanks for the link. I appreciate you positing it too since (1) it does not support your view/views 😉 and (2) I am a fan of the “school of thought” behind it and their different understanding of our current problems.

On a wider issue it also highlights a key problem with economics. The over-use of mathematics leads to a false sense of accuracy/definition/precision in a subject that is at best a messy one. Relationships are rarely linear nor constant and models and maths give a totally false sense of the real world. This is reflected in the wide range of outcomes from sources using largely the same underlying model.

JunkyardFree MemberPosted 7 years agoPost truth? Is that a different set of lies to the Pre truth era? Perhaps its the same lies but said by some you don’t like and who you don’t want to agree with.

its what THM says when someone says something they KNOW is untrue and yet he will do it himself – its not actually theft- so I merely pointed out his hypocrisy and he failed to attempt a defence beyond his usual digs – he also likes to remind us to not play the man assuming the man is a man he likes.

IMHO post truth is just saying something you know is BS and pretending its true

Its not theft though it may well be unfair – that is at least debatable.jambalayaFree MemberPosted 7 years agoAnother Brexit victim –

😀

So the Australian franchises went into receivership due to Brexit ? It’s a love or hate it chain, I think its ok but there are many who feel it’s over priced rubbish.

kelvinFull MemberPosted 7 years agoLow interest rates have been essential to prevent numerous EU countries going bust and to achieve the same for massively indebted individuals.

Is Japan in the EU, is Switzerland in the EU, is the USA?

Seriously, what the —- are you on about? Low interest rates across the First World.

jambalayaFree MemberPosted 7 years agotmh ah missed the reference, I post stuff from all view points. The peice is pretty positive despite negative assumptions. As Insaid had that been the “project fear” scenarios I think Leave would have won by more. We will start seeing more positive pieces going forward as Economists eat their humble pie as actual data continues to be much more positive. Europe is in a dreadful state economically, sp ething is going to break sooner rather than later.

JunkyardFree MemberPosted 7 years agoThe over-use of mathematics leads to a false sense of accuracy/definition/precision

its strange as people want ever more accurate predictions but each attempt just makes the science look worse

for example if a billion people started smoking today no one could say exactly which ones get cancer, when where it would cluster etc

yet we all know that cancer rates will inevitably riseIn much the same way the modellers were correct that Brexit will be “bad” but not able to say exactly how bad – see also global warming and any number of areas where folk are amazed we cannot actually predict the future with 100% degree accuracy and use this as a method to deride the entire subject/experts.

jambalayaFree MemberPosted 7 years ago@kelvin yes indeed. My point is that’s a big part of why the EU has low rates. Switzerland has negative interest rates to try and discourage money flowing into the country out of bust Europe, Japan has had ultra low interest rates for decades as they still haven’t really dealt with the excesses of the 1980’s (sound familiar ?)

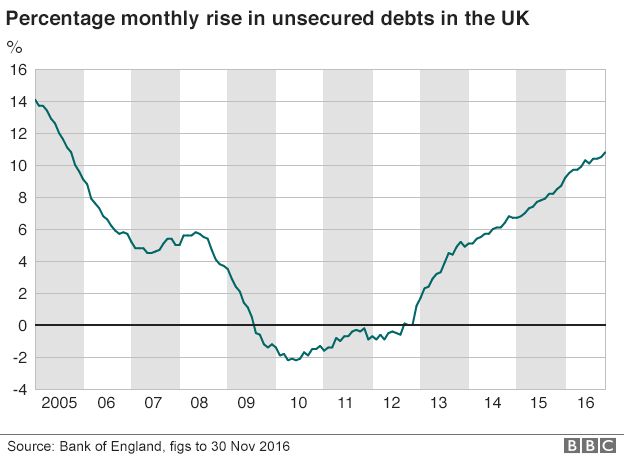

CloverFull MemberPosted 7 years agoAre we betting on whether credit will continue to rise to a point of catastrophe or whether it’ll go down a bit because it was a ‘last hooray’ response to the expectation of price rises and belt tightening during 2017/18?

I’m not sure, although the scale of consumer credit is now alarming. Again.

kelvinFull MemberPosted 7 years agoSo the Australian franchises went into receivership due to Brexit ?

The news in that link is about UK branches closing.

The Australian buy out/back is old news.brFree MemberPosted 7 years agoAnother Brexit victim –[/I]

Wouldn’t think so, footfall doesn’t cover overheads – wonder what the ‘fees’ are to the mother business?

teamhurtmoreFree MemberPosted 7 years agoJambas – not sure it is positive, just less negative than others largely because (IIRC) their model treats consumption differently

While we include a scenario based on Treasury assumptions, a more realistic, although in our view still pessimistic, scenario assumes a much lower level of the trade loss than that of the Treasury. The results are presented through comparing these scenarios with a pre-referendum forecast. In the milder Brexit scenario there is a 2% loss of GDP by 2025 but little loss of per capita GDP, and also less unemployment but more inflation. In the more severe, Treasury-based scenario the loss of GDP is nearer 5% (2% for per capita GDP), inflation is higher and the advantage in unemployment less.

Actual data is not much more positive – consumption and services have held up well, the pound has weakened as predicted and inflationary expectations have increased. So a mixed bag. Remember too, that these models all include assumptions about a life post-Brexit and this has not happened. The BoE admitted yesterday that they underestimated the resilience of consumption. That was it really.

FWIW, econ data from Europe surprised on the upside yesterday! German’s want rates to rise see Handelsblatt from two days ago

kelvinFull MemberPosted 7 years agoWouldn’t think so, footfall doesn’t cover overheads – wonder what the ‘fees’ are to the mother business?

Overheads – they pride themselves on using Italian ingredients, not UK sourced ones, so margins tighten when the £ drops. Plenty of UK companies are built on trade, because, well, you know, the world is not one little island.

So a mixed bag.

We are still in the EU, and a party to all the trade deals and agreements that the EU has with non-EU countries.

And we’ve delayed triggering our exit for an extra 9 months, so 2 year plans can still go ahead as normal, for now.teamhurtmoreFree MemberPosted 7 years agoI know – but the macro trends can still be observed so far and they are a “mixed bag”. Happy?

Oliver misread the market clearly. His massive overuse of garlic in most dishes is incompatible with our newly uncovered xenophobia. Who wants breath like a S European these days? 😉

kelvinFull MemberPosted 7 years agoAgreed… Italian food made with Italian ingredients… string the traitor up!

teamhurtmoreFree MemberPosted 7 years agoWe are still in the EU, and a party to all the trade deals and agreements that the EU has with non-EU countries.

Ssshhhh, dont tell the Brexshiteers that we already have trade deals with nearly 90% of our trading partners as it spoils one of their five lies.

EdukatorFree MemberPosted 7 years agoLow interest rates have been essential to prevent numerous EU countries going bust and to achieve the same for massively indebted individuals.

Greece was paying 25%, Portugal 9%(or more), Spain 7%… not low interest rates.

The countries in difficulty were put in more difficulty because of Germany’s refusal to fund debt with Eurobonds in the same was as the Fed funds states in difficulty with money at low interset rates.

The topic ‘EU Referendum – are you in or out?’ is closed to new replies.